I have spoken a lot about analysts’ favorite stocks to buy. But along with buying comes the stocks to sell. You have to know when to cash out at the right time. This is all the more important given the current market conditions. Even top-rated stocks are getting hammered right lately.

Luckily Morgan Stanley is out with its list of the stocks you should sell now. These stocks all have a “sell” rating from the firm and “an unfavorable risk-reward skew.” As the firm explains, these companies are “facing challenges that are independent of cyclical trends.” The worst part is that they could even lose over half their value in the next 12-18 months.

These challenges include everything from market-share loss and rising competition to deteriorating end markets and cost pressures. In short, when it comes to these stocks, save your money. There are much more worthy investing opportunities out there.

Here I also use TipRanks market data to get a better idea of where these stocks are heading. What’s the rest of the Street saying, for example? Let’s take a closer look these even stocks to sell:

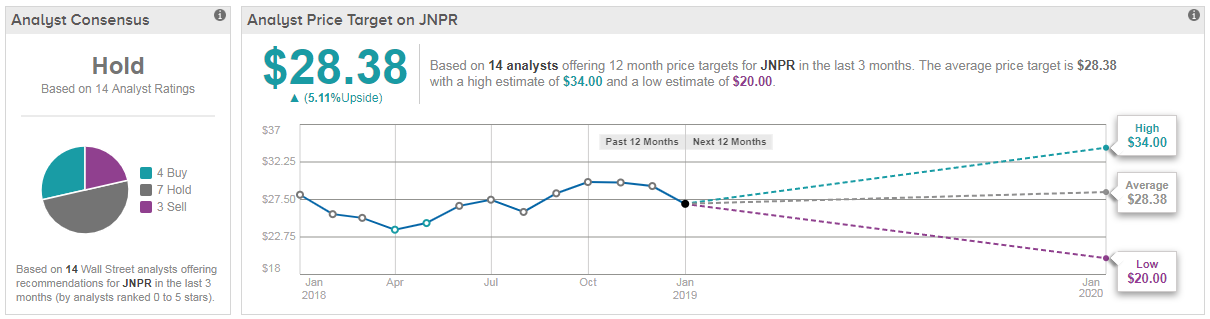

Juniper Networks (JNPR)

Morgan Stanley says “sell” networking and cybersecurity stock Juniper Networks (NYSE:JNPR). The firm isn’t alone in its bearish take on this stock. Goldman Sachs’ Rod Hall (Track Record & Ratings) is also advising investors to spend their money elsewhere — and put this on their list of stocks to sell when the price is right.

The analyst stated “we would advise investors to use any strength to reduce exposure as we believe 2019 forecasts remain overly optimistic for Routing just on the basis of deflation in the data center.”

Hall continued: “Beyond this we believe that 2019 is a year of routing architecture transition in U.S. carrier networks toward lower cost ports and software as Verizon’s 5G build gains some momentum as does the fully automated network solution that we believe comes along with 5G.”

Indeed, long-term concerns — and a lack of catalysts — keep Rosenblatt’s Ryan Koontz in the bear camp. “We expect continued pricing and top line pressure to drive gross margin weakness and earnings below consensus over 4Q18 through FY19” he writes.

Both Hall and Koontz believe the stock looks overvalued at current levels. Hall is modelling for a potential 25% drop in shares; Koontz for 10%. That’s with shares already down 2% on a three-month basis. Not that JNPR doesn’t have its supporters. Four analysts still rate the stock a “buy.” Hence its “hold” Street consensus. Interested in JNPR? Get a free JNPR Stock Research Report.

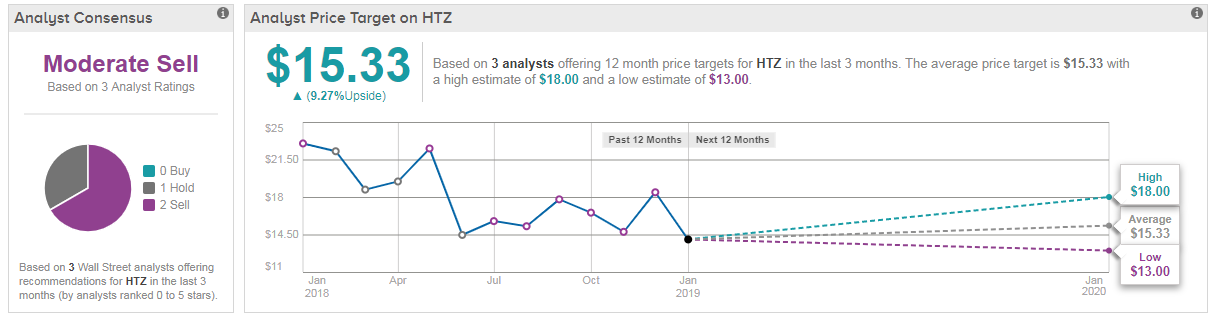

Hertz Rental (HTZ)

Leave while you can! Morgan Stanley’s Adam Jonas (Track Record & Ratings) has just reiterated a “sell” rating on Hertz Global Holdings (NYSE:HTZ). Although high prices in used vehicles “saved” third-quarter results, he is troubled by a dangerous trio of rising finance costs, secular pressures and weakness in rental car pricing.

According to the firm, the rental-car company is highly exposed to the peaking used car and auto credit markets.

“We continue to believe HTZ confronts substantial secular problems in car rental manifesting in slower growth and cost headwinds for depreciation and cost of funds,” writes Jonas. “We would use the recent stabilization of the stock price as an opportunity to reduce exposure.”

He has a $15 price target on the stock (7% upside from current levels). Bear in mind, shares have already plunged 35% year-to-date. And as we can see above, the company holds a fairly damning “moderate sell” Street consensus, making this a smart stock to sell. Get the HTZ Stock Research Report.

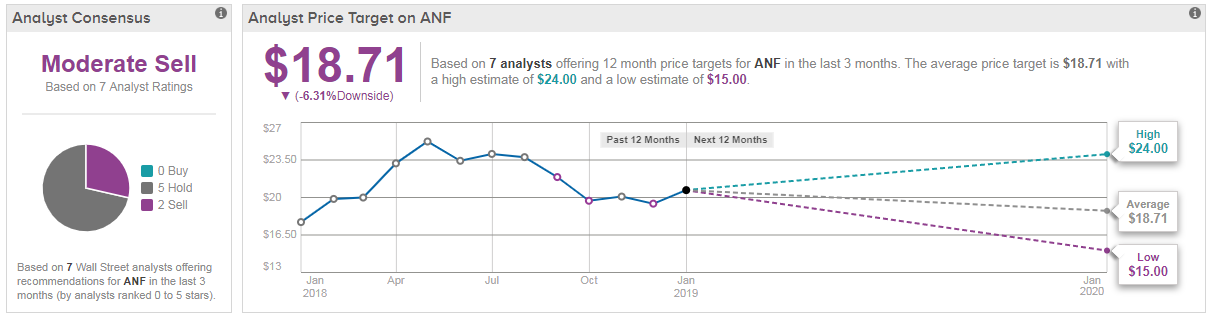

Abercrombie (ANF)

It’s best to put struggling fashion retailer Abercrombie & Fitch (NYSE:ANF) on your stocks to sell list for now. That’s the advice not just of Morgan Stanley, but the Street in general. This is a stock with a “moderate sell” Street consensus, and an average price target that suggests shares could fall 12%.

However, Morgan Stanley’s price target of just $14 suggests a much deeper pullback of 34% is possible.

ANF is in the midst of a major organizational, product and strategy overhaul in an effort to stabilize its top-line efforts which are accelerating share gains out of Hollister (58% of 2017 sales) and slowly taking root in the A&F brand (42% of sales).

“These updates could not be more necessary, in our view, with the company ending 2016 with productivity and profitability at trough levels, including a (0.3%) EBIT margin” writes RBC Capital’s Brian Tunick (Track Record & Ratings).

Another worrying thought — with 25% short interest, expect shares to remain volatile. Right now, the stock is trading down 18% in the last six months, but has gained 7% over the last three months. Get the ANF Stock Research Report.

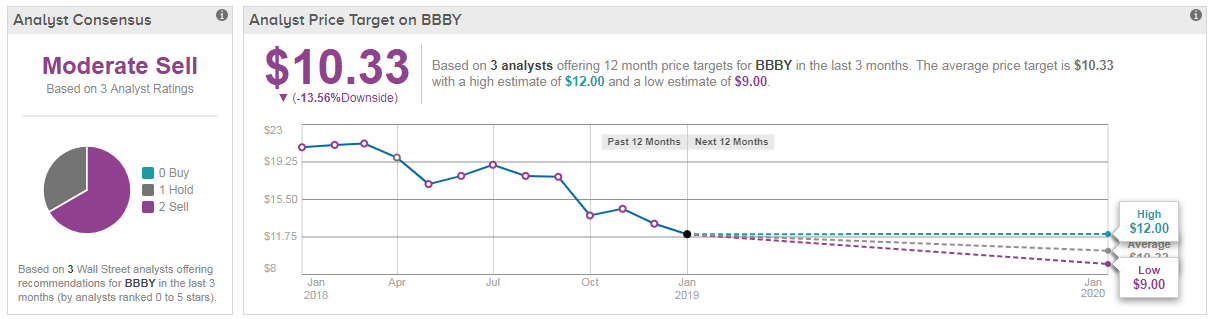

Bed Bath & Beyond (BBBY)

The situation for home-retail store Bed Bath & Beyond (NASDAQ:BBBY) is looking increasingly perilous.

- Shares have crashed 44% in the last one year.

- The Street consensus is “moderate sell,” with analysts tilting towards sell over hold.

- Even after such dramatic losses, the average analyst price target of $10.50 still indicates shares will fall rather than rise (the current share price is $12.06). So we are looking at downside of 14% right now.

- Citi has just lowered its PT from $13 to $10, while Wolfe Research’s PT has also shrunk from $15 to $10

- And on top of all that, Argus analyst Chris Graja (Track Record & Ratings) downgraded Bed Bath & Beyond to Hold from Buy. He cites a lack of confidence in the company meeting long-term targets, ongoing gross margin pressure, declines in store traffic and overspending.

Let’s close this stock with the words of Wells Fargo’s Zachary Fadem: “With the benefits of Toys ‘R Us closures, a strong consumer environment and a host of ambitious company initiatives failing to materialize in our view thus far, we remain bearish … and see further downside risk ahead.”

Add in the threat of e-commerce giant Amazon (NASDAQ:AMZN), and you can see why it’s best to put this is the “stocks to sell” pile. Get the BBBY Stock Research Report.

Fitbit (FIT)

Even a recent earnings beat was not enough to convince the Street that Fitbit Inc (NYSE:FIT) is a worthy investing proposition.

The fitness tracker maker has had a hard time on the market since it went public in 2015. And it doesn’t look like a turnaround is coming any time soon. In fact, in the last five years, share prices have almost halved.

Now Morgan Stanley says this is a “sell” rating stock, with a price target of just $4. From current levels that means we are looking at downside potential of over 25%.

The firm’s Yuuji Anderson (Track Record & Ratings) remains skeptical that the improvements with Charge 3 and Versa can make up for ongoing legacy declines. Fitbit Charge 3 is a heart rate fitness tracker that tracks activity, exercise and sleep, while the Versa is FIT’s $199 smartwatch, and answer to the Apple Watch.

Anderson thinks the current pace of new features is not enough to stabilize declining demand this year and expects shares to underperform into 2019.

Most damning is the feedback from Citi analyst Jim Suva. He maintains a “sell” rating on the stock with a $5 price target. The problem: even though they may be cheaper, Fitbit’s new products “are not as smart as the Apple watch”. Overall, the Street consensus on FIT stands at a slightly more positive “hold.” Get the FIT Stock Research Report.

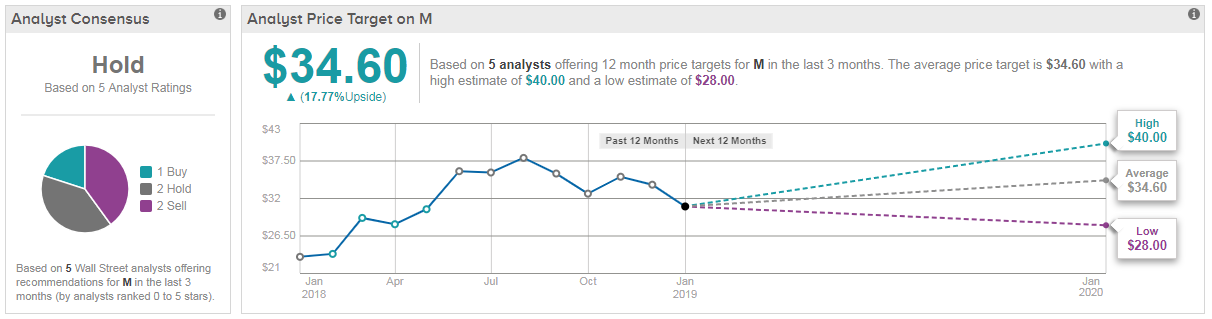

Macy’s (M)

Hot on the heels of Morgan Stanley’s Sell rating for Macy’s (NYSE:M) comes another bearish turn. This time it’s from Atlantic Equities analyst Daniela Nedialkova (Track Record & Ratings). She has just downgraded M from “hold” to “sell.” That’s with a $28 price target, exactly in line with Morgan Stanley. From current levels that means both firms see prices dropping 5%.

Nedialkova puts her move down to unrealistic market expectations. She comments “With prior year comparisons turning tougher for the next several quarters, we see expectations as too high. Macy’s is continuing to execute on its strategic initiatives but we do not expect to see a material impact in the numbers until later in the year.”

For example, the company is currently investing $200 million in its Growth50 initiative. This is an experimental retail strategy offering expanded curated merchandise to 50 key locations.

However these rewards will take time to materialize, and in the meantime expect trading to stay choppy: “As we expect most of 2019 will still be a year of transition, and with upcoming difficult prior year comparisons, we expect more volatility from the stock and given currently high expectations, see downside risk.” Get the M Stock Research Report.

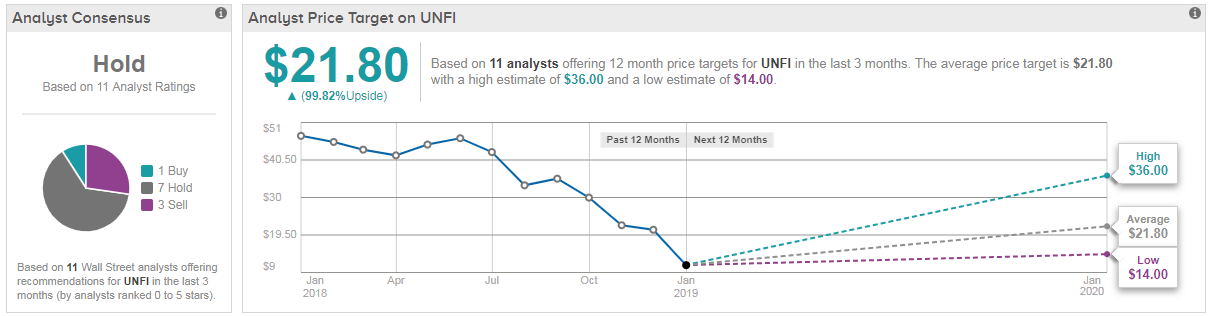

United Natural Foods (UNFI)

{kind=link}

United Natural Foods (NYSE:UNFI) is a distributor of natural and organic and specialty foods across the U.S. and Canada. Its also the primary distributor to Amazon’s Whole Foods Market.

However, this isn’t enough to save the stock from a pretty poor stock rating. Not one top-performing analyst rates the stock a “buy,” and the overall consensus is “hold.” A lot of people put this on their stocks to sell list already.

That’s with shares losing a disastrous 75% of their value in the last year. As you can imagine, analysts are not recommending a buy-the-dip type scenario here. For example, Morgan Stanley’s Vincent Sinisi (Track Record & Ratings) has a “sell” rating on UNFI.

He made the call following the news that UNFI would buy supermarket chain SuperValu. The deal was valued at a cool $2.9 billion. While “notable potential growth opportunities exist” for the combined company, integration risks leave Sinisi concerned.

First quarter results provided fresh disappointment — and caution. SuperValu reported a very soft first half of the year, with wholesale EBITDA declining more than 20% to $131M from $165M in the prior year.

“With a bottom less clear in UNFI shares and limited margin for error given very high leverage levels, we believe investors should tread cautiously from here” sums up Oppenheimer’s Rupesh Parikh. “Execution at SVU remains the key risk, especially against the current difficult grocery backdrop” he concludes. Get the UNFI Stock Research Report.

TipRanks.com offers exclusive insights for investors by focusing on the moves of experts: Analysts, Insiders, Bloggers, Hedge Fund Managers and more. See what the experts are saying about your stocks now at TipRanks.com. As of this writing, Harriet Lefton did not hold a position in any of the aforementioned securities.