I wanted to find five food and beverage stocks that pay consistent dividends and that are also undervalued. The idea is that these stable companies can provide consistent returns for value investors despite the popularity of momentum stocks.

It turns out that the five stocks I found have very attractive value features. For example, the average dividend yield of this group is 2.6%.

Moreover, each of these companies has been consistently paying dividends even during the pandemic-induced recession. Some have even increased their dividends or are set to increase their dividends.

In addition, these stocks are cheap and have good upside potential. For example, the average price-earnings ratio is 13 times. In addition, my estimate for each stock’s target value is on average 38% higher than today.

The most fundamental reason to invest in food and beverage stocks is that the underlying business tends to be stable. Everyone needs to eat and drink. The companies tend to have consistent growth as well. This feeds through into the dividends the companies pay. With this in mind, here are five food and beverage dividend stocks to buy:

- Coca-Cola (NYSE:KO)

- Constellation Brands (NYSE:STZ)

- Kraft Heinz (NASDAQ:KHC)

- J.M. Smucker (NYSE:SJM)

- Tyson Foods (NYSE:TSN)

Let’s dive in and look at these stocks.

Food and Beverage Stocks: Coca-Cola (KO)

Click to Enlarge

Market Capitalization: $208 billion

Everyone knows this popular beverage company. Everyone loves one — or several — of its beverages. As a result, Coca-Cola’s main attribute is that it is consistently profitable.

Coca-Cola just emerged from a tough quarter where its global unit case volume declined 16%. Net revenues fell 28% and operating income dropped 34%. But that information is already in the stock price.

The good news is that things are now already improving. The company’s reported case volume for June is now down only 10% year-over-year. Moreover, although analysts expect earnings per share to fall this year to just $1.82, they also expect EPS to rise to $2.06 next year.

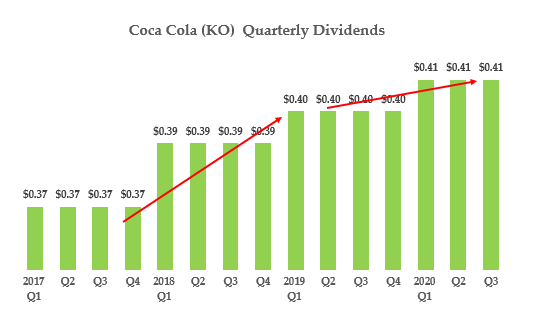

In addition, the $1.64 dividend per share is still covered by earnings. It’s also expected to rise after the next upcoming quarterly dividend payment.

Click to Enlarge

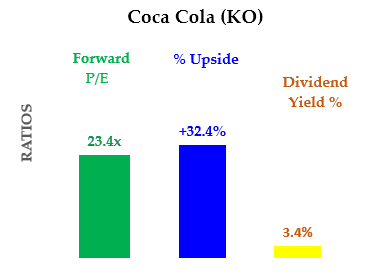

You can see this on the table at the right. KO’s 3.4% dividend yield is also slightly below the historical average of 3.36%.

KO stock is worth at least one third higher than its present price. The $64.18 price target was derived by averaging three different methods. The first is the historical dividend yield method.

The second is based on the stock’s historical P/E record. Its average P/E has been 38 times over the last five years. The implied target price is therefore 62% higher.

The last method is based on peer P/E ratios. The P/E of 31.4 times for its peers is 34% higher than Coca-Cola’s. KO stock is therefore worth 32% more than today’s price.

Constellation Brands (STZ)

Click to Enlarge

Market Capitalization: $35 billion

Constellation Brands produces and imports beer and wine in North America, Italy and New Zealand. Its iconic beer brands include Corona Light, Modelo and Victoria. It has seven wine brands and spirits such as Svedka. In addition, Constellation Brands has a 37% stake in Canopy Growth (NYSE:CGC), a Canadian cannabis company.

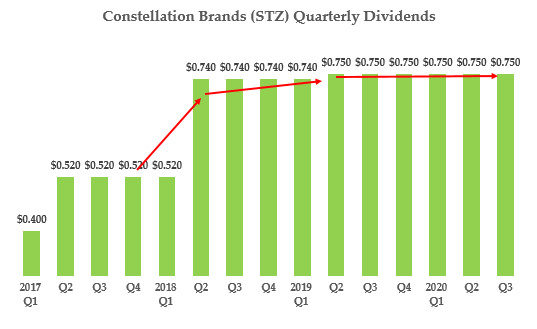

Constellation’s fiscal Q1 actually showed positive comparable EPS growth, despite lower volumes in beer and spirits. In addition, its cash flow growth was positive as well. This is quite an achievement.

Moreover, the company maintained its steady dividend, as you can see in the chart at the right.

Click to Enlarge

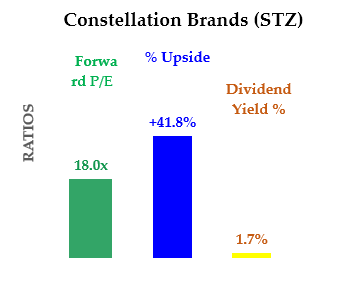

For the past six quarters, the company has paid the same dividend, giving STZ stock a 1.7% dividend yield.

My estimate is that the stock is at least 42% undervalued. This is based on the same three methods used above. For example, the company’s historical dividend yield is lower than today at 1.26%. The historical P/E is higher at 22 times, against today’s 18 times. And its peer comp P/E ratio is 30 times.

As a result, STZ stock is worth 42% more at $255.01 per share. Simply put, people are still drinking brand-name beer and wine, recession or not.

Food and Beverage Stocks: Kraft Heinz (KHC)

Click to Enlarge

Market Capitalization: $42.5 billion

Kraft Heinz has had it for rough several years. The company makes condiments and sauces, cheese and dairy, meals, meats and seafood. Behind all of those products is an iconic brand. Earnings fell in 2019 to just $1.9 billion from over $10.9 billion a year earlier. Brand write-downs and falling sales didn’t help.

Earnings were down 6.7% year-over-year in the first quarter. Earnings and dividends for Q2 will be released on July 30.

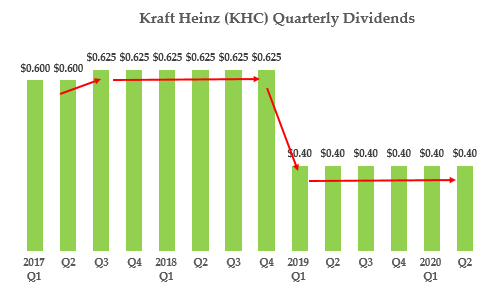

The company has paid a reduced quarterly dividend ever since early 2019. You can see this in the chart at the right. This chart shows that the quarterly dividend is 40 cents per share, giving KHC stock an attractive dividend yield of 4.6%.

Click to Enlarge

Based on my analysis, the stock is worth at least 31% more than the present price. As a result, the target price is $45.52.

For example, the company’s average dividend yield in the past four years has been 4.6%. This is where the stock is today. However, KHC’s average historical P/E ratio has been over 19 times. This compares with its present 14.7 times cheap valuation.

In addition, its peer comparable P/E ratio is 23.6 times. This means that based on this measure, the stock is worth over 60% more than today.

Averaging these three methods yields upside potential of 31%.

J.M. Smucker (SJM)

Click to Enlarge

Market Capitalization: $12.4 billion

The J.M. Smucker Company makes pet foods, premium coffee, peanut butter and specialty fruit spreads under a number of iconic brands. These brands include Smucker’s spreads, Jif peanut butter, Folger’s Coffee, Meow Mix, Kibble ‘N Bits and Milk-Bone.

Revenue and earnings have been growing consistently higher, despite the recession. Revenue for its fiscal fourth quarter grew 10% year-over-year. For the year ending April 30, revenue was still 1% higher, despite the recession. Moreover, adjusted earnings per share grew by 24% for the quarter and up by 6% for the year ending April 30.

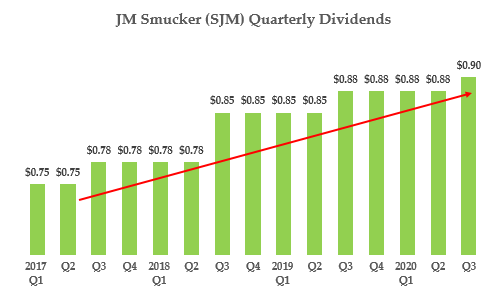

Therefore, the company decided to increase its quarterly dividend. It is probably one of the few companies that have recently done this. The company has grown its dividend every year for the past 19 years.

Click to Enlarge

The chart at the right shows that the company raised its dividend to 90 cents per share after paying 88 cents for four quarters. Investors can likely expect another dividend increase in another year.

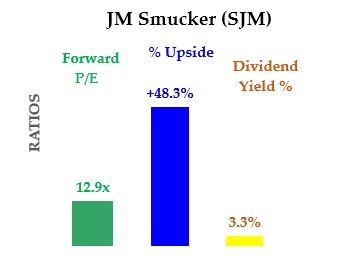

Moreover, I estimate that SJM stock is clearly worth at least 48% more than its present price. For example, the dividend yield over the past four years has been 2.8%, whereas today the yield is still 3.3%. Therefore, if this dividend stock rose to its average dividend yield, it would gain over 17%.

In addition, its average historical P/E ratio is 18.6 times, or 18% higher than today’s 12.9 times P/E ratio. Lastly, the peer P/E ratio is also higher at 23.8 times.

Therefore, the average upside of all these three methods is a target price of $160.41. This is potential upside of over 48%.

Food and Beverage Stocks: Tyson Foods (TSN)

Click to Enlarge

Market Capitalization: $22.2 billion

Tyson is a large protein food company with many popular brand names like Jimmy Dean, Tyson, Hillshire Farms and Ball Park. The company has enjoyed relatively stable growth in revenue and earnings.

However, although revenue was up in the quarter ending March 31, its adjusted earnings fell 36% from the prior year. Some of its plants were affected by shutdowns from the effects of Covid-19.

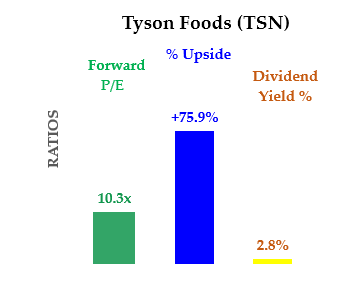

Analysts expect the company’s earnings to grow over 30% in the next year. The stock trades at just 10.3 times next year’s earnings and has a 2.8% dividend yield.

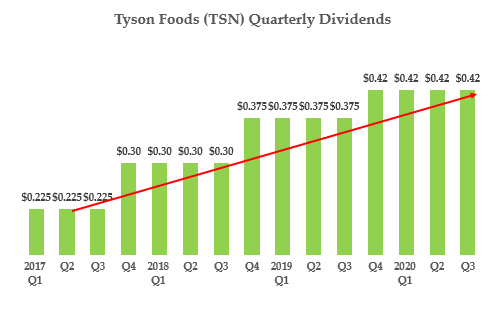

Click to Enlarge

The chart at the right shows that the quarterly dividend has been consistently growing over the past four years.

The most recent dividend was declared on May 8, so the next announcement — which may include a quarterly increase — will likely come around Aug. 7 or Aug. 8.

The average dividend yield in the past four years was 1.7%. It’s worth over 66% more since its yield today is 2.8%. The average P/E ratio has averaged 13.4 times over the past five years. Therefore, the stock should be over 30% higher.

Moreover, its comp peer-based P/E ratio is 23.8 times. This implies that it’s worth 131% more than today. Averaging these three methods yields a target price of $106.98 for TSN stock, up 76% above today’s price.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide, which you can review here.