I know the market looks awful, and the headlines hitting our inboxes aren’t helping. I’ve already seen multiple times that the market has not “looked this bad since the COVID crash of 2020.”

These stories are anything but comforting, but they contain an important silver lining.

On March 25, 2020, I told you…

At this moment, the fear of losing money (FOLM) is the prevailing investor sentiment…

Because so many world leaders, science authorities and media outlets around the world have been urging panic, the voices of reason have no voice. The nonstop doom and gloom muffles any hopeful observations or helpful insights.

The stock market is paying a price for this one-sided narrative.

While the current market situation cannot be blamed for a brand-new pandemic, the identical sentiment is prevailing: fear.

Investors are fleeing the market as they would a spewing volcano, selling off their investments after seeing them tick down, down, down…

But, and as I’ve mentioned before, the best opportunities can emerge in times of turmoil.

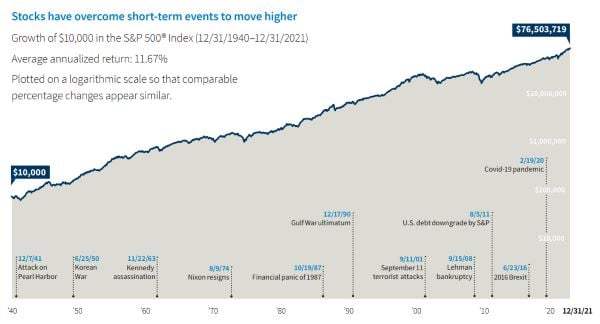

And this is not just an opinion; following every single market crash, the market has rebounded to new highs thereafter.

Just look at this chart from Putnam Investments:

Things are indeed darkest before the dawn, and if you lose your logic to the media, the talking heads, and those that know little about the true nature of the stock market, you very well could miss out on lucrative moves coming down the pike.

But, and of course, this does not mean that you should shirk your risk profile and throw money at stocks like darts in the dark. It pays as much to be cautious as it does to be greedy.

So, today, let’s examine my top three actions to take during market turmoil… and how they can position you best for when the market finds its footing once again.

No. 1: Equip Your Portfolio to Survive AND Thrive

First stop: “Intelligent Asset Allocation.”

When I use this term, I refer to both the precise assets

that make up a portfolio and to the weightings of each asset in that portfolio. (Some portfolios might devote 60% of their allocation to stocks, whereas others might devote just 40% to stocks.)

When it comes to the weightings in an asset allocation, there is no one-size-fits-all formula; each investor must determine the appropriate weighting of his portfolio assets, based on factors like age, risk tolerance, and investment objectives.

A long-standing rule of thumb is that investors should subtract their age from 100 and commit that percentage of their portfolio to stocks. The remaining percentage should reside in relatively safe assets like cash, gold, and short-term Treasury securities.

While each individual must determine his own allocations, this is a good starting point for most investors.

Typical asset allocation strategies fill a pie chart with each of the major asset categories like stocks, bonds, precious metals, real estate, and cash. Each asset category receives a predetermined percentage of the pie.

But for Intelligent Asset Allocation, I take a different approach. I begin by defining the objective of each piece of the pie, rather than focusing on the exact assets that fill each slice.

Specifically, I split the pie into three objective-defined categories:

- Wealth Creation Assets: These offer big upside potential and can create and compound wealth over time; they can really “move the needle” and grow your wealth. But these assets also have the power to destroy wealth. They are two-edged swords. They are risky.

- Wealth Preservation Assets: This category includes just one asset – cash. Investors use the term cash to refer to a variety of cash-like securities – typically, some kind of money market fund that always trades for exactly $1 and pays a modest yield. Money-market funds function well as cash in most environments. The 2008 crisis was one notable exception. Several money market funds “froze” clients’ cash for days or weeks… or months.

- Wealth Insurance Assets: The final piece of the pie contains just two assets, gold and put options. These assets perform well when stocks are performing poorly. That’s why they function as “insurance” against crisis-fueled bear markets, like we suffered in 2008. Unlike a Wealth Preservation Asset like cash, Wealth Insurance Assets can be volatile. They can – and do – produce losses in some market environments. When stocks are rising, for example, put options lose value. Meanwhile, gold’s inverse relationship with stocks is less rigid. But over most time frames during the last five decades, the price of gold has tended to ‘zig’ higher whenever stock prices ‘zag’ lower.

Now that I’ve described the three “pie pieces” of Intelligent Asset Allocation, it’s easier to see how to both fortify your portfolio against a bear market, while also encouraging growth.

No. 2: Buy Your “Forever Stocks” Now

Next, we have something called “Forever Stocks.”

Long-term survival does not rely just on a strong defense; it also requires an effective offense. That’s where “Forever Stocks” come into play – stocks that we nickname our “Top 10” or “Great 8” and hold a sacrosanct position in our portfolio.

Obviously, Forever Stocks will suffer during a severe bear market, just like ordinary stocks. So any investor who holds onto stocks like these during a sell-off is likely to suffer mark-to-market losses.

But these losses are a small price to pay for big long-term gains… assuming the rest of your portfolio is well-positioned.

Investment success cannot depend on clairvoyance. It must rely on the humble admission that the future is unknowable. It must rely on tactics that can succeed in good times — and protect against adversity… no matter when it strikes.

So just like we can never predict exactly when disaster will strike, we can also never predict the precise moment when prosperity will hit.

That’s why we must prepare for both.

Conventional wisdom says that market highs are the worst time to buy stocks… which is the opposite of what we’re experiencing currently, making today — or any day in the near future — a good time to buy them.

No. 3: Just Say “No”

Lastly, we have a simple word: “No.”

Marginal opportunities are what I call “bad risks,” or “asymmetrical risks.” That’s when the potential upside is much smaller than the potential downside.

Here’s an extreme example to illustrate the concept…

- Riding in a barrel over Niagara Falls for a $20 prize. If everything works out perfectly, you win $20. If not, you perish.

Here’s another example…

- Running red lights to get to Disneyland 10 minutes early. If everything works out just right, you make it to the “Happiest Place on Earth” and have to wait 45 minutes instead of an hour for Space Mountain. Or you might get into a horrible accident.

These examples of asymmetrical risk are so obvious that they seem ridiculous.

But many asymmetrical risks are less obvious, like the TV example I gave earlier.

Disciplined investors understand the dangers of these risks; that’s why they begin their analysis by asking “What can go wrong?” rather than “What can go right?”

Disciplined investors understand that investing is optional and that they must be selective.

It’s OK to say “no” to bad risks. Unfortunately, many investors grow impatient. We justify buying richly valued stocks by comparing them to stocks that are even more richly valued. But it is still dangerous to buy stocks that are “less risky.”

It’s no different than camping 40 feet away from a pride of lions because a few other folks are camping only 20 feet away. You might wake up every morning 40 feet away from the lions, just like the morning before. But getting eaten is also possible, if not probable.

Avoiding bad risks is the essential first step toward outperforming the market. And it is especially important to avoid bad risks during a bear market, when even the best stocks will struggle to make headway.

Knowing which stocks to avoid can work wonders for your portfolio — and can protect you from the perils of opportunity cost.

Above all, don’t panic. Set out a disciplined course, and then follow it through good times and bad.

Regards,

Eric