How to Manage the Risk in REITs

by David Fabian | May 22, 2013 11:30 am

Whenever I hear the phrase “low volatility” mentioned, I rarely think about the real estate sector that underwent tremendous price compression during the 2008 financial crisis. However, over the last year we have witnessed a new trend emerge in real estate investment trusts that defies the volatility perception.

This asset class has been in a steady uptrend with very little fluctuation which may be an ominous sign of complacency among investors that are seeking a steady income stream. As I wrote back in April[1], REITs are offering investors attractive dividend and capital appreciation opportunities, but how long this trend will continue remains to be seen.

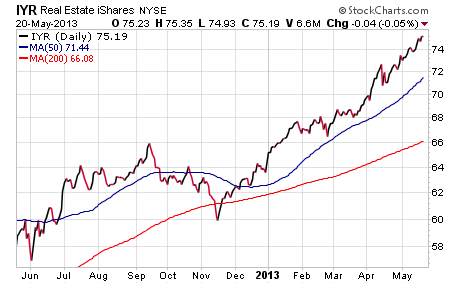

The largest ETF in this sector is the iShares U.S. Real Estate ETF (IYR[2]) which controls over $5.7 billion in total assets invested in 94 publicly traded REITs. So far this year IYR is closely pacing the gains of the S&P 500 Index with a total return of 17.33% (through May 17). As you can see on the chart below, IYR has been consistently hitting new highs and investors have benefited from its strong momentum.

The primary driver behind the capital appreciation in this sector has been a rebound in real estate asset prices which has been a direct result of the loose Federal Reserve monetary policies and aggressive quantitative easing. Cheaper interest rates have stimulated continued expansion and investment in office, medical, and apartment complexes that these REITs directly control.

However, with increasing correlation to the equity markets and falling yields, REITs could be at risk of a wider sell off in the near future if stocks begin to falter. Right now IYR is 11% above its 200-day moving average which is one of the largest divergences I have seen for this ETF in the past three years. This could be a warning sign of an overbought sector that is ripe for a pullback.

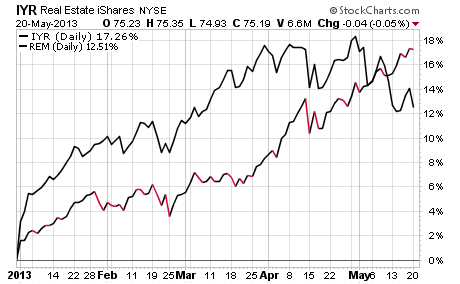

Another concern for the real estate sector is the recent underperformance of mortgage REITs, which had been previously leading their commercial REIT counterparts. The chart below shows the year-to-date correlation between IYR and the iShares Mortgage REIT Capped ETF (

REM[3]).

If you believe (as I do) that the stock market is overdue for a correction, then you might want to consider pairing back some of your exposure to IYR and other real estate funds to reduce your risk profile. It always makes more sense to make subtle changes to your portfolio during periods of calm, rather than having to make a snap decision when volatility returns.

Right now the price action in IYR is reminiscent of the top that we saw back in 2006 which was a precursor to a protracted bear market. While I don’t believe that IYR is going to see the same style of drawdown that we witnessed in 2008, I am hesitant to commit new money to REITs at these lofty levels. I would prefer to wait for a pullback to re-enter this space for my income clients[4] at more attractive valuations.

David Fabian is the Chief Operations Officer and Managing Partner of Fabian Capital Management. To get more investor insights from Fabian Capital, visit their blog here[5], or click here to download[6] their latest special report, The Strategic Approach to Income Investing.

- As I wrote back in April: http://fabiancm.com/real-estate-still-running/

- IYR: http://studio-5.financialcontent.com/investplace/quote?Symbol=IYR

- REM: http://studio-5.financialcontent.com/investplace/quote?Symbol=REM

- income clients: http://fabiancm.com/wealth-management/strategic-income-portfolio/

- visit their blog here: http://fabiancm.com/investor-insights/blog/

- click here to download: http://fabiancm.com/investor-insights/special-reports/

Source URL: https://investorplace.com/2013/05/how-to-manage-the-risk-in-reits-iyr-rem/