When it comes to electric vehicles, investors shouldn’t look to me to provide an overly optimistic picture. While I recognize that EVs may very well be the future of transportation, it might not be an easy ride getting there. Certainly, many brands that look attractive today will fail. But for Lucid (NASDAQ:LCID), I don’t have the same reservation. If I had to electrify my portfolio, I’d go with LCID stock.

Why the confidence when I’ve been pensive on other related investments? It comes down to a simple fact that I’ve mentioned multiple times before: Lucid’s management team understands the reality of the EV market as opposed to the fantasy that so many outsiders are seemingly committed to believe in.

Put another way, before mainstream integration, EVs must be practically attainable to average households.

Unfortunately, that’s where the discussion ends for me. According to U.S. Census Bureau, the median household income was $68,703 in 2019. That amounts to $5,725 per month. For context, the cheapest Tesla (NASDAQ:TSLA) EV is the Model 3, which costs $40,000, or $667 per month for 60 months (principal only). No financial advisor would recommend a household to pay 12% of their gross income on a car payment.

Yes, cheaper EVs exist. But the problem is that a reasonably priced EV is hardly reasonable holistically. Typically, you’re talking about losing a wheel or sacrificing seating capacity. With Lucid, you’re not making any sacrifices, but that’s not the only reason to consider LCID stock.

Indeed, Lucid doesn’t make any pretenses about its target audience. With its cheapest models starting at $70,000, the upstart enterprise is going for the only demographic that can afford electrified transportation: the wealthy.

Better yet for LCID stock, the historical rate of integration of new technologies supports management’s cold but smart decision.

Long Stretches of Upside Awaits LCID Stock

In my last discussion about Lucid, I juxtaposed the historical rate of automobile production in the U.S. to the global production of EVs. If you look at the chart I produced comparing the two trends, you’ll have noticed that the rate at which Americans adopted the combustion automobile is very similar to the rate at which global citizens have adopted EVs.

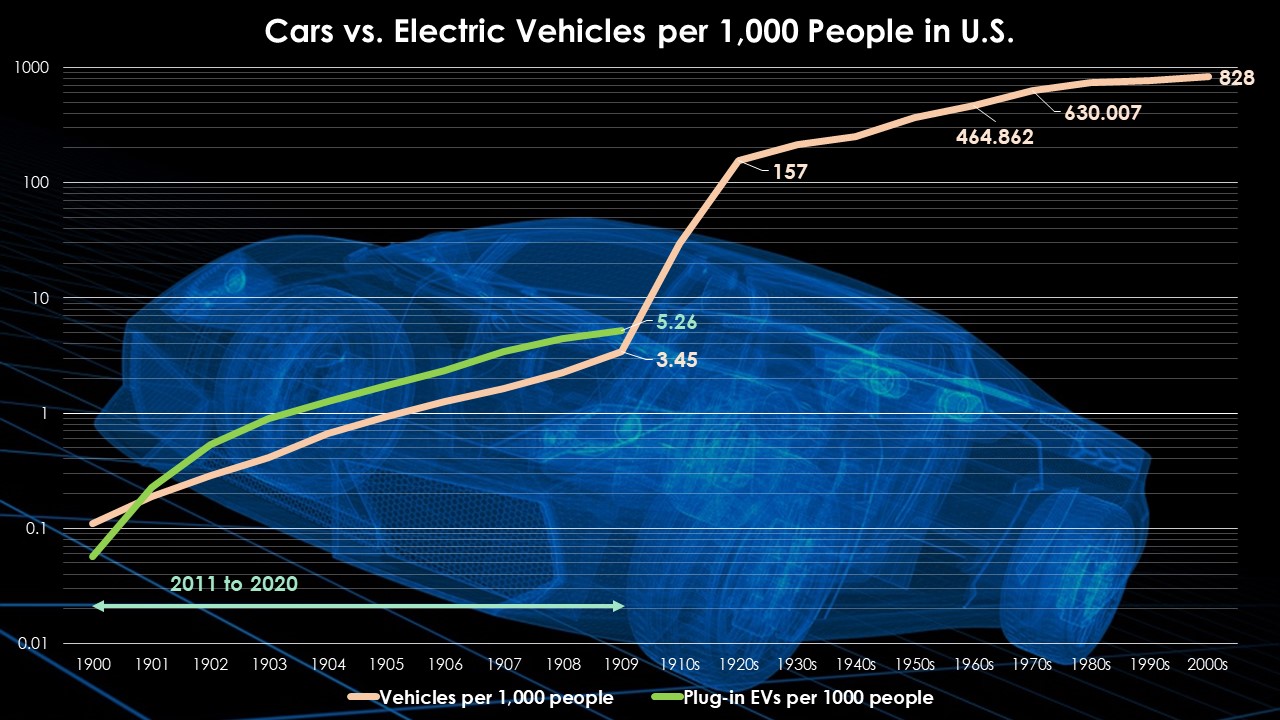

For this analysis of LCID stock, though, I’d like to compare automobiles and EVs per every 1,000 people in the U.S. alone. The reason why is that certain countries like Norway may skew global integration stats due to incredibly generous government subsidies.

Interestingly, the growth of automobiles per 1,000 people between 1900 through 1909 has a strong direct correlation with the growth of EVs per 1,000 people between 2011 through 2020; specifically, a correlation coefficient of 98%.

Click to Enlarge

At the end of 2020, there were only 5.26 EVs per 1,000 Americans. Similarly, at the end of 1909, automobiles numbered 3.45 per 1,000 Americans. Essentially, at the current juncture we’re in regarding EVs, only a very few can afford them.

Further, if we look at the historical integration rate of the automobile, it wasn’t until somewhere between the 1960s and 1970s — when the cars per 1,000 people metric broke above 500 — that the automobile became something that anybody with a reasonable income could afford.

And here’s where the situation is appealing for LCID stock. Compared to the advent of the combustion automobile, we’re basically back to 1910. Should historical rates of tech integration play out similarly, Lucid may have up to half-a-century of potential market dominance before rising battery technologies enable low-cost leaders to steal sizable share.

Even if Lucid only has 10 years of relatively smooth sailing in the luxury EV segment, that’s still a lucrative pathway.

A Solid-State Threat?

To be sure, not everything about LCID stock is encouraging. For one thing, the underlying company is an aspirational business. It must first prove it can produce, then it must stay relevant amid a ramp up of competition from legacy automakers.

But an intriguing headwind is the possible development of a solid-state battery. If SSBs become commercially viable, their energy density and enhanced capabilities across a smaller physical footprint could drastically reduce prices for EVs. That’s a positive for the environment but maybe not so much for Lucid.

Still, that innovation could be decades away, if it ever comes up at all. In the meantime, so long as tech integration trends stay consistent, I think you have a decent shot of long-term profitability with LCID stock.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.