Listen to the audio version of this article (generated by AI).

The jobs report Main Street wanted, Wall Street didn’t… the consumer underneath the headline… AI displacement gets new data… a week that could move everything

As I write on Monday morning, the markets are trying to claw back from last Friday’s tech rout triggered by the blowout jobs report – it was the last thing an inflation-rattled market wanted to see.

The May employment report landed well above expectations. The U.S. added a seasonally adjusted 172,000 jobs in May, more than doubling expectations of 80,000. Meanwhile, the unemployment rate held steady at 4.3%.

Stepping back, payroll gains have averaged 188,000 over the past three months – a pace not seen since March 2024.

Now, this would appear to be great news – so, why the Friday tech-wreck?

Because the report landed on top of the latest Personal Consumption Expenditures (PCE) inflation reading of 3.8% – the highest since May 2023 – and two consecutive inflation prints trending in the wrong direction. A robust labor market, in this environment, doesn’t give the Fed any room to cut interest rates. If anything, the conversation now shifts to rate hikes.

White House National Economic Council Director Kevin Hassett told Bloomberg Television that investors are “terribly wrong” to interpret the strong report as evidence that the Fed will hike rates – his argument: oil-price shocks historically produce temporary, not lasting, inflation.

We’ll find out soon enough. Fed officials meet next week under the leadership of new Chairman Kevin Warsh – and Friday morning’s data just made that meeting considerably more interesting.

But Fed policy aside, is this report really a glowing reflection of Main Street health?

Let’s break it down.

The headline vs. what’s underneath

Friday’s jobs number looks strong on the surface. Underneath, there’s a different picture.

Beyond the 172,000 new jobs, the same report showed that year-over-year average hourly earnings rose just 3.4% in May – down from 3.6% in April. With PCE inflation running at 3.8%, that means real wages are deeply negative. Translation: workers are getting raises that don’t keep up with what they’re paying at the pump and the grocery store.

Meanwhile, the long-term unemployment rate – people out of work for 27 weeks or longer – jumped to 27.5% in May. That’s up from 25.3% in April, and the highest level since December 2021.

So, under the glossy “172,000 jobs” headline, there are widening cracks.

And it gets more complicated…

Even as long-term unemployment ticks up and real wages decline, our technology expert Luke Lango, editor of Innovation Investor, has been tracking a strange paradox.

Here’s Luke:

Nominal personal spending growth rose in April from 5.7% to 5.9% — the strongest reading since January 2025.

Consumers haven’t pulled back at all. If anything, they’re spending more. But the fundamental support for that spending has completely collapsed underneath them.

So, if wages aren’t funding this spending binge, what is?

Savings.

Luke reports that the U.S. personal savings rate crashed to 2.6% in April 2026 – one of its lowest levels in modern history.

But savings aren’t the only source of this spending – it’s also coming from debt. And some cracks are forming.

Here’s CBS News:

Credit card delinquencies across the U.S. have reached their highest level since 2011…

Nationwide, about 13% of all credit card accounts were in arrears in the first quarter.

CBS went on to report on data from Fidelity that more Americans are taking out loans and making hardship withdrawals from their 401(k)s.

So, while Friday’s headline unemployment rate suggests the labor market is strengthening, the picture for the American consumer is considerably more troubling.

Here’s the Wall Street Journal‘s summary from Friday:

American consumers report feeling miserable about the economy, gasoline prices, inflation and the labor market.

A key measure of consumer sentiment has hit new all-time lows in recent months amid anxiety about future inflation.

Where does all this take us?

Here’s Luke’s latest prediction:

Over the next 12 months, the consumer situation goes from bad to worse.

Sometime in 2027, they hit the wall. Spending collapses. Consumer confidence craters.

And since consumer spending still drives roughly 70% of U.S. GDP, the broader economy starts to crack.

And here’s where the AI jobs-displacement narrative that we’ve been tracking kicks in.

Luke predicts that when the economy starts to crack, corporate revenues will be hit. So, how will management respond?

By accelerating the transition from human workers to AI.

That dynamic feeds directly into Luke’s “2028 election” forecast – a populist, bipartisan anti-AI movement pushes through legislation. That could look like different things – perhaps a tax on AI profits, a forced limit on hyperscaler capex, or maybe mandatory review processes for new AI models – but whatever the form, it derails the AI trade.

Back to Luke:

By late 2028 or early 2029, those politicians follow through…

That’s the March 2000 moment for the AI bull market.

We’ll keep tracking this.

And on that note, last Thursday, the data gave us something new to track…

The AI jobs debate just got more data

Over the last several months, I’ve been in what I’d call a “convince me” posture about AI-driven job displacement.

Long-time Digest readers know I’ve spent years flagging the risk. But over the last 12 months, I’ve encountered increasing data and analysis that counter that narrative. At a minimum, on its timing.

Most recently, I came across research from Citadel Securities reporting that job postings in AI-exposed sectors are now rising, not falling. Meanwhile, executives are framing AI as a complement to their workforce, not a substitute for it.

Today, while still concerned about the job displacement thesis, I’m holding it with less conviction than before as I track the data, which brings us to last Thursday’s Challenger, Gray & Christmas report.

The headline:

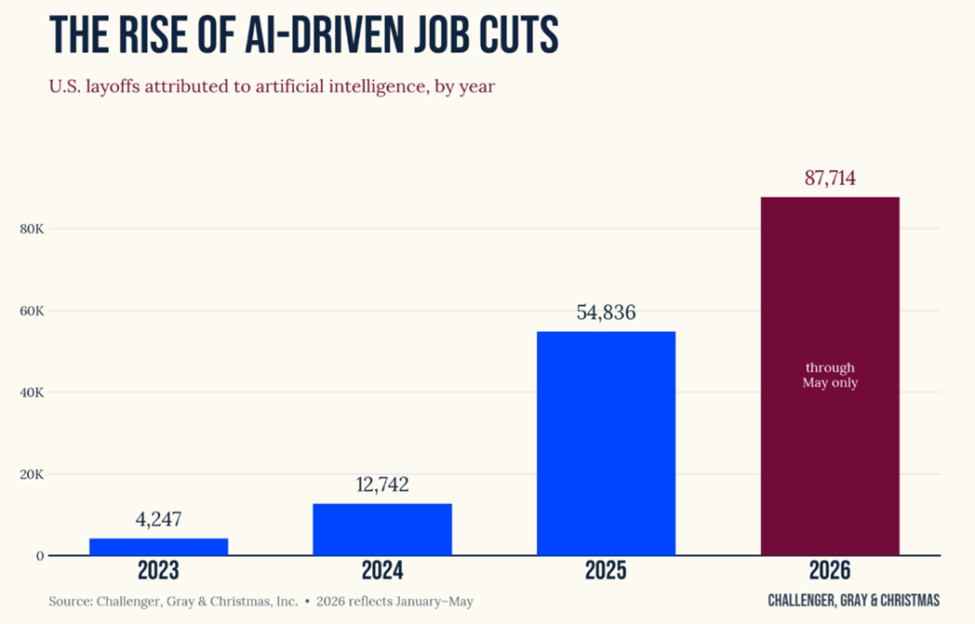

AI drives May cuts to 97,006, the highest May total since 2020.

For the third straight month, firms cited artificial intelligence as the leading reason for layoffs – accounting for 40% of all May cuts.

AI-driven job cuts have now reached 87,714 so far this year, already up roughly 60% versus all of 2025, with seven months still to go.

Luke saw the report and offered a pointed response:

Jevons’ Paradox… meet Engels’ Pause.

To make sure we’re all on the same page, Jevons’ Paradox holds that when a resource becomes more efficient, total consumption of that resource tends to rise rather than fall.

Applied to AI: cheaper, more capable AI might expand demand for workers who use it, not shrink it.

Meanwhile, Engels’ Pause refers to a period during Britain’s Industrial Revolution – roughly 1790 to 1840 – when GDP growth exploded, and corporate profits surged, while average workers’ real wages remained flat or fell for 50 years.

The wealth eventually trickled down. The jobs eventually multiplied. But it took half a century.

Luke argues that AI is compressing that same dynamic into a single decade. The steam engine took a century to deploy. ChatGPT hit 100 million users in two months.

So, while the Jevons argument has its believers, Luke isn’t one of them – at least not right now:

While I understand those arguments in the long-term, I’m not sure I believe them in the short-term, because the numbers and announcements tell a pretty clear story.

That story added a new chapter last Thursday.

We’ll keep following this evolution here in the Digest.

What’s driving volatility this week

If Friday’s 4.2% pullback in the Nasdaq had you feeling rattled, you’re not out of the woods yet. This week is stacked with catalysts that could move markets.

Wednesday brings the May Consumer Price Index report – the latest data on the Iran War’s impact on consumer costs.

Thursday follows with the Producer Price Index, showing how that same inflation is hitting businesses.

Friday brings the latest Consumer Sentiment report.

All of it feeds directly into the Fed’s calculus ahead of next week’s FOMC meeting, now the most consequential Fed gathering in years.

New Chairman Warsh will have to weigh Friday’s strong labor market reading against inflation running nearly double the Fed’s target – with rate-hike pressure building from multiple directions.

Now, amidst that packed calendar, there’s one more wildcard.

This Friday, SpaceX is expected to price its IPO at a $75 billion valuation – already oversubscribed, according to Bloomberg. It could be the largest IPO in history, arriving in the middle of one of the most consequential macro weeks in recent memory.

Luke has been preparing his subscribers for this moment – and his view may surprise you. Buying a landmark IPO on day one is usually the wrong trade.

Here’s Luke:

The biggest gains from landmark technology IPOs have almost never gone to the investors who bought on day one. They’ve gone to the investors who owned the ecosystem around those companies before Wall Street showed up to reprice it.

That’s exactly the opportunity I’ve been preparing for. I call it the Pre-IPO Backdoor — a small group of publicly traded companies that supply, power, and benefit from both OpenAI and Anthropic, and that I believe will get significantly repriced the moment those S-1 filings land.

The window to get in ahead of that repricing is open right now. I don’t know how much longer it stays that way.

For everything Luke has found – including the specific stocks he thinks you need to own before the IPOs arrive – click here.

Bottom line: Between inflation data, Fed policy, AI disruption, and a historic IPO pipeline, investors have plenty to digest. Buckle up!

Have a good evening,

Jeff Remsburg

P.S. Louis Navellier is doing something I’ve never really seen him do before

The legendary investor is partnering with TradeSmith to unveil a new AI-powered investing approach designed to help investors become more tactical in a fast-moving market.

What’s especially interesting is that you don’t have to wait for the event to get a taste of it. You can use the free ticker tool to check the short-term health of stocks you already own, then join Louis on June 10 for the full presentation.

I’ll bring you more on this tomorrow. But to learn more now, just click here.