Given that Nvidia (NASDAQ:NVDA) is a best-in-class growth stock, it’s a name that has to be on every growth investor’s watchlist. Why? In the same way that Nvidia is becoming a pillar in the tech space, NVDA stock should be a pillar in investors’ portfolios.

Now, not every investor is fit for growth stock investing. These names can endure swoons of 20%, 30% and even more than 40% at times. They also tend to command high valuations.

But here’s the secret that many investors either can’t accept or refuse to accept: a high valuation isn’t as scary as it seems.

The Truth About Valuation

I’ve been reading blogs, articles and dossiers for years. In many cases, someone will make the case that a stock is a good buy because of its low valuation or on the flip side, that a stock is a bad buy because the valuation is too high.

Now, valuations do matter — I’m not saying they don’t. But valuations don’t tell the whole story. For instance, think of it this way: Premium businesses trade at premium prices.

Why would a great company with solid growth and excellent financials trade at a low valuation?

That’s not to say a great company can’t trade with a low valuation. In the same light, a low-quality company can trade with a high valuation too. However, there’s a huge difference between a great company trading at a premium and a low-quality company trading at a discount. In both of these cases, it’s deserved.

For NVDA stock, we’re talking about an incredibly high-quality company. As a result, prepare to pay a premium (and be okay with it).

Why Nvidia Justifies a Premium Valuation

First, we’re talking about a company with secular growth drivers. There are not many companies out there carving out a significant role in multiple long-term growth segments. It has secular growth in gaming and graphics chips, Nvidia’s bread and butter. But it’s also present in the data center, AI and machine learning, autonomous driving and professional graphics.

In each of these categories, Nvidia isn’t just relevant, it’s dominant.

The company’s GPU offerings are the best in the business. Even though competition has picked up — how could it not? — we know Nvidia’s products are top notch because its margins are better.

While all of this is nice, justifying its premium valuation comes down to one thing: Accelerating growth.

Analysts expect 44.6% revenue growth this year to $15.8 billion. However, at the start of 2020, those estimates stood at just $10.8 billion. So we’ve seen Nvidia’s revenue estimates increase by $5 billion for this year. That is so much money it’s incredible.

Friends, realize that this isn’t a company that does $250 billion worth of sales each year, where $5 billion barely moves the needle. This is almost 50% higher than what was expected just 11 months ago.

Earnings are forecast to grow an even more impressive 57% to $9.11 per share this year. Next year, estimates cool to “just” 22% earnings growth (to $11.10 per share). However, I think these estimates may be conservative. The fact that we’re not seeing growth decline next year — suggesting 2020 wasn’t just a demand-driven event due to the novel coronavirus — is flooring.

Truth be told, I wouldn’t be completely surprised by $12.50 to $13 per share in earnings and $20 billion in revenue. Nvidia continues to show just how big its growth potential is and how much runway is left. For that, it is worth a premium.

The Bottom Line on NVDA Stock

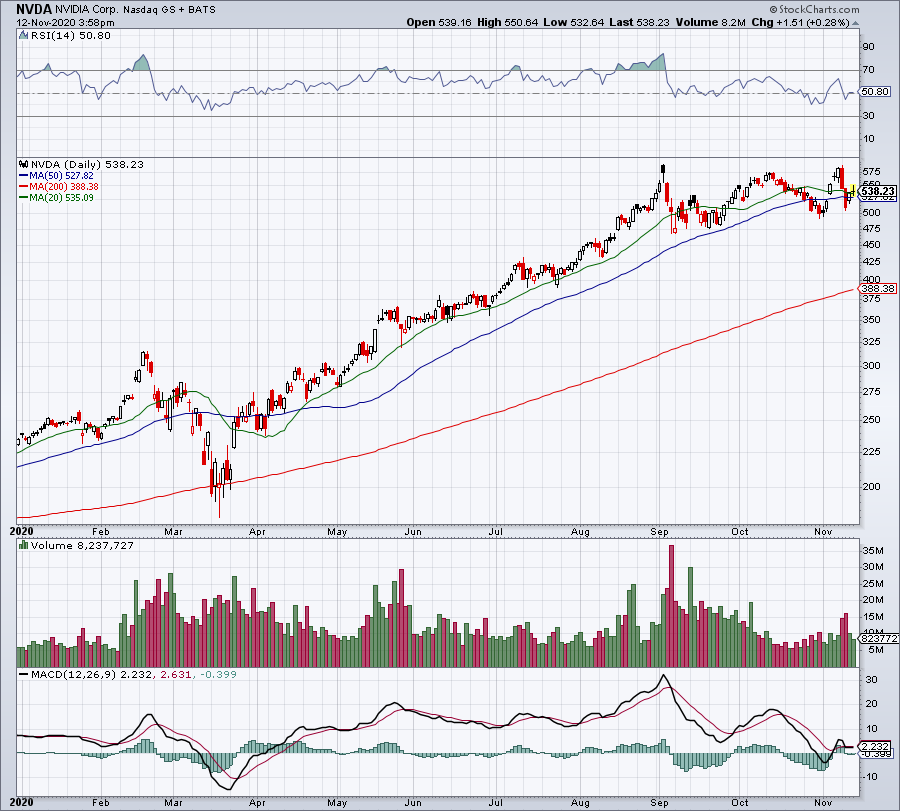

Click to Enlarge

Luckily for investors, NVDA stock has cooled off a bit. I don’t mean that sarcastically, either. When a stock is in a full-blown rally and the train is leaving the station, it can be hard to get on board.

However, when the stock takes time to digest its gains and/or pull back, that’s where the opportunity lies.

Too many investors look at the chart above and say, “No thanks. The stock is up huge — I’ll pass.”

That’s the wrong way to look at it, in my opinion. It’s not about where NVDA stock came from, it’s about where it’s going. I just highlighted how analysts had expected about $11 billion in sales this year. Now they expect almost $16 billion. Of course the stock has surged on that realization.

Realize too that, right as the market was topping, Nvidia stock was breaking out to new highs. Then growth accelerated even more. Then the company closed its deal for Mellanox. Now Nvidia is working to buy Arm, which would allow it to become a semiconductor juggernaut.

I like NVDA stock during this consolidation phase and even more so on a dip, should one develop.

On the date of publication, Matt McCall did not have (either directly or indirectly) any positions in the securities mentioned in this article.

The InvestorPlace Research Staff member primarily responsible for this article held a long position in NVDA.