Angry Americans and paycheck to paycheck living … the Fed is a lot of big talk, little action … looking beyond more market pain to what comes after

Before we dive in, let’s take a moment to enjoy today’s rally.

It’s long overdue and shows how quickly markets can rise when pessimism grows too extreme.

But now, let’s look bigger picture.

One great day in the market does not make a trend. So, let’s try to analyze the massive tectonic movements that will be the building blocks of those long-legs trends – we’re talking quarters and years, not days.

Now, on one hand, things are pretty good…

Just about everyone who wants a job has a job (as evidenced by the millions of open positions that employers are having trouble filling).

Meanwhile, earnings are still largely strong. The earnings analytics company FactSet will update their data later today, but based on last’s Friday’s information, 87% of the S&P has reported earnings and 79% of those companies have reported positive earnings surprises.

And, of course, home prices have enjoyed huge run-ups. So, the balance sheet of the average American has been padded over the past couple years.

Despite this, Americans aren’t feeling optimistic.

As you can see below, consumer sentiment has fallen to levels nearly on par with those found at the depth of 2009’s great financial crisis.

What’s behind this?

From The New York Times yesterday:

Americans are unhappy about the economy.

They report less confidence in it than they did at the start of the Covid pandemic, when the unemployment rate was four times as high as it is now…

The culprit is what Americans describe as one of the most important problems today: high inflation.

Inflation stands out from other problems because it is so inescapable.

Unlike unemployment, it affects everyone. And people encounter it every day — when they go to the grocery store, drive by a gas station or buy almost anything.

***Inflation has moved beyond being an “annoyance” and is now having a marked impact on Americans’ daily living

Last week, LendingClub released its 9th edition of “New Reality Check: Paycheck-to-Paycheck Report.”

From Anuj Nayar, Financial Health Officer at LendingClub:

The number of people living paycheck to paycheck today is reminiscent of the early days of the pandemic and it has become the dominant lifestyle across income brackets.

As inflation we have not seen in a generation takes more of our paychecks for everyday needs, Americans across incomes and credit scores are increasingly relying on credit products just to get by.

The report finds that close to two-thirds of the U.S. population, 64%, were living paycheck to paycheck in March.

With the number that high, it’s clear this dynamic isn’t limited to lower-income Americans. In fact, the report shows that of consumers earning more than $100,000, a whopping 49% of them are living paycheck to paycheck.

This is resulting in a change in consumer behavior.

For example, last month, the Food Industry Association published research finding:

The majority (86%) of shoppers who are worried about rising food prices are making behavior changes, including looking for deals (59%), making substitutions or product changes (58%), changing where or how they buy groceries (48%) or buying more store brands (35%).

***The challenge with this is that we’re at risk of inflationary psychology becoming entrenched

In an interview that Fed Chairman Jerome Powell just did with American Public Radio’s Marketplace, he said: “But ultimately the most painful thing would be if we were to fail to deal with it and inflation were to get entrenched in the economy at high levels…”

What if it’s already more entrenched than Powell realizes?

At the beginning of today’s Digest, we included a consumer sentiment chart. That comes from the University of Michigan.

Richard Curtin is the University of Michigan professor who has directed these surveys since 1976.

He recently wrote an opinion piece for Barron’s, highlighting the danger he’s seeing today:

Prices and wages will continue to spiral upward until the cumulative erosion in inflation-adjusted incomes causes the economy to collapse in recession.

It is like the children’s game of musical chairs: Everyone knows the game will end, but they feel compelled to keep racing around the circle at an ever-faster pace, hoping their forced exit will leave them in the best possible position—even if it still means an inflation-adjusted loss.

This situation has been termed “inflationary psychology.”

Consumers purposely advance their purchases in order to beat anticipated future price increases. Firms readily pass along higher costs to consumers, including the future cost increases that they anticipate.

That’s what happened in the last inflationary age, which started in 1965 and ended in 1982: Expected inflation became a self-fulfilling prophecy.

But let’s push back.

On Wednesday, we saw a decrease in the CPI number. Yes, it was smaller than anticipated, but it was a decrease nonetheless. And yesterday, we saw a similar small decline in the Producer Price Index.

Should we not be encouraged by this and interpret it as a foreshadowing of additional decreases to come?

Back to Curtin:

Another critical characteristic of the earlier inflation era was frequent temporary reversals in inflation, only to be followed by new peaks.

That same pattern should be expected in the months ahead.

***Curtin suggests that the Fed remains more focused on the labor market than inflation, despite big talk

In recent weeks, we’ve been barraged with speeches from Fed members that are filled with tough talk on inflation.

“Inflation is much too high” … “acutely concerned” … “is as harmful as not having a job.”

Last month, it was Fed Governor Christopher Waller who put on the tough guy act:

We know what happened for the Fed not taking the job seriously on inflation in the 1970s, and we ain’t gonna let that happen.

This week, Powell said the same thing without quite as much Dirty Harry:

Now, we see the picture clearly and we’re determined to use our tools to get us back to price stability.

But there’s a huge difference between big talk and big actions. Back to Curtin (underline added):

Most consumers expect the government to undertake policy actions to curb inflation.

Indeed, the largest proportion of consumers in the past half-century have expected the Fed to hike interest rates.

Given that the fed funds rate had lingered for an extended period near zero, that was not a hard call to make.

What was perhaps more surprising was that the quarter-point hike the Fed adopted in March was simply too small to signal an aggressive defense against rising inflation.

Instead, it signaled the continuation of a strong labor market along with an inflation rate that would continue to rise.

The Fed had another chance to make good on tough talk at its last meeting, too, by raising rates 75 basis points. As you know, it opted for only a 50-basis-point hike.

***It feels like the Fed is playing the role of the playground bully who’s actually a coward

He doesn’t truly want to fight because he’ll get whipped, so he spouts lots of big-talk bluster, trying to scare his opponent into inaction.

We showed the chart below in our Monday Digest. It compares the Fed’s response in rate hikes to the CPI.

If you’re having trouble seeing the size of the Fed’s rate hike (in blue) relative to the huge spike of inflation (in red), that’s pretty much the point.

The Fed is not acting like a central bank that’s serious about ruthlessly eradicating inflation.

Unfortunately, history suggests that a soft approach doesn’t work.

Back to Curtin:

Many commentaries assert that the current situation is nothing like the situation faced in 1978-80. That’s true, but irrelevant.

The more apt comparison would be to the five to ten years prior to that period, when inflation had not yet reached crisis levels.

Government officials claimed they had the policy tools that could easily reverse inflation, just as they claim now.

Those policies, however, repeatedly failed across administrations, from Lyndon B. Johnson’s surtax, to Richard Nixon’s wage and price controls, to Gerald Ford’s public relations “Whip Inflation Now” campaign, and Jimmy Carter’s fireside pleas to diminish material aspirations.

Only after Paul Volcker was appointed Federal Reserve chair and raised the fed funds rate to 20% in 1980 did inflation begin to fall.

He pushed up rates aggressively, by 10 percentage points in just six months. The resulting 10% unemployment rate was needed to reduce inflation by 10 percentage points.

We keep hearing about the “soft landing.” But keep in mind, so much of the potential for a soft landing is based on things the Fed doesn’t control – namely, the supply side of the equation. We’ve pointed this out several times in the Digest this week.

What this means is that even if the Fed executes perfect policy, we could still be in for a crash landing due to things outside its control.

Powell actually made this very same point yesterday. From Seeking Alpha:

“Inflation is just way too high here in the United States,” Powell later said in an interview on American Public Radio’s Marketplace program.

The central bank’s tools for taming that inflation are only focused on demand, and “supply is a big part of the story here.” There are additional factors such as the war in Ukraine and new lockdowns in China to limit the spread of COVID-19, so there is no guarantee “whether we can execute a soft landing or not… it may actually depend on factors that we don’t control.”

***If Curtin is correct in all of this, it means we still have plenty of economic and market pain in front of us

Yes, that will be tough for Main Street and Wall Street alike.

But it will also present investors with a generational buying opportunity when the dust settles.

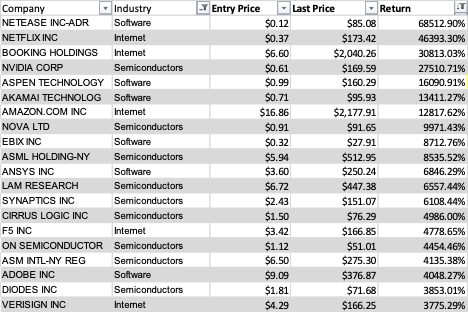

Earlier this week, our CEO Brian Hunt sent around a spreadsheet showing the gains from certain technology stocks as measured from their lows of the great financial crisis through their peak price in subsequent years.

Here’s a screenshot of some of the top-returning stocks:

These are life-changing returns – and that’s not hyperbole or embellishment. A 68,000% return turns a $10,000 investment into nearly $7 million.

Now, when you combine an inflationary-induced bear market with the type of tech-fueled economic growth we’re going to see as this decade rolls on, we should expect similar returns for the market’s top performers – if not even greater.

So, there’s plenty of reason for excitement today despite the gloom.

But if Curtin is right, there’s more pain to come before we have that opportunity. Be ready for that – most people won’t be.

Back to Curtin:

Much more aggressive policy moves against inflation may arouse some controversy. Nonetheless, they are needed.

Adam Smith’s legendary invisible hand describes how individuals acting in their own self-interest can create unintended benefits for the entire society.

Unfortunately, the country now faces the potential for an inflationary hand that can transform self-interested decisions into losses for the entire economy.

Perhaps, but those losses will create the opportunity for a complete transformation of your portfolio over the next decade.

Let’s enjoy today’s gains. But keep your focus on the big picture. It’s likely there’s additional weakness in front of us, but what comes after that will be explosive.

Have a good evening,

Jeff Remsburg