Long time readers know that I use a price earnings ratio of 20 as one of the parameters in my set of screening criteria for dividend stocks.

In addition, anytime I analyze a company, I always end up with a conclusion of whether I find it overvalued or undervalued in terms of P/E relative to the benchmark of 20.

A common question in my mailbox concerns the reasoning behind using this variable, and the reason why I don’t look at historical P/E ranges or industry P/E ranges when looking at companies.

A P/E of 20 implies an earnings yield of 5% by the way. I set this parameter back in 2007- 2008, when yields on treasury bonds were about 5%. If yields on treasury bonds increase above 6 – 7%, I would likely require a P/E of about 15 for screening purposes.

The reality is that I use that P/E of 20 for dividend stocks as a way to screen out companies that trade at a higher P/E than 20. I am not willing to pay for a high valuation above 20 times earnings, especially for mature dividend growth companies. However, I do not use this P/E in a vacuum to select companies. Instead I use it as one of the tools to compare individual dividend stock companies that are valued attractively at the present.

I use this criterion for screening purposes, as a way to narrow down the list of qualified opportunities to a more manageable level. I also use other criterion in my screening, such as requirements for minimum yield (2.50%), 5 and 10 year annual dividend growth (6%/year), and dividend sustainability (payout ratio below 60%).

However for the purposes of this exercise, I am not going to go into much detail on those.

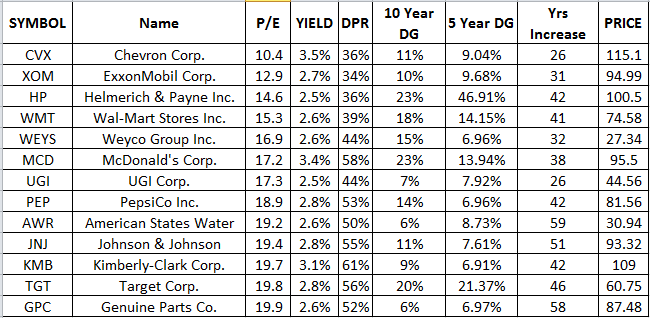

I applied those results to the list of dividend champions, and received the following output:

After I narrow down the list of prospect to a more manageable level, then I compare companies listed in the output. I try to determine which one/ones to buy – based on valuation, earnings stability, growth prospects, portfolio weight.

I analyze each company on the list for qualitative factors as well, such as moats, competitive advantages, brands, pricing power etc. For me earnings stability and opportunities for future earnings growth are paramount. You cannot simply look at yield or P/E ratios without gaining some comfort on stability of earnings and dividend payments, and prospects for future growth in both.

As you can see, I try to allocate my funds in what I believe to be the best ideas at the time. I do not believe in the strategy of accumulating cash, and waiting for lower prices from there. I try to balance obtaining the most earnings yield, with the highest probability of growth, for every dollar I put to use today.

However, I also face the constraint that I can make only 24 – 36 dividend stock purchases per year, and that I want to have a diversified portfolio of securities.

If you look at the screen, Chevron (CVX) is on the top of the list by valuation. Therefore, if I was just starting out, I would analyse and potentially buy Chevron in the first month, then maybe analyse and buy some Exxon Mobil (XOM

) the next, followed by some Helmerich & Payne (HP) in the third month.

If I had not analyzed Helmerich & Payne and Weyco Group (WEYS) before, I would need to add them to my list for further research, before I allocate any capital to them. I have done what I describe in this article for the past 6 years, and it has worked fine for me.

I do not look at P/E ratios for industry and in terms of historical ranges. To understand why, let’s walk through an example where you have two companies, one which typically sells at 8 – 12 times earnings and another which sells at 18 – 24 times earnings. Both grow dividends at 7% per year, and both yield 2.50%. We would also assume that earnings are relatively stable in both, there is an equal history of dividend growth, and both companies have some sort of durable competitive advantage.

Company A trades at the top end of its P/E valuation range (P/E of 12), while company B trades at the low end of its valuation range (P/E of 18). If I was just getting started investing, I would choose company A any time over company B. This is because I am getting more earnings yield for each dollar I invest. This also provides the company with certain options such as share buybacks to boost earnings per share. This could be more accretive to shareholders of company A than for those of company B. It doesn’t matter that the P/E is at the top of the range for company A, because I am getting more value for my dollars invested.

Of course if I already have exposure to company A, I would then start allocating funds to company B, which is the next best thing to put my money in. I will also do it because I like to be diversified and not keep all my eggs in one basket.

So as you can see, my method of screening provides a very good launching pad for evaluating opportunity cost, and selecting the most optimal investments at the time. It is superior to looking at past P/E ratios and industry P/E ratios, because it focuses on finding value today, relative to the rest of the market opportunities of the day.

To summarize, I use the P/E as one of the tools to narrow down list of prospects to a manageable level, and then help me to choose between dividend stocks. This low P/E, coupled with my qualitative and quantitative analysis of companies, helps me identify and purchase shares in the best bargains at the present moment. I have money to invest every month, so this P/E of 20 helps me avoid overvalued securities, and helps me to find the best bargains in the market at the time I have to allocate my capital.

Full Disclosure: Long CVX, XOM, WMT, MCD, PEP, JNJ, KMB & TGT