The mighty and unstoppable Shopify (NYSE:SHOP) stock — which from late December 2018 to late August 2019, rattled off an impressive 200% gain in almost straight-line fashion — finally hit a road-bump. In September 2019, amid a massive shift in equity markets from momentum names to value names under the impression that the U.S. economic outlook is improving, SHOP stock got killed.

Month-to-date, Shopify stock is down nearly 10% — and we are only a few trading days into September. For what it’s worth, this marks the biggest and sharpest correction in SHOP stock since late 2018.

Is the epic rally in SHOP stock over? Or is this simply an opportunity to buy the dip in a secular winner?

I think the latter. But patience is key. At current levels, Shopify stock is still fundamentally overvalued. Plus, the unwinding of the momentum trade could persist. But if the current weakness continues for a bit longer, then the stock will become undervalued and the momentum-trade unwinding will be over.

Consequently, investors should welcome this weakness in SHOP stock. This high-flying equity simply went too far, too fast. Now, it’s coming back down to earth. Let it come down some more. Then, once the fundamentals, optics, and technicals all give buy signals, go ahead and buy the dip in this long-term winner.

The Fundamentals Make More Sense Now

In plain English, the Shopify growth narrative has been so good that investors crowded into SHOP stock in 2019 without regard for valuation. This caused SHOP stock to explode higher. For a long time, it exploded higher with improving fundamentals. But recently, shares simply got too high — that is, the valuation started to lose touch with the fundamentals.

Now, Shopify stock is correcting lower. Eventually, the valuation and the fundamentals will be in sync again.

In numbers, Shopify’s gross merchandise value (GMV) was about $40 billion last year, up an impressive 56% year-over-year. But that $40 billion represented just about 1.5% of all global e-retail sales. Importantly, Shopify’s share of the global e-retail sales pie has climbed from 0.8% in 2016 to 1.1% in 2017, and to 1.5% in 2018. Further, it projects to be around 1.8% this year. In other words, you have a rapidly growing player in a huge addressable market.

Project it out. Given the current decentralization, the rising gig economy, and direct retail trends, it is very likely that Shopify’s e-retail share continues to scale towards 5% or more by 2030. Additionally, some contribution will come from the offline segment (which Shopify is aggressively expanding in). Assuming so, Shopify could easily be a $500 billion to $600 billion-plus GMV player by 2030. That makes sense given that Shopify, at scale, reasonably projects as the store-front for millions of merchants globally.

Gross margins are big (55%-plus), and the opex rate (also around 55%) has tons of room to fall with robust revenue scale. I think Shopify will wind up a 60% gross margin player with a 30% opex rate, implying 30% operating margins on billions of dollars in revenue. Net-net, I think that earnings per share by 2030 will wind up somewhere between $20 and $30.

Based on an application software industry average

35-times forward multiple and 10% discount rate, that equates to a 2019 price target for SHOP stock of somewhere between $270 and $400. That averages out around $340, roughly where SHOP stock is trading today.

The Optics Will Improve, Soon

In addition to the fundamentals starting to make sense again, the optics — which have turned sharply negative over the past two weeks — will start to look good again within the next few days to weeks.

The idea here is pretty simple. Throughout the summer, investors were rattled by recession and economic slowdown fears. Those fears ultimately caused investors to ditch economically sensitive value stocks that required good numbers to head higher. Conversely, they piled into momentum growth stocks like SHOP that didn’t require a good economy to head higher (because they had such strong secular tailwinds).

Click to Enlarge

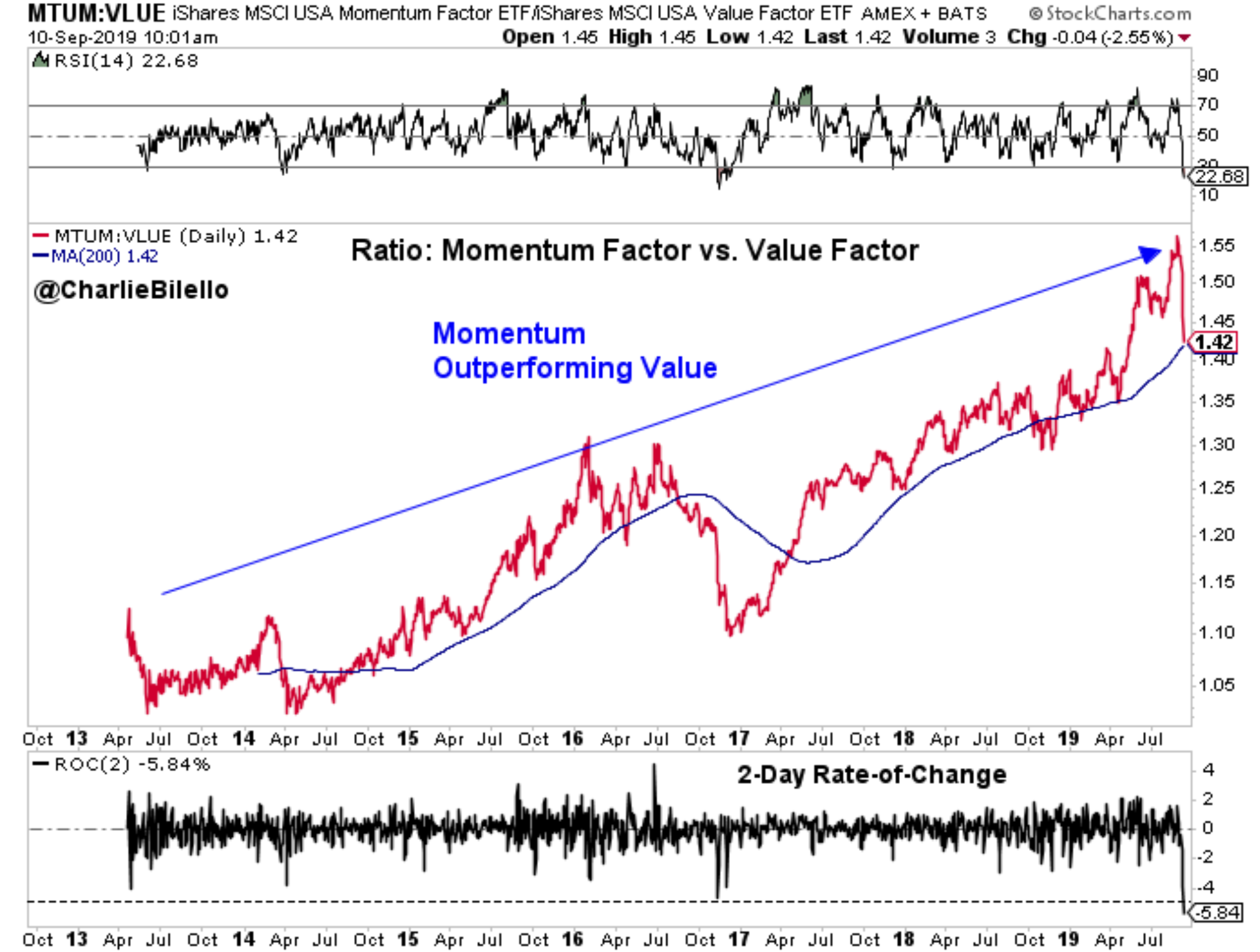

Now, though, signs are starting to emerge that the U.S. economy is going to be fine, meaning that the recession fears which dominated the investment landscape over the summer were overstated. Investors are responding by unwinding the crowded momentum trade which dominated the summer. That means they are selling momentum growth and buying beaten up, economically sensitive value stocks.

This unwinding could persist for the next few days to weeks. But it will end, and soon. As the attached chart shows, the momentum/value performance divergence widened to decade highs this summer. The current shift out of momentum and back into value is just a reversion to the trend line, which is still pointing sharply up.

We are getting close to fully reverting to that trend line. Once we do fully revert there, momentum stocks will likely come back in favor, meaning Shopify stock should start to head higher again soon.

Bottom Line on SHOP Stock

SHOP stock is a long-term winner. But in the summer of 2019, this long-term winner sprinted ahead of the fundamentals. That is, Shopify stock became too richly valued for its own good.

Now, Shopify stock is very naturally and healthily retreating to more sustainable and fundamentally supported levels. This retreat isn’t over yet. But it will be over and soon.

As such, investors should embrace the recent weakness in SHOP stock. Ultimately, it will turn a golden buying opportunity into a long-term winner.

The level I’m watching? $300. I’m not sure SHOP stock will get there. But I hope it does, because I think that would be a great level to add more exposure for the long haul.

As of this writing, Luke Lango was long SHOP.