Did the U.S. Federal Reserve just kill the stock market? After yesterday’s market crash, it’s tempting to say “yes.”

If you’re looking at the sea of red and thinking the Fed just killed all hopes of a big market rebound, I don’t blame you.

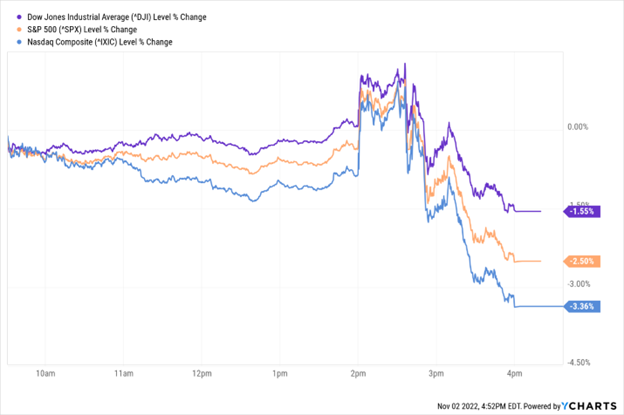

After all, the Fed hiked interest rates by 75 basis points and basically said it won’t stop hiking rates anytime soon. In response, the Dow Jones dropped more than 1.5%. The S&P 500 shed 2.5%, and the Nasdaq crashed more than 3.3%!

It was an ugly day on Wall Street.

But I actually think the stock market rebound is just getting started, and that the Fed will be a big reason why stocks soar over the next 12 months.

Here’s why.

A Process, Not a Moment

Right now, just about everyone is saying that the Fed killed all hopes of a “pivot” yesterday.

But a pivot isn’t defined by the moment when the Fed stops hiking rates. It’s a process that eventually leads to the Fed pausing on rate hikes – but it doesn’t start there.

From our perspective, the Fed pivot is a four-step process that begins with a dovish shift in language/sentiment/rhetoric. That shift in language is followed by a slowdown in rate hikes, then a pause, then rate cuts.

Clearly, the Fed pausing on rate hikes is part of the pivoting process – but it is Step 3, not Step 1.

We believe we got the first step of the pivot process yesterday.

For the first time this year, the Fed openly acknowledged in both its statement and in the press conference that its rate hikes have “lag effects.” That’s critical because previously, the Fed was all about “data dependence.” And the mantra was that so long as inflation data remains above 2%, it would hike rates.

In this meeting, the words “data dependence” were swapped out for “lag effects.” The mantra has changed. The Fed now believes that it has hiked rates fast and high enough that it doesn’t need to respond aggressively to every hot inflation print. Rather, it can afford to wait, let higher rates marinate, and see the lag effects they produce in the economy.

This language shift is the first step. It’s a sign that the Fed is trying to start the end-game for its rate-hike cycle. To that end, it sets the stage for a rate-hike slowdown in December, then a pause in early 2023, then rate cuts in late ‘23.

This is the most likely path forward for interest rates. And as Fed policy follows this path over the coming months, we believe stocks will soar.

The Fed Can’t Be Too Transparent

If the Fed is pacing toward a pause, then why didn’t Powell just come out and say as much yesterday?

Because communicating a pivot while still hiking rates would completely undermine the rate-hiking campaign.

The Fed is hiking interest rates to kill inflation by suppressing economic demand. That only works if economic demand is actually suppressed by the rate hikes. However, if everyone knows that interest rates will stop rising and/or start falling, higher interest rates won’t suppress demand. Everyone will just keep spending and investing on the idea that rates will go lower soon.

Rate-hike campaigns do not work in suppressing economic demand if the consensus belief is that the rate-hike campaign will end soon.

That’s why Powell sounded ultra-hawkish in yesterday’s press conference. Deep down, he knows the Fed is starting its pivot process. But he also knows that he cannot afford to communicate that to the markets.

In fact, he knows that the tougher he sounds and the more the market believes the Fed is not starting its pivot, the better the rate hikes will work in quelling inflation and the faster the pivoting process can happen.

The faster that happens, the quicker stocks will recover. So, in a weird roundabout way, the Fed staying super-hawkish yesterday actually sets the stage for a stock surge over the next 12 months.

The Final Word on the Hawkish Fed

Despite the negative market reaction, we think the Fed pivoting process did start yesterday in the form of a language pivot.

Next up? A slowdown to smaller hikes in December and February, a pause, then cuts.

Throughout this dovish evolution, we believe stocks will move higher. But the recovery will not be smooth. Two steps forward, one step back.

Our investment approach, therefore, is strategic accumulation. Stay tactically long, but save up dry powder for big selloffs over the next few months. They’ll happen frequently. When they do, buy those dips.

But make sure you buy the right stocks.

Find out which are the best stocks to tactically buy on the dip.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.