Russian supply is getting kneecapped … but Chinese demand is equally in the toilet … where do prices go next? … watching the EU

Oil prices have taken a slight breather in recent weeks. But if you think that means the oil trade is done, think again.

To establish some context, let’s look at a chart of the U.S. oil standard, West Texas Intermediate Crude (WTIC). As you can see below, it’s soared here in 2022 in the wake of the Russian invasion of Ukraine.

But since March, the price of WTIC has been saw-toothing.

So where will oil prices go next?

Well, we’re about to witness a massive battle between supply and demand.

Specifically, both forces are running into headwinds, but at present, it’s unclear whether supply will have it worse, leading to higher prices, or if demand will have it worse, which will lower prices.

Either way, there’s still money in the oil trade. We’ll explain that momentarily. But first, let’s look at supply.

***The domino effect of Russian oil sanctions

Russia has the world’s largest natural gas reserves. It’s also the third-biggest oil producer, making up about 12% of global oil production.

Obviously, sanctions on Russian oil – both official, by global governments, and unofficial, by corporations not wanting public relations blowback – are decreasing the amount of oil in the market.

But let’s dive into what this really means.

From Oil Price:

The war Putin started in Ukraine is hitting home: storage capacity is full, infrastructure and shipping logistics prevent Russian from exporting all the oil unwanted in the West to China and India, refineries are cutting run rates as product storage is overflowing, and as a result, companies are scaling back crude production…

In the first ten days of April, Russia’s crude oil and condensate production slumped to an average of 10.365 million bpd, data obtained by Energy Intelligence showed this week. That’s more than 600,000 bpd below the March average crude and condensate output of 10.996 million bpd.

According to the IEA, Russian oil supply and exports continue to fall, with April losses expected to average 1.5 million bpd as Russian refiners extend run cuts, more buyers shun barrels, and Russian storage fills up.

From May onwards, nearly 3 million bpd of Russian production could be offline due to international sanctions and self-sanctioning from buyers.

On the current trajectory, we’re going to see vast cutbacks in Russian production. For example, Vagit Alekperov, the president of Russia’s second-largest oil producer Lukoil, informed Russia’s Deputy Prime Minister that storage is already brimming with fuel due to the plunge in oil deliveries.

So, with fewer buyers and no more places to store oil, what’s going to happen?

You have to shut off production.

From The Wall Street Journal:

In the latest indication of problems ahead, the International Energy Agency forecast Wednesday that starting in May, almost 3 million barrels a day in Russian production will be turned off.

That would reduce output to fewer than 9 million barrels a day, a larger pullback than other analysts have predicted…

A sustained drop would undermine the prime driver of Russian growth just as sanctions are set to pitch the economy into a steep recession.

“There is the risk you permanently lose some production potential,” said Helge André Martinsen, senior oil analyst at DNB Markets.

While this is a political victory, it’s a disaster for consumers because the world can’t make up the supply differential. Especially if there are “permanent” production losses, as Martinsen just noted.

OPEC’s Secretary General Mohammad Barkindo recently said “OPEC+ could not replace a complete loss of Russian oil to the market.”

***This comes as no surprise for readers of our macro expert, Eric Fry

In his newsletter Investment Report, Eric evaluates markets and asset classes from a big-picture perspective to identify attractive opportunities. When he’s found such an opportunity, he digs down to find the best ways to play it. Given this approach, Eric has been all over the opportunities in oil for months now.

Returning to the supply imbalance due to Russian sanctions, here’s Eric from his latest issue:

Many folks assume that OPEC producers could easily boost output to satisfy any significant surge in demand. But could they?

So far, the evidence is not persuasive.

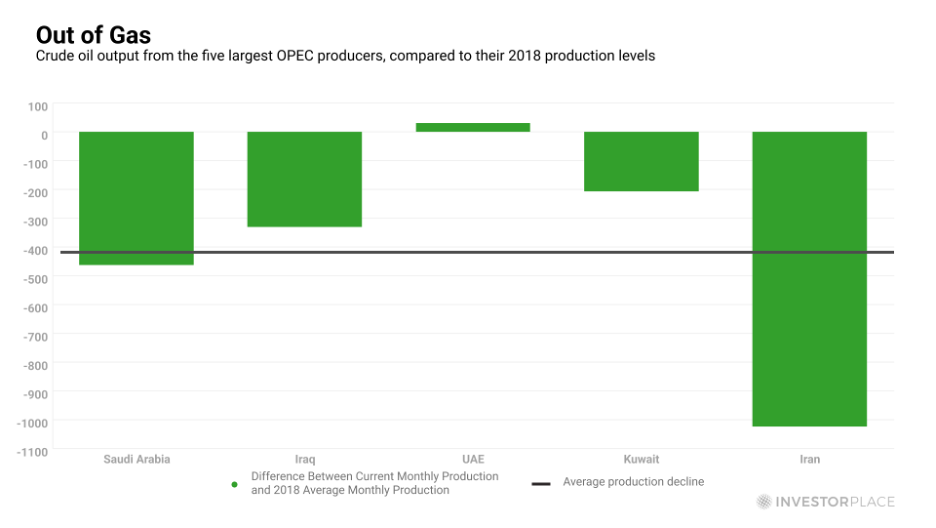

Production has been declining in many OPEC countries for years, and the cartel’s total output has tumbled by nearly five million BPD from its 2018 peak.

The U.S. has supplied almost all of the world’s crude production growth during the last decade, not OPEC. Performing that dazzling stunt a second time will not be easy, as U.S. shale production topped out two years ago.

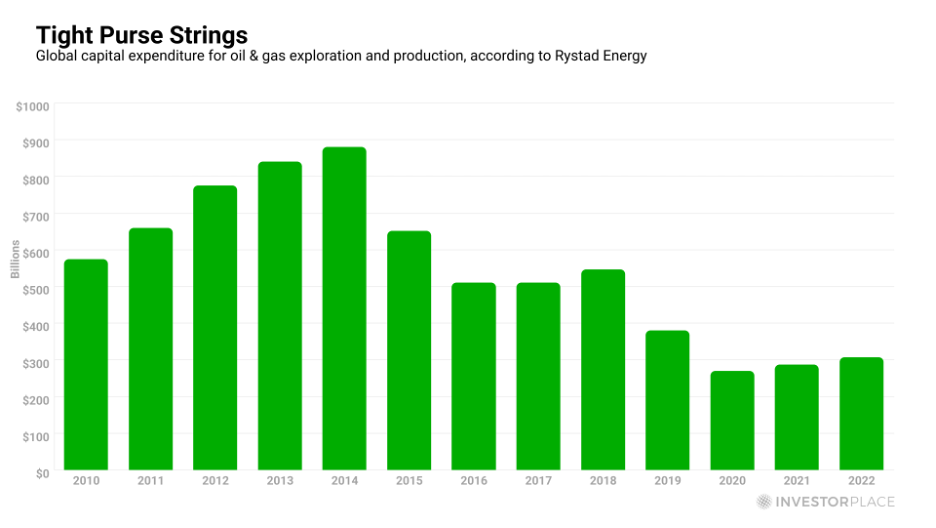

Furthermore, as I have pointed out previously, oil and gas companies have been slashing their exploration budgets for many years… Global investments in oil and gas exploration and production have plummeted by about 65% since 2014.

Net-net: Bountiful new supplies of crude oil seem highly unlikely.

Now, let’s include a new, major wrinkle – there’s the potential Europe is going to ban Russian oil.

From The New York Times:

European officials are drafting plans for an embargo on Russian oil products, the most contested measure yet to punish Russia for its invasion of Ukraine and a move long resisted because of its big costs for Germany and its potential to disrupt politics around the region and increase energy prices.

Having earlier this month banned Russian coal for the first time — with a four-month transition period to wind down ongoing orders — the European Union is now likely to adopt a similarly phased ban of Russian oil, E.U. officials and diplomats said. The approach is designed to give Germany, in particular, time to arrange alternative suppliers.

This would be a gamechanger.

Russia supplies over 4 million barrels of oil per day to Europe. Even a partial ban on these imports would lead to far wider Russian production shutdowns, and a major uptick in prices.

Here’s the bottom line from the Dallas Fed:

…Unless the Russian petroleum supply shortfall can be contained, it appears necessary for the price of oil to increase substantially and to remain elevated for a long period to eliminate the excess demand for oil.

By the way, we haven’t even mentioned news from yesterday that Libya is shutting down its oil fields.

From Bloomberg

:

Libya’s oil production has fallen by more than half a million barrels a day as a wave of political demonstrations engulfs the OPEC member’s energy industry.

The Sharara field in the west of the country, which can pump 300,000 barrels each day, was closed after protesters gathered at the site demanding Prime Minister Abdul Hamid Dbeibah quits, according to people familiar with the matter. That came after the nearby El Feel deposit, with a daily capacity of 65,000 barrels, was halted for the same reason.

Not good.

So, clearly supply is facing massive problems.

But let’s switch gears, because so too is demand.

***Could China-based demand reduction offset Russian supply reduction?

As we’ve been profiling here in the Digest, China is a pursing a “zero COVID” approach.

This has resulted is lockdowns on a colossal scale.

From CNBC:

China’s latest wave of Covid restrictions has forced millions of people — roughly three times as many as live in New York City — to stay home and undergo mass virus testing in the metropolis of Shanghai.

As Covid cases began to spike in late February, Shanghai tried to control the outbreak with targeted, neighborhood lockdowns.

But the city, a center for global transport, manufacturing, finance and trade, decided in late March to implement a two-stage lockdown that soon applied to all districts, generally forcing people not to leave their apartments.

For some perspective, Shanghai has nearly the same number of people as all of Australia. Its GDP is bigger than that of Sweden’s. And it’s home to the world’s busiest port, accounting for 7.3% of all of China’s exports.

Plus, Shanghai isn’t the only Chinese city dealing with lockdowns. For example, the city of Xi’an just said it would impose a partial lockdown on its 13 million residents.

This stands to have such a dramatic impact on oil demand that the International Energy Agency (IEA) just dialed back its estimates of global demand.

From Bloomberg:

(The IEA) lowered projections for world fuel consumption this year by 260,000 barrels a day, with a particularly steep reduction of 925,000 a day for China in April.

But let’s be clear about this: The IEA isn’t suggesting lower oil demand compared to 2021 – just a lower increase compared to its prior forecasts.

Last week, Toril Bosoni, head of the IEA’s oil-industry and markets division, said “the market does look more balanced.”

Now, Bosoni is saying this as WTIC trades between $100 and $110 a barrel. So, what would a market that’s “balanced” at these prices mean for the oil trade?

Back to Eric:

If, as I believe, the new energy bull market is still in its infancy, and if $100+ oil becomes the new normal, oil companies will begin minting money. Big time.

At the same time, investors will become increasingly convinced that the industry’s robust profit growth can continue to grow for a good, long while.

These positive influences could power most energy stocks to much higher highs over the months ahead.

Even if we’ve reached a relative supply/demand balance today, the current, elevated price of WTIC will drive big returns for top-tier oil plays.

And keep in mind, if the European Union does, in fact, ban any portion of Russian oil imports, watch out: Oil will surge.

We’re running long, so we’ll wrap up. But if you want more of Eric’s research on oil and his specific trades as an Investment Report subscriber, click here.

I’ll give him the final word:

Bottom line: The powerful new bull market in oil & gas stocks will likely deliver a few more upside “surprises” over the coming months.

Have a good evening,

Jeff Remsburg