Some say betting with Warren Buffett puts an investor in pretty good arms. At any rate, investing alongside the Oracle from Omaha will at least ensure that a company has been properly vetted by one of the world’s best investors. International Business Machines Corp. (NYSE:IBM) is a holding of Buffett’s, but does that mean investors should buy IBM stock, too?

IBM is the now the fifth-largest position in Buffett’s Berkshire Hathaway Inc. (NYSE:BRK.A, NYSE:BRK.B) portfolio. After he aggressively bought millions of shares of Apple Inc. (NASDAQ:AAPL) in the first quarter, IBM is now his second-largest tech holding.

Not many would argue against owning Apple, but IBM stock is a different story.

A Closer Look at IBM Stock

IBM stock isn’t particularly attractive on a number of fronts. While its A.I.-based Watson product and move toward the cloud shows hope, there’s not much else to be optimistic about.

Analysts expect revenue to decline 1.6% this year and 0.1% in 2018. That may not seem that bad, if not for one additional fact: Its revenue decline isn’t an anomaly, it’s a trend.

Analysts expect sales of $18.39 billion when IBM reports earnings on Tuesday after the close. Given the same quarter last year generated revenues of $18.68 billion, that would mark another year-over-year decline in revenue. Assuming this comes to fruition, it will mark the 20th consecutive quarter of revenue declines!

Yeah, just think about that one for a minute.

While net income hasn’t been too robust over the years, IBM has become known for its big share repurchase plan. However, that hasn’t boosted per-share earnings the way many had thought it would.

For the current quarter, analysts are looking for flat EPS growth. On the year, they expect 1.4% EPS growth and 2.5% EPS growth in 2018. Again, far from flattering. Now it makes sense why IBM stock trades at 13.8x last year’s earnings and just 12x forward earnings estimates.

In fact, it’s hard to argue with those who believe IBM stock should trade with an even lower valuation considering its unimpressive earnings growth, putrid sales growth and seemingly endless transition to faster growth.

While IBM’s business is a slow-chugging train, it’s not the worst one on Wall Street. In fact, IBM does have a few positives. Although we said an argument could be made for a lower valuation, even at current prices, IBM stock isn’t trading at a premium price.

Trading IBM Stock

We wouldn’t buy IBM for the valuation alone per se, but it’s nice to buy a company that’s trading at a low valuation. Second, IBM stock pays out a 3.3% dividend yield. In a world where interest rates are so low, finding a low valuation stock with an attractive yield is suitable for certain income investors.

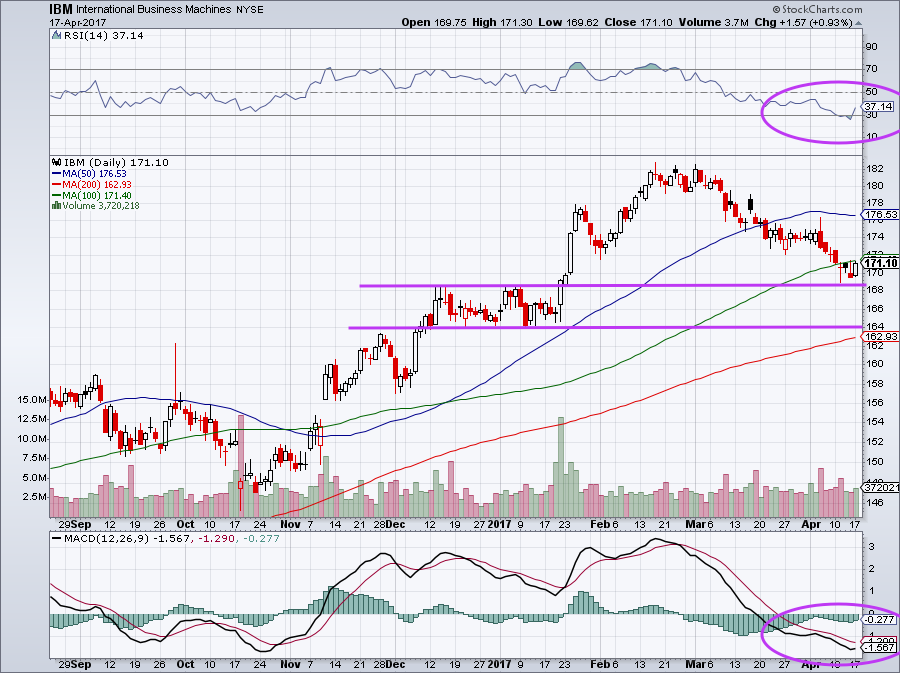

Shares have been pulling back as IBM stock is down about 6% from its 52-week high around $183. Shares have steadily fallen since the beginning of March, reducing the risk of a pullback following the company’s earnings release.

Click to Enlarge

For bullish investors, they could justify a trade in IBM. There are several support levels below current prices, starting with the $168 and $164 levels.

Below that is the 200-day moving average at $162. Additionally, the Relative Strength Index (RSI) shows an oversold bounce may be underway. Finally, the MACD measurement at the bottom of the chart shows a further bounce could be on the way.

It’s notable that IBM stock could be in play for a bounce. But to justify owning it longer term, we need a business that has growing revenue and better EPS growth.

Apple trades at a slightly higher valuation, but with far superior revenue and EPS growth. That makes for a better investment between the two.

That said, IBM is a Buffett stock with a solid dividend yield and a steady (albeit unimpressive) business. For some investors, this low valuation stock makes for an attractive income opportunity.

Bret Kenwell is the manager and author of Future Blue Chips. He can be contacted on Twitter via @BretKenwell. As of this writing, Bret Kenwell held no positions in any security mentioned.