When it comes to investing, it helps to be a straight shooter (and a bit of an optimist). But let’s call it for what it is: FAANG stocks, Facebook (NASDAQ:FB) included, have not been doing very well lately. In fact, FB stock stock is down about 12% from its high about a month ago.

At its recent low, shares were down even more, off nearly 20% and flirting with the so-called bear market territory.

However, here’s where being an optimist comes in handy. Rather than wallow in those losses and bemoan Facebook stock as a loser — it’s actually up 22.4% on the year and up 83% from the March lows — why not use the dip as an opportunity?

Strong Fundamentals for Facebook Stock

Click to Enlarge

First and foremost, the fundamentals for Facebook stock remain strong.

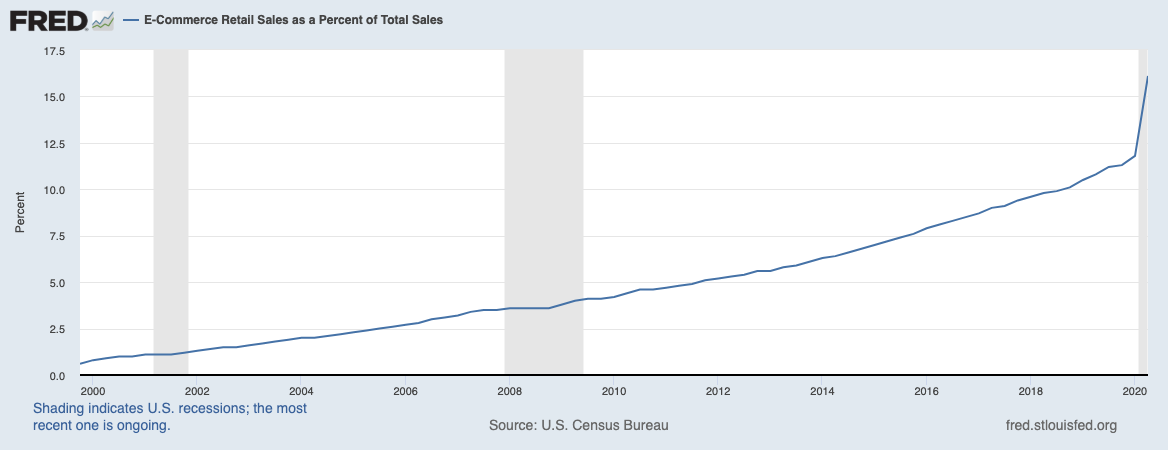

The novel coronavirus triggered a massive disruption. Aside from the volatility in the stock market and impact on the real economy, it drastically sped up online processes. Those processes include everything from streaming video, to video calls, to cloud use, to e-commerce sales.

That said, when e-commerce sales are flourishing, that has a direct impact on digital marketing and advertising. Tech stocks have done well, but business for Facebook and other social media companies has remained solid.

While revenue did dip hard in March and April, management told us that the lows were likely in. And although they were cautious, they were certainly optimistic about business moving forward. That was the conference call investors really needed to hear.

Get this: Despite a year of uncertainty, volatility and headwinds, Facebook is still forecast to grow. Do you realize how many companies and industries can’t say that?

Overall, the company is forecast to grow revenue 13.5% to $80.2 billion and grow earnings about 25% to $8.04 per share. Next year (fiscal 2021) is forecast to be an acceleration year. Consensus expectations call for 24% revenue growth and 26.5% earnings growth to $10.15 per share.

So, with or without a global pandemic, Facebook’s business is growing. And from an investors’ perspective, that’s all you can ask for.

Robust Financials

Investing during a pandemic has investors focusing on two main things: growth and stability.

Facebook answered the growth question already, but what about stability? Well, the simple answer is, this company is rock solid. And that goes for any of the three financial statements one cares to peruse.

The income statement — which houses revenue and net income, among other things — has already shown its resilience with the consensus estimates just highlighted. The balance sheet emphasizes strength, too.

Total assets of $139.7 billion are up almost 20% year over year and dominate total liabilities of $29.2 billion. The latter figure is up just 4.3% year over year. Cash and equivalents sit at $58.2 billion as of the most recent quarter, while Facebook does not carry any long-term or current debt other than capital leases.

In other words, “robust” barely does this balance sheet justice. Just after the quarter ended, Facebook did make a sizable investment, but not one that alters its financials too much.

In the press release, the company stated, “we paid approximately $5.8 billion at the then–current exchange rate for our investment in Jio Platforms Limited.”

Turning to the cash flow statement highlights more strength. There is nothing to love more than a high-margin growth company that can clear a ton of cash each quarter. In Q1, Facebook generated free cash flow (FCF) of $7.3 billion.

Last quarter was just $622 million, but included a $5 billion settlement with the FTC. Backed out, Facebook generated over $5.6 billion in FCF despite what was likely the most turbulent quarter in its history. Sign me up for that.

Facebook Stock Has Strong Technicals

Click to Enlarge

“Healthy? What do you mean healthy? Facebook stock is below the 10-day and 50-day moving averages. That’s not healthy!”

Some investors may concur with a statement like the one above. I view it differently, though. And while it’s true the stock is below these two key moving averages, it has been remarkably strong this year.

Facebook stock has outpaced the indices and has bombarded its way to new highs. Sure, it’s not breaking out to new highs right now but wouldn’t one rather buy a dominant business with solid growth and relative strength on a dip?

I know I would. The stock is holding up over its summer breakout level. And if it can reclaim the 10-day and 50-day moving averages, it puts the 161.8% extension in play in the short term, then $300-plus.

Even if current support wanes, this name is still healthy on a dip to the 200-day moving average and the prior pre-coronavirus highs.

Volatility in the market remains high and as a result, Facebook stock is susceptible to market swoons. That’s the same for any stock, though. Those swoons are long-term investors’ opportunities.

On the date of publication, the InvestorPlace Research Staff member primarily responsible for this article did not hold (either directly or indirectly) any positions in the securities mentioned in this article.