There’s a reason why many analysts are loathe to cover technology firms — they’re just too damn volatile. Magnify that by three or four times for companies in burgeoning industries like cybersecurity. FireEye Inc (NASDAQ:FEYE) is a prime example of sound logic convincing you to go long, only to wish you hadn’t. Unless you’re the Wall Street equivalent of Tom Brady, you can’t take the kind of hits FEYE stock has absorbed and simply get away with it.

I mean, who doesn’t love cybersecurity? Whether you’re talking about PC viruses or possibly altering the presidential election, cybersecurity is a hot-button issue.

Companies like FEYE are on the forefront of this ever-expanding and dynamic sector.

Because of this distinct dynamism, you’d figure that there’s plenty of room for competitors. I doubt that cyber-criminals are always going to use the same tricks. Thus, coming to market first may not necessarily be the absolute advantage that it is for other industries.

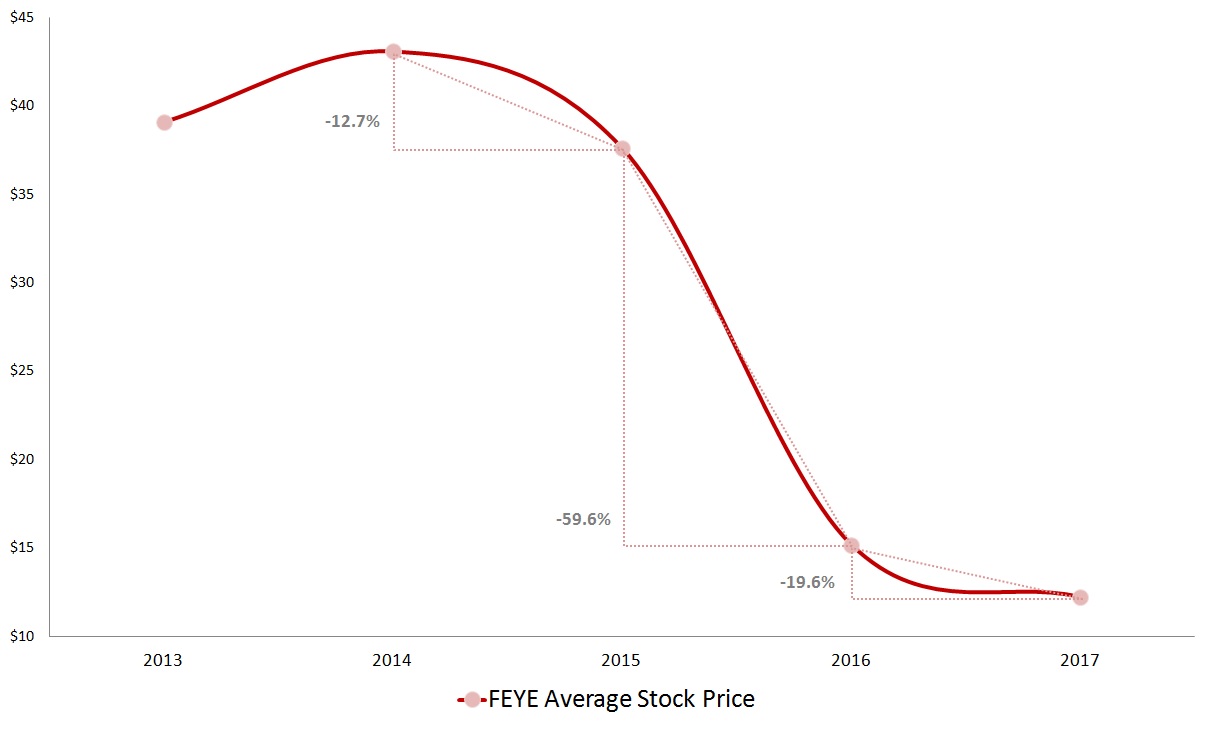

To confirm this point, FireEye stock started off with great fanfare. Investors were initially enthused by its robust momentum. But quickly, FEYE stock began to lose favor. Indeed, when you look at the organization topically, it has never returned a profit for the year. And no, I’m not going to include their extremely shortened 2013 debut.

When you look at analyst coverage overall, you’d be hard-pressed to find anybody sticking their neck out for FireEye stock. Jeff Reeves, executive editor of InvestorPlace, summed it up unambiguously when he wrote, “FEYE Stock Has Crashed for Good.” This was written in early August of 2016. Since then, FEYE has lost nearly 25% in the markets.

Cybersecurity Is Big Enough for FEYE Stock

So is there any hope for this long-embattled company? At first, the fundamentals don’t look so hot for FEYE stock. As InvestorPlace writer and IPO Playbook editor Tom Taulli notes, FEYE’s most recent earnings report was terrible. More ominously, their guidance for the first quarter is pedestrian, to say the least, and FireEye stock subsequently got pounded.

Competitively, FEYE has to go up against two tailwinds. Primarily, they were late to the game in terms of cloud integration, so they have some catch-up to do. On the broader front, the company faces serious pressure from industry leaders Palo Alto Networks Inc (NYSE:PANW) and Fortinet Inc (NASDAQ:FTNT).

However, FEYE stock also has to watch out for old guard firms like Microsoft Corporation (NASDAQ:MSFT). They’ve got the resources to exercise their “mid-life crisis” of breaking into new sectors.

At the same time, we have to appreciate the scale of the cybersecurity landscape. According to Symantec Corporation (NASDAQ:SYMC) CEO Greg Clack, 39% of North American residents have been impacted by cybercrime in 2016. In his words, “I think that’s a very big crisis.” Naturally, Mr. Clack is thinking specifically of his organization’s solutions. But the reality is that FEYE has a solid chance of making up for lost ground.

Furthermore, con artists are constantly getting creative with their nefarious activities. Many of these are exposed by government watchdogs, but by that point, the con is long gone. You can only imagine the possibilities with cybercrime. So yes, FEYE stock looks absolutely terrible now, I’ll concede. But due to the evolving nature of cybercrime, it’s risky to assume that FireEye stock will forever be a dud.

The Worst for FireEye Stock Is Behind It

Based on the actions of investors, I think the company is in the early stages of a turnaround. Long-term, the magnitude of volatility in FEYE stock is slowing significantly.

Click to Enlarge

Another interesting point is that shares could have fallen much further than it did. Everyone agrees that 2016 was a choppy period for FEYE, yet the lowest closing price last year was $11.01.

Presently, the average close is 11% higher than this figure. Also, its present market value is only a few cents shy of 2016’s closing low. That’s not a great statistic, I know. But it leaves the impression that the worst of the volatility may be over.

My final contrarian argument is that we’re not dealing with a fly-by-night operation. FEYE CEO Kevin Mandia was a former U.S. Air Force intelligence officer, and is widely considered a cybersecurity expert. This is not someone that is going to jeopardize his reputation on a whim. I’d also give FireEye stock a higher chance of success based on this much-needed, highly demanded industry.

Ultimately, I understand the hesitation of FEYE stock. It has simply lost too much value to be termed a stable investment. But for those with some risk capital to play with, FireEye stock is a compelling bet. The market losses are being pared, and you have substantial intellectual firepower on the executive team.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.