Marijuana Stock Hits a New High … and an Elite Dividend Pick Continues to Soar

If I didn’t know this before, reaction to our marijuana articles last week demonstrated that people have strong feelings on the subject.

As Jeff demonstrated so well last week, many are dead-set against it, regardless of what governments say about its legality.

Our position remains the same – we take no position on the morality of this trend, or any other. So long as it is legal, we are going to report on opportunities for investors.

And one of the ways our colleague Matt McCall has recommended for taking advantage of the marijuana megatrend has taken off.

It’s such a great example of the kinds of things Matt highlights in Investment Opportunities.

Too many investors think of trends too narrowly.

It’s as if an investment trend were a pebble dropped into a pool, and investors only think about the first few ripples. The effect of the first few ripples is obvious, but they keep going out, and have an influence you never consider.

Matt considers all the outer ripples, all the effects of an investment trend that many don’t consider. And he makes sure his readers get to the opportunities first.

And in August last year, Matt made a call many have never considered about the marijuana megatrend.

He advised his readers to invest in a marijuana REIT.

If you’re an active investor, you already know about the advantages of investing in REITs, or Real Estate Investment Trusts.

If you are not familiar with them, REITs are collections of real estate assets that trade as securities on the stock market. It’s a one-click way to own real estate assets and enjoy the income and capital gains that come with successful real estate projects.

REITs are required by law to distribute 90% of annual taxable net income via dividends to shareholders, and that money is taxed as ordinary income.

And yesterday the marijuana REIT Innovative Industrial Properties (IIPR) hit a 52-week high at $64.85. I’ve circled the point where Matt made his buy call.

Here is what Matt said when he made the call, and the stock was trading at $33.70.

IIPR is one of the first to see and take advantage of the opportunity in helping marijuana companies with the growing process. Founded in December 2016, the company made its IPO that same month on the New York Stock Exchange. IIPR was the first publicly traded U.S. company to provide real estate capital to the medical marijuana industry.

I love IIPR’s business model. The company buys freestanding properties from medical marijuana growers that are – and this is key – already approved by their respective states. IIPR then leases the properties right back to the growers under a long-term agreement. This gives the growers an infusion of capital to expand their operations and increase production. In return, IIPR receives regular rent payments under a long-term lease.

That is a brilliant business model for a nascent industry. And more and more states are continuing to legalize the product.

Plus, the stock pays a nice dividend too.

Investing in new trends can be unnerving.

Stocks can go up and down with the news until the market change takes firm hold.

That makes IIPR a relatively low-risk way to get in on the trend.

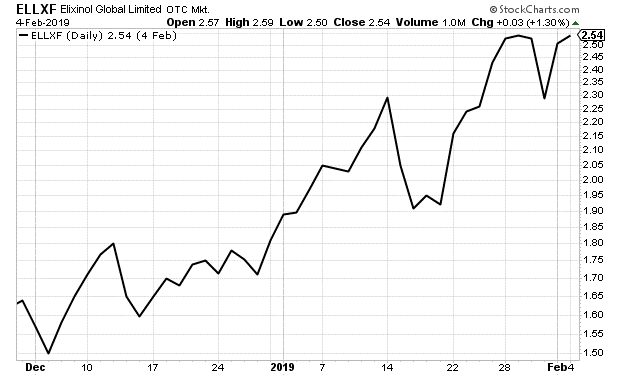

As I shared with you last month, Matt made a specific call Dec. 4 for one of these companies — Elixinol Global Limited (ELLXF).

Since he made that call, the stock is up 69%.

Matt is still identifying the new marijuana businesses that have the potential to make similar gains. In fact, he is going to pick another one for his subscribers on Feb. 19.

Click here to find out more about how he finds them, and when he is making his next big pick.

Meanwhile, a Louis Navellier Elite Dividend Pick also hit a 52-week high

I’ve written numerous times about keeping your eye on market fundamentals.

The 24-hour news cycle can present a lot of buzzers, bells, and flashing lights.

But we are now just about midway through earnings season and we’ve got a much better sense about a lot of the stocks we follow.

Earnings season is big for us since we prefer to focus on fundamentals.

And Louis Navellier, editor of Growth Investor, is especially good at keeping his eye on what matters.

I’ve spoken before about his Portfolio Grader and all the variables he uses to determine which stocks to buy when. For example, he grades stocks on eight factors including earnings growth, earnings momentum and earnings surprises.

Louis also offers a Dividend Grader. Using this free tool, you can see how a dividend stock such as Boeing is graded based on several factors such as reliability, growth and earnings yield.

Just last week, earnings from one of the stocks in his portfolio proved why it’s still a buy.

One of the standouts of this earnings season is The Boeing Company, a stock Louis has kept in his portfolio since mid-October of 2017.

Yesterday, the stock hit a 52-week high. In the chart below, I circled where Louis advises his readers to buy.

Last week, Louis explained why the company’s shares continue to climb.

The Boeing Company (BA) climbed about 6% higher this week, following the company’s record fourth-quarter and full-year results. First, during the fourth quarter, revenue jumped 14% year-over-year to $28.3 billion, up from $24.8 billion in the same quarter a year ago. Analysts were expecting revenue of $26.87 billion.

Fourth-quarter operating earnings soared 49% year-over-year to $3.87 billion, or $5.48 per share, compared with $2.59 billion, or $5.07 per share, in the fourth quarter of 2017. The Street view was for $4.58 per share, so Boeing posted a 19.7% earnings surprise.

Boeing also set a new revenue record for fiscal year 2018, reporting $101.1 billion. That represented 8% annual revenue growth. Full-year earnings per share were $8.91 billion, or $12.33 per share. Company management also noted that it paid $3.9 billion in dividends during the year.

Looking forward to fiscal year 2019, Boeing expects revenue between $109.5 billion and $111.5 billion, and earnings per share between $19.90 and $20.10. The company also anticipates that it will deliver between 895 and 905 commercial aircraft this year, or an 11% to 12.3% increase over the 806 aircraft delivered in 2018.

Clearly, 2018 was a stunning year for Boeing, and the company expects 2019 to be even better. BA remains a solid buy on dips below $393.

So, why is Boeing doing so well? InvestorPlace Contributor Luke Lango noted in his article “Here’s Why Boeing Stock Will Run up to All Time Highs in 2019,” that the company is well entrenched in several secular growth industries.

On the airline front, global travel demand is expected to surge over the next 20 years due to global urbanization and a shift towards an experience-driven consumer economy that values travel. As this demand grows, demand for new equipment will increase, too, and Boeing’s airplane numbers will only get bigger.

Meanwhile, defense spend is another thing that won’t go away anytime soon. While it may be volatile depending on the geopolitical situation, defense spend won’t ever dry up or drop in a big way. Instead, it will grow fairly consistently with the broader global economy.

When it comes to space, investment into commercial space travel will only pick up over the next several years, thanks to improving technological capabilities and growing consumer interest in space travel. This growing interest will inevitably push Boeing’s numbers higher. Also, the air mobility market is a highly undervalued and underappreciated aspect of Boeing that could provide a huge boost to BA stock.

With its reach into such a broad range of secular growth industries that won’t slow in the foreseeable future, Boeing’s growth trajectory should remain healthier for longer.

Earnings for stocks are still very strong overall, but Louis has been clear that this is not a “rising tide lifts all boats” kind of market.

Boeing is a still a buy on the dip, so add it to your watch list.

This is just the kind of stock that Louis has predicted would surge this year. He has made more picks about the kinds of stocks that will surge in a much narrower market, and you can see his presentation about them here.

To a richer life…

Luis Hernandez, Managing Editor

and the research team at InvestorPlace.com