Advanced Micro Devices (AMD) is looking to circumvent its market juggernaut competitor, Intel (INTC) through diversifying into higher margin businesses and cutting expenses. AMD has been working on a turnaround since 2012, and with a backwind on its core processing business, AMD looks like it may be on track to turn the corner next year.

AMD: Restructuring Plan

At the end 2012, AMD found itself needing to re-align resources to more productive areas, divest under performing assets and make certain assumptions about future prospects. AMD’s processors were inferior to its rivals’, revenues were in free fall and AMD’s stock price dropped to under $2 a share.

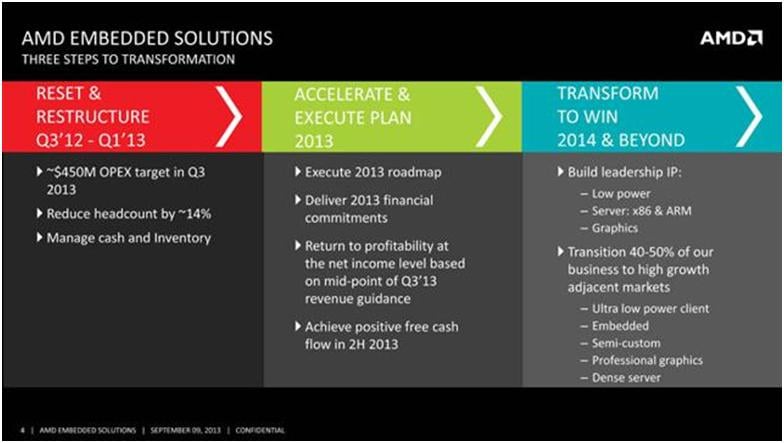

To right the ship, AMD put forth an aggressive three-phased turnaround strategy: Reset and restructure; accelerate and execute; and transform to win.

Phase 1 – Reset and Restructure

By the end 2012, AMD’s business had shrunk to the point that costs were dramatically misaligned with revenues. To fix this problem, AMD’s first phase began with rightsizing the company.

AMD cut headcount of between 20% – 30% and entered into a sale-leaseback of its facilities. So, AMD’s operating margins stabilized going from a negative 20% in 2012 to a positive 2% in 2013 and nearly 6% on a trailing-12-months basis as of last quarter. This is a far cry from the 12-13% operating margins produced in 2009-2010 but is enough to buy time as AMD executes its restructuring plan.

Phase 2 – Accelerate and Execute

With the time afforded by the cost savings initiatives, AMD shifted its focus from a market it was impossible for them to dominate in, the production of central processing units, to focusing on the development of graphics processing units.

AMD and Nvidia (NVDA) were both challenging Intel’s strong hold in the GPU market. AMD believed it could make a bigger impact by driving competitive products into this market than the CPU market, therefore increasing revenues and market share.

The gamble initially paid off, with AMD’s GPU market share surpassing Nvidia’s in 2013

, but backed off a bit in a market that showed some recent declines. In addition, AMD missed production windows for the PC market in Q4 2013, causing a significant decline in the usage of its accelerated processing unit, which is a combined CPU/GPU, and affecting market share.

Earlier this year, AMD announced that its Firepro GPU would be in Apple’s (APPL) new flagship desktop, MacPro. This has allowed AMD to go back on the offensive and has now garnered a 25% market share within professional graphics hardware shipments against Nvidia’s 75%. While a significant market share gap in this space still exists, AMD is making progress.

Phase 3 – Transform to Win

Transforming to win is the phase that AMD is currently entering and is the most important. Expected to be completed by the end of 2015, phase 3 will seek to generate new revenue sources to diversify AMD’s revenue risk into multiple markets.

Traditionally, AMD has competed directly with Intel in the x86 architecture space, but as executed in phase 2, AMD has focused on broadening its revenue to include more GPU and APU products. The goal of the transformation stage is to transition 40% – 50% of AMD’s business to high-growth, adjacent markets that include the following:

- Ultra low power clients (shifting chip development focus from not just horse power but also energy efficiency)

- Embedded chips (chips in games, GPS devices, digital signage, medical devices, gaming machines, calculators, etc…)

- Semi-custom (chips for clients like Microsoft and Sony to power their gaming systems)

- Professional graphics (large and growing market)

- Dense servers (primarily used in data centers they are high-powered, low heat computer servers that have a small physical footprint compared to traditional servers)

Although the ebbs and flows of the personal computer industry will still have a dramatic impact on AMD’s bottom line, diversifying into these adjacent markets where AMD can better compete will lessen the effect that the on-going cat and mouse game between AMD and Intel for faster CPU chips has on AMD.

AMD Progress – Transformation’s Success Will Drive Stock Price in 2015

Prior poor execution (AMD’s Bulldozer CPU architecture failed to thrill customers) and a sluggish PC market continue to wear on AMD profits but are getting better. With the economy getting back on track, computer workstations showed progress in the second quarter of 2014 with growth of 10.8% from the first quarter and 11.5% year over year.

Although overall stronger PC sales growth will help, AMD’s continued shift on adjacent markets will minimize its profit exposure. In the second quarter of 2014, AMD posted only $9 million in operating profits from its computer solutions segment, but $83 million from its graphics and visual solutions segment.

AMD stock is a short-term hold, but look for indications as to when AMD will be releasing a new chip design to replace its failed Bulldozer architecture. Once known, the stock should see upwards movement as the architecture is implemented into new systems.

Also, look for any indications that AMD’s new business segments are showing signs of rapid expansion to the point of overtaking its PC business, which may indicate the need to re-evaluate AMD stock for potential upside.

As of this writing, Kenneth Fick did not hold a position in any of the aforementioned securities. Write him at kfick@piercethefog.com or follow him on his blog at www.piercethefog.com.