Editor’s note: This article is part of InvestorPlace.com’s Best Stocks for 2019 contest. Eric Fry’s pick for the contest is Syrah Resources (OTCMKTS:SYAAF).

If Syrah Resources Ltd. (OTCMKTS:SYAAF) were a graduating high school senior from the Class of 2019, it might be named the “Least Likely to Succeed.” On the other hand, this same “student” could be the one who flies a private jet to the 10-year reunion… and then rolls up to the event in a Bugatti!

Simply stated, this company is capable of achieving great success… or great failure.

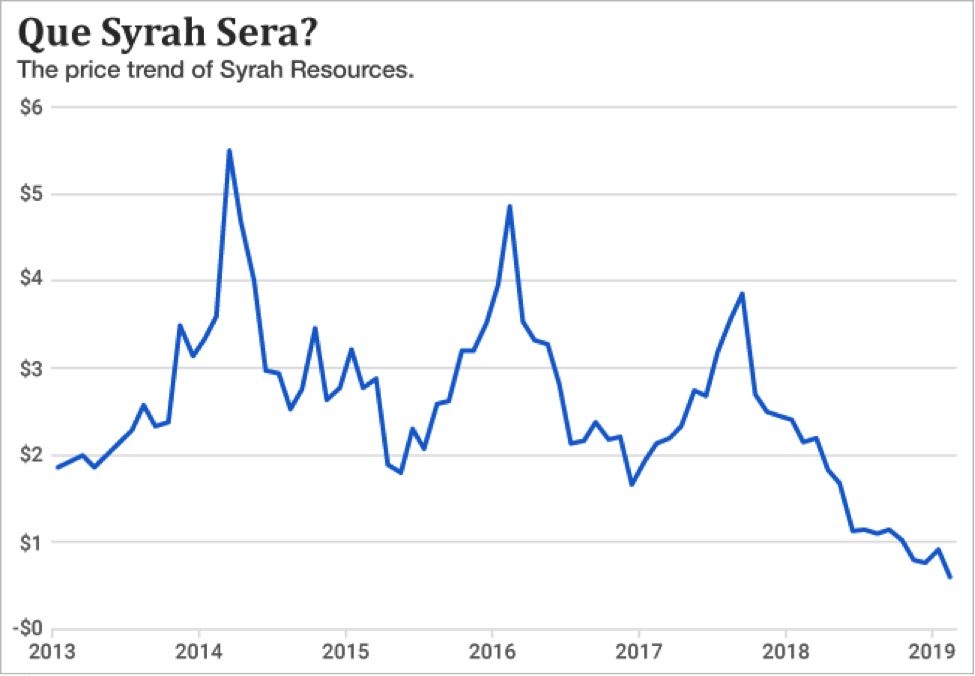

At the moment, however, investors are pricing SYAAF stock for a future of disappointment. It touched a new seven-year low this week and shows no sign of heading in a new and positive direction.

The problem is cash flow. Syrah still isn’t producing any. So, let me repeat what I stated three months ago when we last checked in on this company: “Unless [Syrah] starts producing positive cash-flow soon, it is more likely to be a zero than a hero.”

The company has made modest progress toward generating cash from its operations, but not enough to prevent its stock from tumbling 45% through the first six months of this year.

Syrah’s Key Metal

For readers who may not be familiar with this company, let’s review…

Syrah operates the world’s largest and highest-grade graphite mine. It’s called the Balama Mine, and it sits in Mozambique. Balama is home to about 50% of the world’s known graphite reserves.

Syrah’s Balama operation contains an enormous graphite resource with a projected mine life of more than 50 years. According to Mining Global, it could provide 40% of the world’s natural graphite within three years.

So why should anyone care about graphite?

Because it is one of the main “battery elements.” Think nickel, copper, and lithium. These elements are essential for current battery technologies.

But graphite plays a very unique role in battery chemistries because it is the element that forms the anode material in every electric vehicle (EV) battery.

All four of the leading EV battery technologies use slightly different combinations of metals like nickel and cobalt to create their cathodes.

But the anode material in all four is 100% graphite. That makes graphite “agnostic” about which battery chemistry becomes the most popular or prevalent.

Therefore, as EVs continue to gain market share, demand for graphite should trend higher. Syrah estimates that global demand for natural graphite jumped 10% last year. And over the next decade, graphite demand is likely to jump seven-fold.

SYAAF Has a Promising Plan

All else being equal, rising demand should produce higher graphite prices. But in the here-and-now, graphite prices are not high enough for SYAAF to operate profitably… at least not yet.

That’s the bad news. The good news is two-fold:

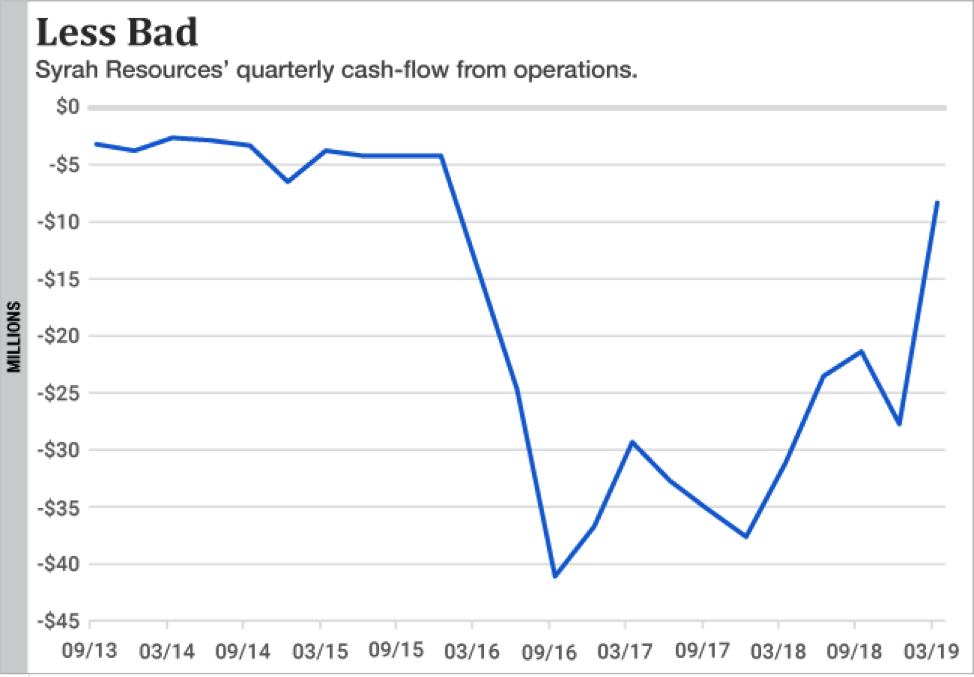

- Syrah has been narrowing its operating losses, mostly by mining its graphite more efficiently. The chart below tells the tale. Quarterly cash-flow from operations has improved from a low of -$41 million in September 2016 to -$8 million in the most recent quarter. But a minus sign is still not a plus sign.

Click to Enlarge - SYAAF is in the process of issuing new debt and equity to raise an additional $78 million. But this new cash isn’t coming cheap. In order to attract these funds, the company is issuing stock at $0.56 a share — a steep 20% discount to where the stock was trading before the company announced this financing.

Unfortunately, that’s the price mining companies — and their shareholders — pay for failing to produce positive cash-flow.

Syrah is forecasting a negligible cash burn during the current quarter, which would leave it with $43 million at quarter-end. But with this new financing, the company’s cash pile would nearly triple to about $120 million.

That cash would give Syrah a lot breathing room — and cover a lot of unexpected setbacks, should any occur.

So now we’re in a wait-and-see period.

SYAAF has disappointed its shareholders so many times that it will not receive the benefit of any doubt. But if the company can start to deliver pleasant surprises, the stock could soar.

Positive cash-flow is the first critical hurdle it must clear. From there, the sky is the limit.

Eric J. Fry has been a specialist in international equities for nearly two decades. He is known for his extraordinary long-term track record, which includes numerous “10-bagger” calls. And Eric’s track record on the short side is just as remarkable. Now, the author, former hedge fund manager, and world-renowned analyst brings you the power of expensive, institutional-quality research in his recently-launched newsletter, The Speculator. Click here to learn more.