On Dec. 10, 2020, a SPAC (special purpose acquisition company) called TPG Pace Beneficial Corp. (NYSE:TPGY) announced a reverse merger with a European charging company EVBox Group. TPGY stock (the new symbol will be EVB after the merger) is worth at least 67% more at $49.32 when the SPAC merger closes.

EBVBox is Europe’s largest electric vehicle charging company, just like ChargePoint is the largest in the U.S.

Based on a comparison with ChargePoint, I estimate that TPGY/EVB stock is worth $7.6 billion or $49.32 per share fully diluted. This compares with its existing pro forma market value of $3.944 billion.

This article will explain how I came up with these calculations.

TPGY/EVB Pro Forma Market Values

Fortunately, most of the valuation analysis work is done by EVBox both in its Dec. 10 press release and in its accompanying slide presentation.

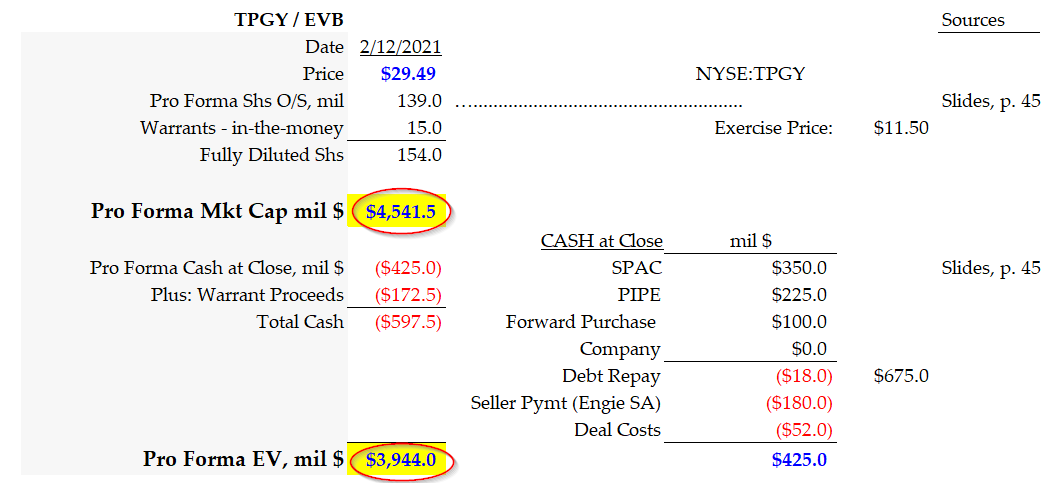

Since TPGY stock (EVB stock) was at $29.49 per share as of Feb. 12, we have to adjust some of the numbers. For example, on page 45 of the slide presentation, we can use the number of shares listed on a pro forma basis once the merger closes to set the pro forma market capitalization.

Click to Enlarge

We can use the total cash raised from the deal, minus the debt repayments and deal costs, to determine the pro forma enterprise value. In addition, I have added in the warrants which are all in-the-money. Those warrants will likely be called within several months after the merger and EVBox will receive the proceeds.

You can see this calculation in the table I have put together at the right. It shows that the pro forma market cap is now $4.54 billion and the enterprise value is $3.94 billion.

We can use these figures to find its enterprise value-to-sales ratios as well as its target market cap and price.

Adjusting the TPGY Stock (EVBox) Forecasts

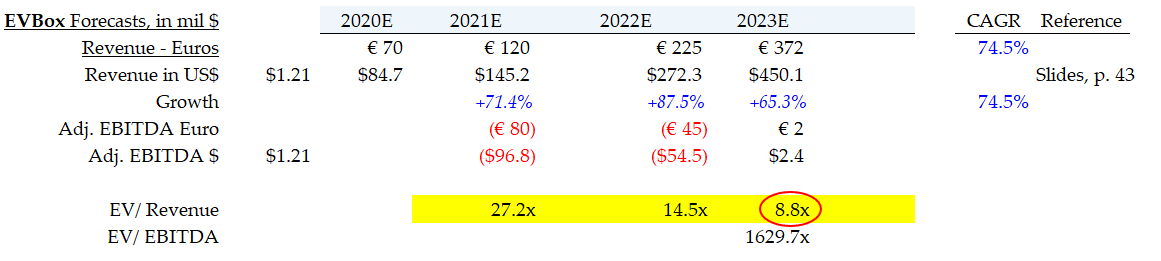

On page 43 of TPG’s slide presentation, the company presents EVBox’s revenue and adjusted EBITDA forecast. These go out to 2o23.

Looking closely at these numbers it is clear that EVBox Group expects its revenue to essentially go through the roof. They grow on average 74.5% annually over the next three years.

Click to Enlarge

In 2021, it forecasts 71% growth over 2020, but in 2022 that rises to 87.5% growth.

You can see this in the table I put together at the right. It shows that by 2023 revenue will be $450 million. This works out to an annual average growth rate of 74.5%. That is incredible.

You can also see in the table that by 2023 the enterprise revenue-to-sales multiple falls from 27 times in 2021 to just 8 times in 2023.

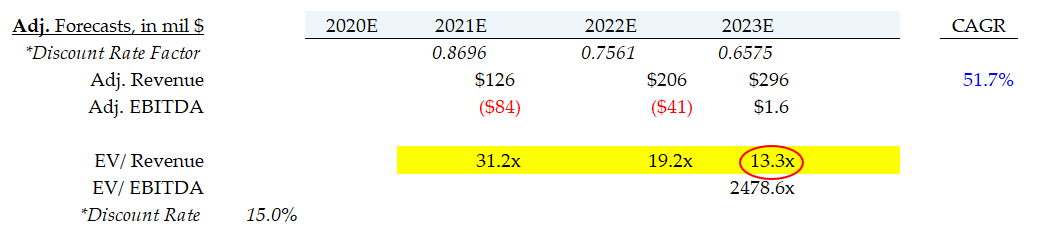

But we cannot use that ratio. It is simply too far out in the future. For one, any investor would want to have a hurdle rate or opportunity-cost rate. This covers the otherwise use of his investment money in EVBox waiting three years in the future.

In addition, we use a 15% discount rate to adjust for risk over the next three years.

Click to Enlarge

The next table on the right shows these adjusted revenue numbers.

This lowers both the absolute numbers so that by 2023 revenue is actually just $296 million, instead of over $450 million. The average annual growth rate falls to 52%. It also raises the 2023 enterprise value-to-sales ratio to 13.2 times.

Valuing TPGY Stock (EVB Stock)

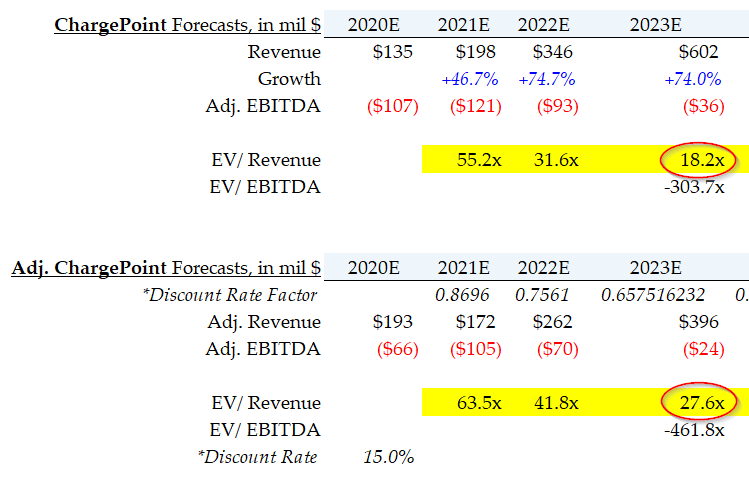

The best and simplest way to value EVBox is to compare it to ChargePoint, using Switchback Energy (NYSE:SBE) presentation numbers. In fact, on page 47 of the TPGY slide presentation, EVBox compares its growth with ChargePoint. Its growth rate to 2022 is expected to be 79% compound annual average growth (CAGR). But ChargePoint’s CAGR is only 60% over that period. This implies that EVBox should have a slightly higher premium.

We can use this when comparing the EVBox average enterprise value-to-sales ratios to ChargePoint’s multiples.

For example, the table at the right shows my analysis of ChargePoint’s enterprise value-to-sales ratios, including on an adjusted basis.

Click to Enlarge

Next, I apply these ratios to EVBox (TPGY stock).

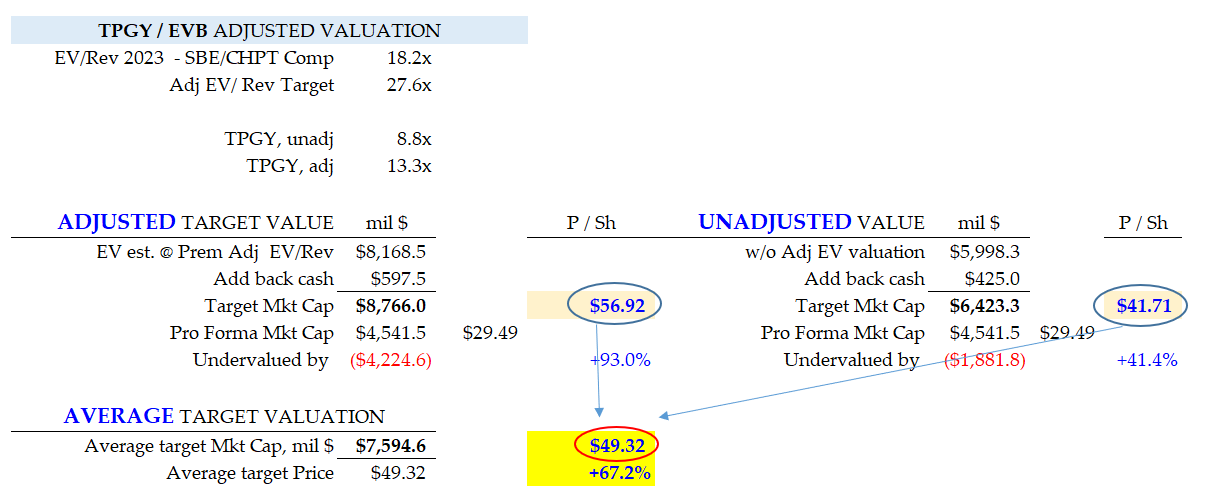

You can see the results of applying the ChargePoint EV-to-sales metrics to TPBY stock (EVBox) in the table on the right.

The adjusted target value, based on a 27.6 enterprise value-to-sales multiple from ChargePoint’s adjusted enterprise value-to-sales ratio, is $56.92 when applied to TPGY stock. That represents a gain of 93% from the recent TPGY price.

Click to Enlarge

However, the unadjusted target price, based on SBE stock having an 18.2 times enterprise value-to-sales ratio, is $41.71. That represents a gain of 41% over the Feb. 12 price.

Therefore, the average between the two numbers is $49.32 per share. This represents a potential gain of 67% from Feb. 12.

Therefore, TPGY stock is worth somewhere between a gain of 41% and a gain of 93%, or an average of $49.32 per share. I suspect that once the merger goes through the market will revalue TPGY stock (EVB stock then) about 67% higher.

On the date of publication, Mark R. Hake does not hold a long or short position in any of the stocks in this article.

Mark Hake writes about personal finance on mrhake.medium.com and runs the Total Yield Value Guide which you can review here.