A people however, who are possessed of the spirit of Commerce – who see, & who will pursue their advantages, may achieve almost anything.

This quote is likely one you haven’t heard before, but I bet you’ll recognize whom it came from: one of America’s Founding Fathers and the first president of the United States, George Washington.

George Washington wrote this comment on capitalism in 1784, but it holds just as true today. We’ve seen folks like Jeff Bezos go from “average Joe” to dominating the e-commerce industry with his company, Amazon.com, and becoming the richest man on the planet.

We also have billionaire Mark Zuckerberg, who founded Facebook and turned it into the No. 1 social media site in the world.

Or consider Bill Gates, founder of Microsoft, who carried $130 billion to his name as of November 2021. His company took the computer software industry by storm, and its market cap as of this writing is north of $2 trillion.

These men didn’t become billionaires overnight. They were talented, worked hard, saved and were smart to get ahead in life. They are the epitome of the American dream.

While I would be first to admit that I am no Bill Gates or Jeff Bezos (I’m also more of a car enthusiast than a rocket-ship fan), I do like to believe that my life story is also the embodiment of the American dream.

You may not know this, but I’m the son of a stone mason. I worked my way through college in hardscrabble neighborhoods near Berkeley, California. Given my background, I now have an abundant life.

I run a billion-dollar financial business. I’m a multimillionaire with beautiful homes in Nevada and Florida. My children attended the best schools. I’m able to collect the luxury cars I used to dream about as a kid.

Capitalism allowed me to build a wealthy life, but that character of America is changing. The government has decided that fiscal responsibility isn’t important anymore.

Let me explain…

Spenders Versus Savers

There are spenders and there are savers, and the U.S. government is most definitely a spender. In 2019, the United States ran its first $1 trillion budget deficit since 2012. In the two years since, the deficit has nearly tripled: In fiscal year 2021, the federal budget deficit was $2.8 trillion.

Those figures are just for the annual budget deficit, which is like the amount of money we make versus spend in a given year.

As for total debt?

At the end of 2021, our total national debt stood at a whopping $28 trillion. To put that into perspective, that’s essentially a credit card bill of nearly $84,850 for every American.

Today, the U.S. government owes more money to more people than anyone else in the world. In response to the COVID-19 economic shutdown, the U.S. government handed out trillions of dollars in direct payments to citizens and stimulus programs for businesses

The government also passed the Bipartisan Infrastructure Deal worth $1.2 trillion in spending. While the country badly needs infrastructure upgrades, passing the bill piles on to our deficit.

And now the government is proposing to spend even more money to cover a variety of social programs.

If passed, the “Build Back Better” spending bill would cost an estimated $2 trillion. It would reduce the costs of childcare and healthcare, fund national parks and forest preservation efforts, and make changes to Medicaid – all setting the United States up for an even greater deficit in the coming years.

To me, all of these programs signal that the United States is becoming less entrepreneurial… and more socialist.

All this spending – all this socialism – is setting the stage for massive devaluation of the U.S. dollar.

We’re Spending More Now Than We Did During World War II

To understand why the U.S. dollar is about to lose a lot of value over the next decade, you must understand our past.

I liken our current situation to a line of dominoes.

You know how it works…

One domino gets knocked over… which knocks over another domino… which knocks over another domino… and so on.

You get a chain reaction.

We are smack-dab in the middle of the most dangerous financial “chain reactions” in history… a reaction that could destroy the savings of millions of people.

The first domino that got us to where we are today is the buildup of debt leading up to the Great Financial Crisis of 2008.

You probably remember what those days felt like…

Back then, real estate values were soaring every year. It seemed like everybody was becoming a housing flipper or a developer. Big banks leveraged themselves 50-to-1 so they could play the real estate market. Entire countries took on huge debts to speculate in real estate. Until finally, the whole rotten structure couldn’t support another dollar of debt.

And then, that domino toppled over.

As that domino fell, portfolios of home loans collapsed. The stock market plummeted 50%. The real estate market crashed. Big banks went under. Lehman Brothers became the biggest bankruptcy in U.S. history. Millions of people lost their life savings.

Many people believed “The Greater Depression” was at hand.

And then, the crumbling financial system tapped the next domino…

The U.S. government stepped in and saved the banks. It spent nearly $1 trillion bailing out General Motors, Chrysler, insurance companies, and the mortgage market.

Many other governments around the globe followed suit. They launched one of the biggest bailout and stimulus packages the world has ever seen. Altogether, the amount of bailout and stimulus from national governments totaled over $3 trillion.

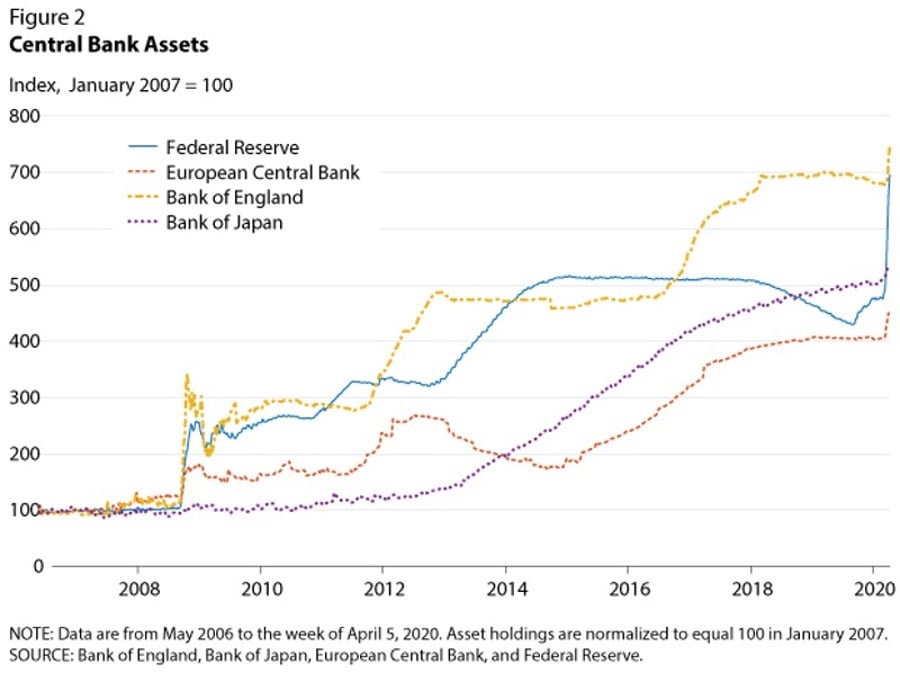

They printed much of it essentially out of thin air… and made it available via microscopic interest rates.

From 2008 to the end of 2019, the size of central bank assets soared from $6 trillion to more than $20 trillion. That’s a more than threefold increase in global central bank money creation.

This ocean of new money and credit didn’t create “regular” inflation as many people know it…

Instead, central banks pumped it into the financial markets – and inflated the value of the stock and real estate markets by trillions of dollars.

The government bailouts also inflated the value of “zombie” companies. These are companies that are too indebted and unprofitable to stand on their own. They need constant injections of debt and bailout money to survive. For example, in the beginning of the coronavirus pandemic, Congress gave the airlines a whopping $25 billion in federal funds to help the industry stay on its feet. Airlines were bleeding $180 million in cash a day, with passenger volumes slipping about 70% and the number of cancellations increasing.

In a 2019 report, Bank of America estimated that zombie companies made up an incredible 13% of all companies in developed economies. The inflated value of these zombie companies would have quickly gone to zero without all the “free money” from the government.

Again, that sounds more to me like socialism than the free-market capitalism that built our great nation.

But… we can’t deny that times felt good after the Great Financial Crisis was over.

The stock market soared more than 300% off its lows. Popular stocks like Google, Amazon, Netflix, Facebook, and Microsoft hit all-time highs. Real estate recovered and hit all-time highs in many areas. Unemployment hit a 50-year low.

However, the government’s money printing and ultralow interest-rate policy had dire consequences.

It made possible a historic pileup of more debt!

And it tapped the next domino…

As a result of the government’s money printing and ultralow interest rates, U.S. corporations have gorged on debt. They have built up over $11 trillion in debt. The amount of U.S. corporate debt to the country’s GDP hit an all-time record in 2021. A record amount of this corporate debt is rated “junk,” which means it is highly risky. Worldwide, companies have issued $13 trillion in debt.

That’s twice what they owed in the Financial Crisis year of 2008.

The government stuck its snout into the debt trough as well. Total U.S. government debt as a

Remember: Our government owes more money to more people than anyone else in the world.

And this all was happening before the COVID-19 crisis!

That’s what makes the huge amount of money printing we saw in 2020 and 2021 so dangerous. As we all well know, an economic shutdown is horrible for any economy. But it’s much, much worse for a highly indebted economy like America’s. The reality is it means the government bailout efforts must be huge in order to have any meaningful effect on the economy.

It means the government must print trillions of dollars, so the U.S. government’s $4 trillion in stimulus so far isn’t nearly big enough.

This “bigger than World War II” domino is about to crash into the U.S. dollar and every other currency on the planet.

They have been creating trillions of dollars out of thin air!

The result will be one of the largest mass paper currency devaluations in history…

When you take the $23 trillion of debt before we had COVID-19 and add the $6 trillion more in debt we accumulated during the worst of COVID and future government spending… you get a debt burden no nation can ever hope to possibly pay with sound money. Instead, we will pay it back with devalued, debased money created out of thin air. This rise of Socialist America will continue to create inflation, which, in turn, will cause the value of the U.S. dollar to plunge in value.

How the Coming Spending Spree Could Destroy Your Savings

Inflation is a term that gets thrown around a lot.

You’ve likely heard how Germany experienced massive inflation after World War I… and its paper money became worthless. Or, you might know how Venezuela recently experienced massive inflation… and its paper money became worthless.

But what exactly is inflation?

Inflation is the increase in the supply of money… which decreases the value of each “unit” of money. In America’s case, that unit is the dollar.

Let’s say a country has $100 million in its monetary system. People and businesses use these dollars to pay each other for goods and services. When people earn money, they park of some of those dollars in banks.

Now, let’s say the political leaders of this country decide to launch a big social welfare program and fight a war at the same time. The trouble is that the government doesn’t have the money to spend on those programs. It has already budgeted all of its tax revenue for other things.

For sake of simplicity, let’s say the government can’t borrow the money it needs for the welfare program and the war. Let’s also say that it’s politically unacceptable to raise taxes.

One option political leaders often choose – and they’ve done this for centuries – is to print new money to pay for the welfare program and the war.

They choose to “debase” their currency.

In this example, that’s what the government decides to do. The government prints up $20 million to pay for the social program. This increases the number of dollars in circulation by 20%. Remember, we started with $100 million and then added $20 million more, which is a 20% increase.

Because lots of new dollars make their way into the economy, people start noticing that prices are increasing…

The price of a $30,000 car works its way up to $36,000 (a 20% increase). The price of a $5 sandwich works its way up to $6 (a 20% increase).

Remember, neither the car nor the sandwich gets 20% bigger or better.

The value of the money simply fell… and caused the prices you see every day to increase. You are seeing that right now at the gas pumps and in the grocery stores. If you hold a lot of money in the bank during this inflation, you suffer a huge loss in purchasing power.

A big problem savers have with the U.S. dollar and other paper currencies is that they are controlled by political leaders who have huge incentives to spend more than they take in… which massively devalues the money over time.

Because of inflation, $100 in 1982 is worth about $282.90 today. But don’t think this is a problem from just the 1980s…

The amount of devaluation since just 2008 is shocking. Since 2008, the purchasing power of the U.S. dollar has fallen by about 20%. This is an incredible loss of your purchasing power. And this rise of Socialist America isn’t something that could just happen in the future.

It’s happening now.

So, what should you do about it to protect yourself?

Buy stocks.

Why Stocks Are the Ultimate “Devaluation Plays”

I want to take you back to 1980…

During that year, the Rubik’s Cube was released… Mount St. Helens erupted… The Empire Strikes Back hit movie theaters…

And the Dow Industrials Average sat at a mere 838.49. At the time, few people realized we were on the cusp of the greatest bull market in U.S. history. Starting at the 838.49 level in 1980, the Dow Industrials soared to 10,787 by 2000… a gain of 1,187%. Keep in mind, that’s just the “average” gain.

Top companies gained much, much more.

- Microsoft, for example, soared 50,000% during the 1980–2000 boom.

- Home Depot soared 20,000% during the boom.

- Amgen soared 40,000%.

- Cisco soared as much as 42,000%.

A modest investment of $5,000 in one of these super-boom winners could have grown into more than $2 million.

During the 1980–2000 super boom, innovations like computers, cell phones, and the internet changed the way we work and live… and our home prices soared.

However, few people realize the real, fundamental reason why the 20-year period from 1980 to 2000 saw stock prices soar at incredible rates to new highs.

That’s because few people know that the 1980s and ’90s were a period of significant inflation.

The average annual inflation rate during this “super boom” period was 4.2%.

Thanks to inflation, $1 in 1980 was worth just $0.44 by 2000.

It turns out, a 4.2% annual rate of inflation has proven throughout history to be a mild, stock market-boosting rate of inflation.

To be clear, when inflation runs at 4.2% for 10 years, any dollar you have in the bank loses 33% of its value.

A 4.2% annual rate of inflation is not good for people who keep all of their money in the bank or under a mattress.

However, we know that rate is extraordinary for stocks.

That rate acts as a stimulant to the economy. It greases the wheels of commerce and keeps things “buoyant.”

Remember, from 1980 to 2000, the Dow Industrials soared 1,187%… and top-performing companies gained much more.

Stocks are such a great inflation hedge because they represent ownership in real businesses. And great businesses act as inflation “pass through” vehicles. An inflation “pass through” vehicle is a business that “passes along” the price increases that occur as a result of inflation.

For example, if inflation sends the price of sugar and cocoa up by 5%, chocolate maker Hershey will “pass through” those input increases by raising the price of chocolate by 5%.

Or… if inflation sends the price of writing software code up by 7%, Microsoft will “pass through” those input costs by 7% by raising the price of its software.

Great businesses like Hershey and Microsoft act as inflation pass-through vehicles because people love their products and services (or at least can’t stand the idea of switching).

So… as inflation increases the price of input costs, these business can recoup those higher costs by charging more for their products. The nominal price of inputs and product prices might change, but the businesses’ profit margins do not. They simply “pass through” the inflation, which allows their profits and market values to rise along with prices. Of course, you can’t just throw a few darts at the S&P 500 to find the best stocks to defend yourself against the rise of Socialist America.

You need to find the best type of stocks… and then dig deeper to find the best individual stocks within that group.

It’s especially important to put your money into stocks now. The Federal Reserve is certain to raise interest rates in the future. The market has already priced in three to four rate hikes… so stocks won’t be taking a hit.

Simply put, stocks are your oasis in this inflationary environment… during the rise of Socialist America.

In the remainder of this report, I’m going to show you exactly which ones to own…

11 Stocks to Buy in Socialist America

For years, gold has been considered one of the best inflation “hedges” out there. And I believe gold will go up as inflation does.

But I believe tech stocks will do even better. In fact, tech stocks have proven a much better long-term inflation hedge than gold, as this chart of the Nasdaq 100 vs. gold since 1992 shows.

It’s no contest.

Tech stocks have returned over 3,700% since 1992… while gold returned 437%. That’s eight times better.

High-growth, high quality tech stocks CRUSH gold over the long term. I hope you see that rising technology stocks are the best way to grow your wealth in a Socialist America.

So which tech stocks should you buy right now for the maximum growth?

The key is to focus on the sectors just on the verge of a profit explosion. With inflation spiking, we don’t want to wait years before we see the big gains.

We want to invest in the technologies of the near future, just over the horizon.

The tech stocks I’m about to share with you aren’t the has-beens, the old news.

These are the tech giants of the next decade… before anyone’s ever heard of them.

I run the entire stock market through my Navellier Formula every week. And recently, nearly every week, the same names continue to pop up.

As I dug further, I realized these companies are the ultimate inflation-beaters… the ultimate hedges against Socialist America.

They have proprietary technologies in rising new industries… and they are poised to explode thanks to a flood of federal government tech spending expected to hit the market.

If you’re concerned about beating inflation, even as it rises every year, you need to own these stocks…

Top Stock to Buy No. 1: NVMI

Nova Ltd. (NVMI), formerly known as Nova Measuring Instruments, provides metrology solutions that are used in semiconductor manufacturing. The company offers a suite of products, including high-precision hardware and software, that are used by some of the biggest integrated-circuit manufacturers in the world. NVMI’s products allow manufacturers to dig deeper into the manufacturing process in order to shorten production times and increase product yields.

Back in June 2020, Nova said it expected demand for semiconductors to triple by 2025. The main drivers of this growth will come from artificial intelligence (AI), autonomous vehicles, smart cities, AR/VR, smart sensors and smart industry. Well, even amid the global semiconductor shortage of 2021, thanks to demand from these industries, we saw semiconductor demand increase immensely last year.

According to the Semiconductor Industry Association (SIA), global semiconductor sales rose 24% year-over-year to $48.8 billion in October 2021. SIA now anticipates that global sales will increase 25.6% in 2021 to $553 billion – and could exceed $600 billion in 2022. As such, Nova’s services and solutions should remain in top demand for the foreseeable future.

This strong demand has already added to and will continue to add to the company’s top and bottom lines. In fact, in the third quarter of fiscal year 2021, Nova achieved record results. The company reported earnings of $34.5 million, or $1.16 per share, on $112.7 million in revenue, which represented 104% year-over-year earnings growth and 62% year-over-year revenue growth. Analysts were expecting third-quarter earnings of $0.91 per share on $102.8 million in revenue, so Nova topped earnings estimates by 27.5% and sales forecasts by 9.6%.

Company management commented, “The increasing demand for our innovative portfolio along with the current market demand, paves us the way to another outperformance year in 2021 and builds a solid momentum towards 2022.”

For the fourth quarter of 2021, Nova expects revenue between $113 million and $123 million and earnings per share between $0.94 and $1.12. That compares to earnings of $0.55 per share and revenue of $76.3 million in the fourth quarter of 2020. Thanks to the strong outlook, analysts have upped fourth-quarter earnings estimates over the past two months. So, NVMI is likely gearing up for another quarterly earnings surprise.

Top Stock to Buy No. 2: FTNT

Fortinet, Inc. (FTNT) provides unified security solutions that can be deployed over digital networks to protect users against malware, spam and network intrusions. The company provides its security solutions to data centers, enterprises, carriers and distributed offices around the globe. Fortinet currently boasts a portfolio of 1,250 issued patents and 251 pending patents.

Since its founding back in November 2000, the company has had a meteoric rise. Over the past 21 years, it has shipped more security solutions than any other cybersecurity firm worldwide. It has sold more than 7 million units of its security solutions, and it has a base of more than 500,000 customers. And since 2002, its revenues have surged from just $2 million to $2.6 billion in 2020.

Clearly, the company’s products are in high demand. In fact, in the third quarter of 2021, Fortinet achieved total revenue of $867.2 million, or 33% year-over-year revenue growth, and earnings of $1.06 billion, or 42% year-over-year growth. Third-quarter earnings came in at $0.99 per share, topping estimates for $0.94 per share by 5.3%.

Fortinet also looks great going forward. For the fourth quarter of 2021, the consensus estimate calls for earnings of $1.15 per share on $957.58 million in revenue. That translates to 8.5% year-over-year earnings growth and 28% year-over-year revenue growth. The company has a strong earnings surprise history, so it will likely post even stronger fourth-quarter results.

Top Stock to Buy No. 3: EPAM

Grade-school friends Arkadiy Dobkin and Leo Lozner partnered back in 1993 to found software engineering services company EPAM Systems, Inc. (EPAM). Interestingly, the company had both humble beginnings and a global reach, as the company’s dual headquarters were in Dobkin’s apartment in New Jersey and in Lozner’s home in Minsk, Belarus.

Today, EPAM Systems operates in more than 35 countries, with more than 43,450 EPAMers and more than 275 Forbes Global 2000 customers. The company also has strategic partnerships with big-name corporations like Adobe, AWS, Google, Microsoft, Salesforce and SAP.

So, what services does EPAM offer to attract such noteworthy partners? Simply put, EPAM helps businesses adapt, grow more agile and faster, and stay competitive amid a constantly evolving digital world. The company offers consultants and data expertise, designers to customize and develop digital experiences, engineers to construct software platforms, next-generation software solutions and process optimization solutions.

EPAM Systems collaborates with clients in a variety of industries, including automotive, retail, business information services, financial services, life sciences, travel and hospitality, software and insurance. The company has also partnered with healthcare clients, including Curogram. EPAM is working with Curogram to help healthcare systems implement a simplified COVID-19 crisis-response solution.

For the third quarter of 2021, EPAM achieved earnings of $2.42 per share and revenue of $988.5 million, or 46.7% year-over-year earnings growth and 51.6% year-over-year revenue growth. The consensus estimate called for earnings of $2.22 per share on $964.61 million in revenue, so EPAM topped earnings estimates by 9% and revenue forecasts by 2.5%.

For fiscal year 2021, EPAM now expects revenue to increase 40% year-over-year and for earnings per share to come in between $8.72 and $8.79, up from $6.34 per share in 2020. And for the fourth quarter of 2021, EPAM anticipates revenue between $1.075 billion and $1.085 billion and earnings per share between $2.44 and $2.51, which is nicely higher than current estimates for earnings of $2.34 per share and revenue of $1.04 billion.

Top Stock to Buy No. 4: KLAC

Technology has evolved significantly over the years. For example, today’s smartphone has literally millions more RAM than the computer that put the Apollo 11 mission on the moon! The iPhone has 7 million more times RAM than the Apollo 11 computer.

The semiconductor equipment industry, which invents and produces electronic circuits from natural components, places a significant role in this technological evolution. So, it’s no surprise that this space is expected to see significant growth, too. Forecasts are for the market to increase from $66.1 billion this year to $103.5 billion by 2025 – a compound annual growth rate (CAGR) of 9.4% during that time period.

KLA Corporation (KLAC) is one of the biggest semiconductor equipment manufacturers in the world. With a focus on machine learning, electron and photon optics, and data analytics and sensors, the company develops solutions that enable next-generation technologies, including the cloud, robotics, internet of things (IoT), and autonomous vehicles.

In regard to chip manufacturing, KLA offers data analytics, defect inspection, in situ process management, metrology and patterning simulation. These solutions better enable microchip manufacturers to monitor the wafer and chip manufacturing process. The company also provides packaging manufacturing services, which help device manufacturers and foundries achieve higher yields and quality standards in advanced semiconductor packaging processes.

And that’s only a sample of all the solutions that KLA offers. The company also provides reticle manufacturing and quality control, stylus and optical profilers and nanomechanical testers, as well as offers support for the manufacturing of LED, photonics, MEMS, CPV solar and display.

KLA posted better-than-expected results for its second quarter in fiscal year 2022. The company achieved earnings of $5.59 per share and revenue of $2.35 billion, which was up from earnings of $3.24 per share and revenue of $1.65 billion in the second quarter of fiscal year 2021. Analysts were expecting earnings of $5.45 per share and revenue of $2.33 billion, so KLAC beat earnings estimates by 2.6% and posted a slight revenue surprise.

Looking forward to the third quarter of fiscal 2022, KLAC expects total revenue between $2.1 billion and $2.3 billion and earnings per share between $4.35 and $5.25. The forecast was slightly lower than the current consensus estimate, which calls for earnings of $5.50 per share and revenue of $2.37 billion.

Top Stock No. 5: CLFD

One corner of the market that has continued to expand, despite the global pandemic, is 5G.

As you probably know, 5G is the next generation of internet infrastructure and connectivity. With 5G, download speeds could be between 10 and 100 times faster than what’s currently available. All of the big wireless carriers, including Verizon, AT&T, Sprint and T-Mobile, are vying for the fastest network, and all released some form of 5G last year.

However, I’m not interested in the big wireless carriers. I see more opportunity in a company that’s designing and developing the fiber-optic platform to enable 5G connectivity.

Clearfield, Inc. (CLFD) started operations as APA Enterprises with the acquisition of fiber connectivity operations from Americable and Computer System Products in 2003. But, by 2007, the company changed gears (and names!) and reinvented itself as a leading provider of fiber-optic management, protection and delivery products.

The company’s “fiber to anywhere” platform was designed to not only meet the needs of broadband service providers, but also cut down on the costs associated with the deployment, management, protection and scalability of fiber-optic networks. Clearfield’s game-changing Clearview Cassette is the building block of its FieldSmart product portfolio of cabinets, enclosures, panels and wall boxes. All of which are designed with flexibility, service and network migration capabilities.

Recently, Clearfield introduced the StreetSmart Small Count Fiber Hand-Off Box, which was developed to streamline a provider’s ability to extend fiber networks even further into the network at a more economical price. The product is expected to support not only 5G network rollouts, but also the rollout of fiber-to-the-premise (FFTP) and wireless access services.

With 5G spreading across the country, from urban city centers to rural areas, it’s not surprising that Clearfield has seen strong demand for its products – or that it posted record results recently.

Clearfield achieved record results for its first quarter in fiscal year 2021. First-quarter revenue soared 89% year-over-year to $51 million, topping expectations for $41.27 million. First-quarter earnings surged 228% year-over-year to $10.4 million, or $0.75 per share, which compared to earnings of $3.2 million, or $0.23 per share, in the same quarter a year ago. Analysts were only expecting first-quarter earnings of $0.44 per share, so Clearfield crushed estimates by 70.5%.

Company management commented, “Clearfield delivered another record-setting financial performance in the fiscal first quarter of 2022, in a market that continues to evolve and grow with each passing quarter… We remain very optimistic about Clearfield’s growth potential as the demand for high-speed broadband, especially fiber-led broadband, continues to be very robust.”

Thanks to this strong demand coupled with the better-than-expected quarterly results, Clearfield increased its outlook for fiscal year 2022. The company now expects total sales between $176 million and $183 million, which would represent 25% to 30% year-over-year growth.

Top Stock No. 6: HIMX

Taiwan’s Himax Technologies, Inc. (HIMX) provides semiconductor solutions that are used in display imaging processing in consumer electronics. With more than 2,500 patents, Himax Technologies is a leader in display image processing semiconductor solutions. Its display driver integrated circuits (ICs) and timing controllers are used in laptops, tablets, mobile phones, car navigation systems, televisions, digital cameras and much more. And the company also develops controllers for touchscreens.

Third-quarter 2021 revenue jumped 75.4% year-over-year to $420.9 million, falling short of analysts’ estimates for $424.3 million. Third-quarter earnings were in line with analysts’ expectations for $0.80 per ADS, which represented a 1,043% year-over-year increase.

Looking forward to the fourth quarter, Himax Technologies expects revenue to rise between 4% and 8% quarter-over-quarter. Fourth-quarter earnings per ADS are forecast to be between $0.78 and $0.83, slightly lower than analysts’ current estimates for $0.89 per ADS.

Top Stock No. 7: SSTK

Founded back in 2003, Shutterstock, Inc. (SSTK) is a tech company that provides an online platform and marketplace for licensed images. Businesses of all sizes from around the world rely on Shutterstock to supply photos, videos, music clips, vectors and illustrations for their communication needs.

In fact, Shutterstock boasts that it has customers in more than 150 countries and its online platform is available in 21 different languages. A few big-name brands that rely on Shutterstock’s services include Google, BuzzFeed, CapitalOne, Aol., AMC and Marvel

More than 1 million contributors add to Shutterstock’s offerings. As a result, the company provides access to more than 1 billion forms of media content, including images, music clips and videos. Its image library contains more than 300 million images, with 200,000 images added each day.

Third-quarter 2021 revenue rose 18% year-over-year to $194.4 million, topping forecasts for $185.84 million. Adjusted third-quarter earnings dipped 13% year-over-year to $0.70 per share, but beat analysts’ estimates for $0.58 per share by 20.7%.

Shutterstock noted that it experienced a 32% increase in subscribers during the quarter, and it now has 336,000 subscribers. Subscriber revenue also rose 21% year-over-year to $81.5 million. The company’s image collection now contains about 390 million images.

Top Stock No. 8: INMD

More than 20 years ago, InMode Ltd. (INMD) was founded by a group of medical doctors and scientists who developed light, laser and radiofrequency devices for several minimally invasive surgical procedures, including body and face contouring, hair removal, liposuction, skin tightening, facial skin rejuvenation, wrinkle reduction, muscle stimulation and fat reduction.

The company’s third-quarter 2021 revenue soared 58% year-over-year to $94.2 million, with surgical technology platforms accounting for 73% of quarterly revenue. Analysts were expecting third-quarter revenue of $89.26 million.

Third-quarter earnings surged 77.4% year-over-year to $0.55 per share, up from $0.31 per share in the same quarter a year ago. Analysts were looking for earnings of $0.50 per share, so InMode posted a 10% earnings surprise.

Looking forward, InMode expects record full-year revenue between $356 million and $357 million, higher than the $343 million and $347 million range previously announced and earnings per share between $1.91 and $1.93. That’s up from earnings of $1.05 per share and revenue of $206.11 million in fiscal year 2021. This forecast is also nicely higher than analysts’ current expectations for full-year earnings of $1.86 per share and revenue of $341.03 million.

Top Stock No. 9: CAJ

Back in the early 1930s, Precision Optical Instruments Laboratory started out to research quality cameras in Tokyo. In 1934, the company developed the first 35-mm focal-plane-shutter camera in Japan, naming it the Kwanon. Within a year, the “Canon” trademark was registered – and the rest, as they say, is history!

Today, Canon, Inc. (CAJ) is synonymous with not only high-quality cameras but also office multifunction devices (MFDs), printers, copiers, scanners, camcorders, projectors, X-ray systems, ultrasound equipment, radiography systems, MRI systems, semiconductor lithography equipment, OLED display manufacturing equipment, flat panel display lithography equipment and more.

In 2020, office products accounted for 46% of total sales, while imaging systems (cameras) accounted for 23%. Canon achieved total 2020 sales of 3.16 trillion yen, or $30.39 billion.

For its fourth quarter in fiscal year 2021, sales increased 1% year-over-year to 955.4 billion yen, or $8.28 billion. Earnings of $0.50 per share beat analysts’ estimates of $0.49. Looking ahead, analysts estimate earnings of $0.46 per share on revenue of $8.03 billion.

Top Stock No. 10: DAVA

Endava Plc (DAVA) got its start in 2000 with a vision of revolutionizing the relationship between technology and people. Simply put, Endava is a technology services company that helps its clients better engage with their users or customers. The company partners with financial, insurance, media, retail and telecommunications companies around the world.

Endava offers several solutions across the digital evolution, agile transformation and automation areas. The company provides a Digital Strategy solutions, including the design, development and engineering and integration lifecycle for a business. To increase employee collaboration, Endava offers Agile Transformation practices and solutions to understand challenges, as well as define and develop processes. And to help businesses be more productive in taking product concepts to operation, Endava engineers develop and implement automation strategies, which includes infrastructure and software development.

First-quarter fiscal 2022 revenue jumped 55% year-over-year to 147.5 million pounds, up from 95.1 million pounds. Adjusted earnings surged 92.5% year-over-year to 28.3 million pounds, compared to 14.7 million pounds in the same quarter a quarter ago. Adjusted earnings per share came in at 0.49 pounds, topping analysts’ estimates for 0.43 pounds by 14%. The company now has 93 clients with more than 1 million pounds in revenue.

Looking forward to the second quarter in fiscal year 2022, Endava anticipates revenue between 150 million pounds and 152 million pounds, or 47% to 49% year-over-year revenue growth. For fiscal 2022, the company also expects revenue of 615 million pounds to 620 million pounds, which represents 40% to 41% annual revenue growth. Full-year earnings per share are forecast to be between 1.71 pounds and 1.76 pounds, compared to 1.30 pounds in 2021.

Top Stock No. 11: STX

Back in 1978, Seagate Technology plc (STX) got its start as Shugart Technology, but the company changed its name in 1979 and hasn’t looked back. In fact, for more than 40 years, Seagate Technology has been at the forefront of data storage solutions. The company introduced the first 5.25-inch hard disk drive (HDD) in 1980, and by 1982, Seagate had captured half of the market for small HDDs. By 1984, the company was the largest producer of 5.25-inch HDDs in the world.

Over the next two decades, Seagate went on to debut the Barracuda HDD, the first HDD with 7200-PM spindle speed, and the Cheetah 4LP, the first HDD with 10K-RPM spindle speed. In 2001, Microsoft selected Seagate’s HDDs for its Xbox game consoles. And in 2008, the company shipped its 1 billionth HDD.

So, it’s no wonder that Seagate Technology is the leading data storage solutions provider today, offering products that provide storage for and access to large amounts of data. In fact, along with its HDDs, the company also provides solid state drives (SSDs), solid state hybrid drives and storage subsystems. And its products are in high demand…

STX achieved its highest revenue in more than six years in the company’s second quarter in fiscal year 2022. The company noted that it received strong cloud data center demand, which helped deliver second-quarter revenue of $3.12 billion. That represented 19% year-over-year revenue growth and topped estimates for $3.11 billion.

Seagate also reported second-quarter earnings of $2.41 per share, which was up 87% from $1.29 per share in the second quarter of 2021. Analysts were expecting second-quarter earnings of $2.36 per share, so STX posted a 2.1% earnings surprise.

Looking forward to the third quarter, Seagate Technology expects revenue of about $2.9 billion and earnings per share of about $2. That compares to revenue of $2.73 billion and earnings of $1.48 per share in the third quarter of 2021.

Invest in Tech to Combat Socialism

We’ve gone over a lot in this report – everything from the history of inflation to what’s happening now in the White House. And most importantly: The future of the U.S. economy in a time when socialism seems to have taken the reins.

As we’ve discussed, there are several strategies you can take to invest in the current economic and political environment. The reality, however, is that investing in the tech giants of the near future will be the best way to grow your wealth as America throws capitalist values to the wayside.

To beat the ever-growing inflation, you need to own stocks with superior fundamentals and the potential to profit big – and those types of stocks are exactly what I’ve picked out for you today… the crème-de-la-crème.

Like I mentioned before, I’ve picked these stocks based on the findings of my proprietary market-beating system. Therefore, I know that these are your absolute best bets against inflation and Socialist America.

Now… watch your inbox for my regular Market360, which I send your way several times a week. In there, you’ll get all my updates on big earnings, my latest stock picks and much more.