These five high yield drug stocks pay dividends with attractive yields, and also are undervalued. And as a result, these stocks offer good upside potential to investors. As a group, they are cheap. Yet, they have solid earnings that cover their dividends, plus good growth prospects.

I wanted to find these high-yield drug stocks since there is a lot of news out there about pharmaceutical companies that are trying to find a vaccine. I figured some of these larger drug companies can be both innovative and also have a diversified level of income.

This helps the pharmaceutical company satisfy the return objectives of its existing investors. However, they also offer enough growth prospects to provide upside potential for new investors.

For example, the average upside of this group of drug stocks is over 38%. Yet, the average dividend yield is 4.1% and the average price-to-earnings ratio (P/E) is just 12.5 times. This is for earnings estimated for fiscal year 2021, and it is very cheap.

That said, the five high yield drug stocks are:

- AbbVie (NYSE:ABBV)

- GlaxoSmithKline (NYSE:GSK)

- Novartis (NYSE:NVS)

- Pfizer (NYSE:PFE)

- Sanofi (NASDAQ:SNY)

So, with all of that in mind, let’s dive in.

High-Yield Drug Stocks: AbbVie (ABBV)

Click to Enlarge

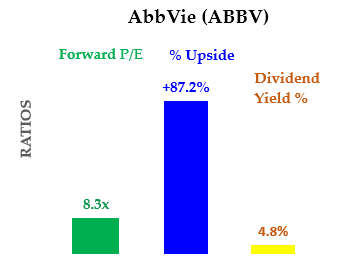

Market Value: $170 billion

Forward P/E: 8.3x

Dividend Yield: 4.8%

Target Price Upside: 87%

AbbVie stock is a large $170 billion market capitalization drug stock that is both cheap and has a very attractive dividend yield. In addition, its growth prospects are high. In fact, it recently closed on the $63 billion acquisition of Allergan.

Allergan is well known for its Botox and other beauty products. In turn, the deal will help AbbVie diversify its earnings and “buys time” before its arthritis drug Humira goes off-patent in 2023.

Overall, that is why AbbVie is so cheap. It accounted for over 54% of the company’s sales as of first quarter of FY2020. The market assumes that generic drugs will eventually overtake that revenue stream for AbbVie, but things are not as bad as that.

With Allergan, Humira will account for only 38.4% of sales. And given that other drugs in AbbVie’s portfolio are likely growing faster than Humira, that portion will continue to fall.

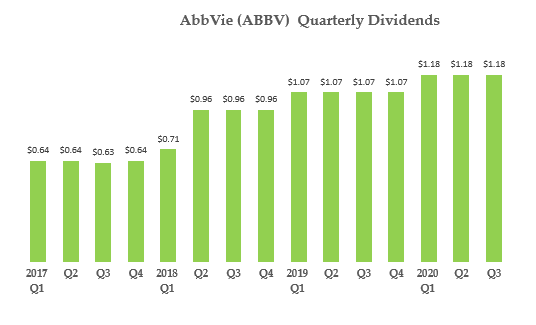

Moreover, ABBV stock has a history of paying consistent quarterly dividends that tend to rise each year. You can see this in the chart here.

Click to Enlarge

Based on my analysis of the stock, it is worth at least 81% more than today’s price.

For example, the company’s historical yield over the last four years is 4.22%. Given today’s yield of 4.8%, that implies AbbVie stock is worth almost 15% more than today.

Also, based on its historical P/E ratio, the stock is worth over double today’s price. And lastly, based on a comparison with its peers, the stock should have an 80% higher price. Averaging these three methods, AbbVie stock is worth $182.30, or 87% more than today.

Therefore, ABBV stock is one of the top drug stocks available.

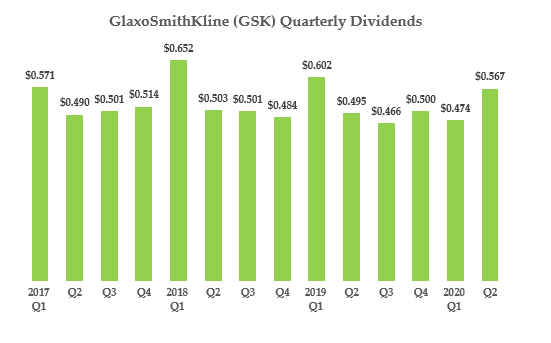

GlaxoSmithKline (GSK)

Click to Enlarge

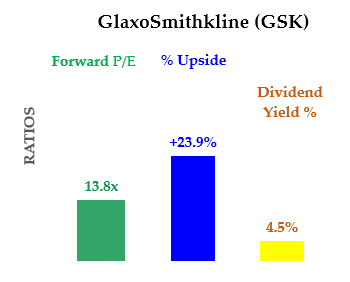

Market Value: $100 billion

Forward P/E: 13.8x

Dividend Yield: 4.5%

Target Price Upside: 24%

GlaxoSmithKline is the world’s largest vaccine maker, and the UK-headquartered company is relying on proven methods of making a vaccine. In fact, Reuters says it prefers the “slow and steady approach of focusing on an established technology that has the best chance of reaching the widest possible demographic.”

They recognize that the world will need billions of doses, and therefore are not worried if they are first to market with a vaccine. Many other vaccine makers will not have the capacity to match what GlaxoSmithKline can do quickly. And once its vaccine is ready — which, only started its trials in June — it can make large amounts.A

Additionally, GlaxoSmithKline believes its vaccine will have better efficacy and last longer. This may mean it can work better with the elderly.

As Barron’s points out, the company has a huge pipeline of drugs, including options for cancer and HIV prevention. GlaxoSmithKline also plans on spinning off its consumer health division, which makes Advil and Panadol.

Moreover, GSK stock has a history of paying consistent quarterly dividends that tend to have a higher year-end dividend each year. You can see this is true in the chart here.

Click to Enlarge

So, based on my analysis of the stock, it is worth at least 24% more than today’s price.

For example, the company’s historical price-to-earnings over the last four years is 25 times. Given today’s P/E ratio of 14 times this year and 13.8 times next year, that implies GSK stock is worth almost 84% more than today.

And lastly, based on a comparison with its peers, the stock should be much higher. Averaging three valuations methods, GSK stock is worth $51.51, or 24% more than today.

Collectively, GSK stock is another one to keep your eye on.

Novartis (NVS)

Click to Enlarge

Market Value: $194 billion

Forward P/E: 14.1x

Dividend Yield: 3.6%

Target Price Upside: 17%

Novartis, a Swiss company, owns Sandoz, a well-known drug company. Sandoz plans on giving away 15 of its generic drugs that treat symptoms of COVID-19 to developing countries. In June, it agreed to $729 million in fines with the U.S. government to settle charges it paid kickbacks to doctors and patients.

Moreover, Novartis will start a Covid-19 clinical trial of their cancer drug, Jakafi, which was developed by Incyte Corp.(NASDAQ:INCY). In turn, Novartis sells the drug outside the U.S. Barron’s recently described the use of this cancer drug for a Covid-19 trial, and how Jakafi could help patients suffering severe immune overreactions caused by Covid-19.

Novartis and Incyte have a Phase 3 trial, comparing those who use it with Covid-19 and those with Covid-19 who don’t. The drug could eliminate hospital intensive care and mechanical breathing assistance. In fact, this drug is one of many in the category of existing drugs that could potentially act as a treatment for Covid-19.

Investors should also consider its attractive 3.6% dividend yield. NVS stock has consistently paid annual dividends that reflect its profitability,and you can see this in the chart.

Click to Enlarge

Therefore, based on my analysis, it is worth at least 17% more than today’s price.

For example, its historical price-to-earnings over the last four years is 21 times. And given today’s P/E ratio of 14 times this year, NVS stock is worth almost 46% more than today.

Finally, based on a comparison with its peers, the stock should be much higher. Averaging three valuations methods, NVS stock is worth $100.62, or 17% more than today — making NVS stock another great drug stock.

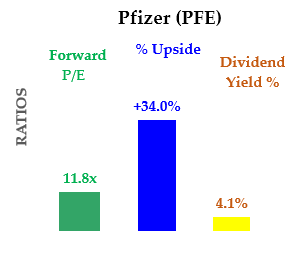

Pfizer (PFE)

Click to Enlarge

Market Value: $204 billion

Forward P/E: 11.8x

Dividend Yield: 4.1%

Target Price Upside: 34%

Pfizer recently indicated that its Covid-19 vaccine trials will be rolled out very quickly. On that note, Barron’s reported that analysts believe the aggressive timeline was “laudable, but seems challenging.” One analyst believes that the positive vaccine data and the trial timeline will act as a “catalyst” for PFE stock.

Moreover, Pfizer is working in collaboration with a German company, BioNtech (NASDAQ:BNTX), on this vaccine. And according to Barron’s, all 24 patients who received lower doses of the vaccine developed levels of neutralizing antibodies after 28 days. These levels were about two times higher than those found in patients who have recovered from the coronavirus.

On July 13, the FDA gave the companies’ vaccine trial a “fast track” status. The two vaccines, BNT162b1 and BNT162b2, could get “priority review” leading to approval within six months. By comparison, Moderna (NASDAQ:MRNA) which uses similar technology, according to Reuters, got this fast track status in May.

Nevertheless, this could why PFE stock has been rising. There are also valuation-related reasons to buy the stock.

PFE stock has a history of paying consistent quarterly dividends that tend to rise each year. You can see this in the chart here.

Click to Enlarge

Based on my analysis of the stock, it is worth at least 34% more than today’s price.

For example, its historical yield over the last four years is 3.77%. And given today’s yield of 4.1%, PFE stock is worth almost 10% more than today.

Averaging three valuation methods PFE stock is worth $49.15, or 34% more than today.

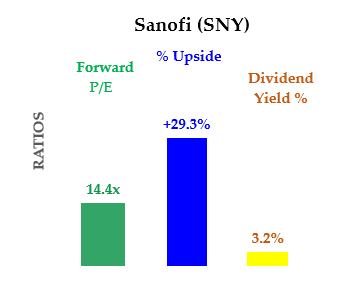

Sanofi (SNY)

Click to Enlarge

Market Value: $134 billion

Forward P/E: 14.4x

Dividend Yield: 3.2%

Target Price Upside: 29%

Sanofi is also in the Covid-19 vaccine race as well. In late June, Sanofi partnered with another company, Translate Bio (NASDAQ:TBIO). The companies have worked together before, and use a messenger RNA technology like Moderna and Pfizer/BioNTech for their Covid-19 vaccine drug. In turn, this technology induces antibodies for a specific protein related to the novel coronavirus.

Also, Sanofi’s Pasteur division is going to spend $1.9 billion to get a vaccine by mid-2021, with trials are expected to start in Q4. Therefore, Sanofi offers both capital and a huge vaccine manufacturing capability to Translate Bio.

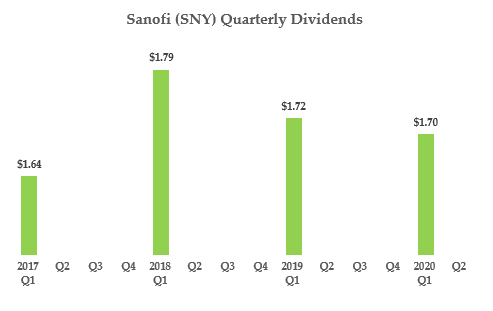

Moreover, SNY stock has a history of paying consistent annual dividends that reflect its profitability each year. You can see this in the given chart.

Click to Enlarge

So, based on my analysis of the stock, it is worth at least 29% more than today’s price.

For example, its historical price-to-earnings over the last four years is 40 times. Given today’s P/E ratio of 35 times this year and 14.4 times next year, SNY stock is worth almost 43% more than today.

Lastly, based on a comparison with its peers, SNY stock should be 6 to 7% higher. Averaging three valuations methods, SNY stock is worth $68.80, or 29% more than today. And with all of that in mind, PFE is one of the best drug stocks on the market.

Summary: High Yield Drug Stocks

These high yield drug stocks are admirable in that most of them are developing Covid-19 vaccines. In addition, they also have attractive dividends with attractive upside potential.

Overall, these are not day trades or momentum stocks. On the other hand, though, they are solidly profitable and can afford their high-yield dividends. They are likely to reach their target upside.

Moreover, this chart sows that the average dividend yield is 4.1% for this group of stocks. They also boast a low average P/E at 12.5 times, and offer a potential upside of almost 38%. That is a very respectable ROI for most investors.

Therefore, for these reasons, these five high-yielding drug stocks could be great options for investors.

Mark Hake runs the Total Yield Value Guide which you can review here. The Guide focuses on high total yield value stocks. Subscribers receive a two-week free trial.As of this writing, Mark does not hold a position in any of the aforementioned securities.