Throughout March, April and May, the novel coronavirus pandemic – formally dubbed Covid-19 – grounded United Airlines (NYSE:UAL) shareholders. United Airlines stock dropped from about $80 in February, to below $20 by mid-May.

Then a few things happened.

One, states across the U.S. started reopening things. Two, consumer behavior started to normalize alongside broader re-openings. Three, air traffic levels rebounded dramatically as consumer behavior normalized.

In sum, UAL stock flew higher in the last two weeks of May and the first week of June. By June 8, United Airlines stock was trading just shy of $50.

Over the past week, this recovery rally has been short-circuited by fears of a potential “second wave” of Covid-19 emerging across the U.S.

These fears are overblown. Not the fact that a second wave is coming. It appears to already be on the way. Rather, the idea that a second wave will kill the air travel industry’s recovery.

It won’t. Air travel trends will continue to improve over the next few months. As they do, UAL stock will fly higher.

Here’s why.

The Recovery Is Here to Stay

The U.S. economic recovery – and by extension, the airline sector’s recovery – that has materialized over the past few weeks is here to stay for the next few months.

Long story short, U.S. consumers got cabin fever. After being locked up in their homes through March, April and May, they got sick and tired of living in fear of a virus that the newest science showed was only slightly more lethal than the seasonal flu.

Consumers started doing things again. They started going to malls again. They started going to beaches and restaurants again. A lot of them went to protests, which were essentially the paragon of the social gatherings which the CDC has been telling people to avoid for the past few months.

Click to Enlarge

Yes, there has been a spike in cases and hospitalizations in certain states because of these activities. But not a significant spike. We are talking 250,000 new cases in June, and about 10,000 new deaths.

That may seem like a lot. But tens of millions of Americans have increased their mobility over the past few weeks, so in context, the overwhelming majority of these consumers who are going to malls, beaches and restaurants again, are not contracting Covid-19, let alone being hospitalized or dying because of the virus.

In other words, it increasingly appears that most consumers have made up their minds: they can sustain a quasi-normal lifestyle, which mitigates virus risks via social distancing and mask wearing, yet still allows them to do things.

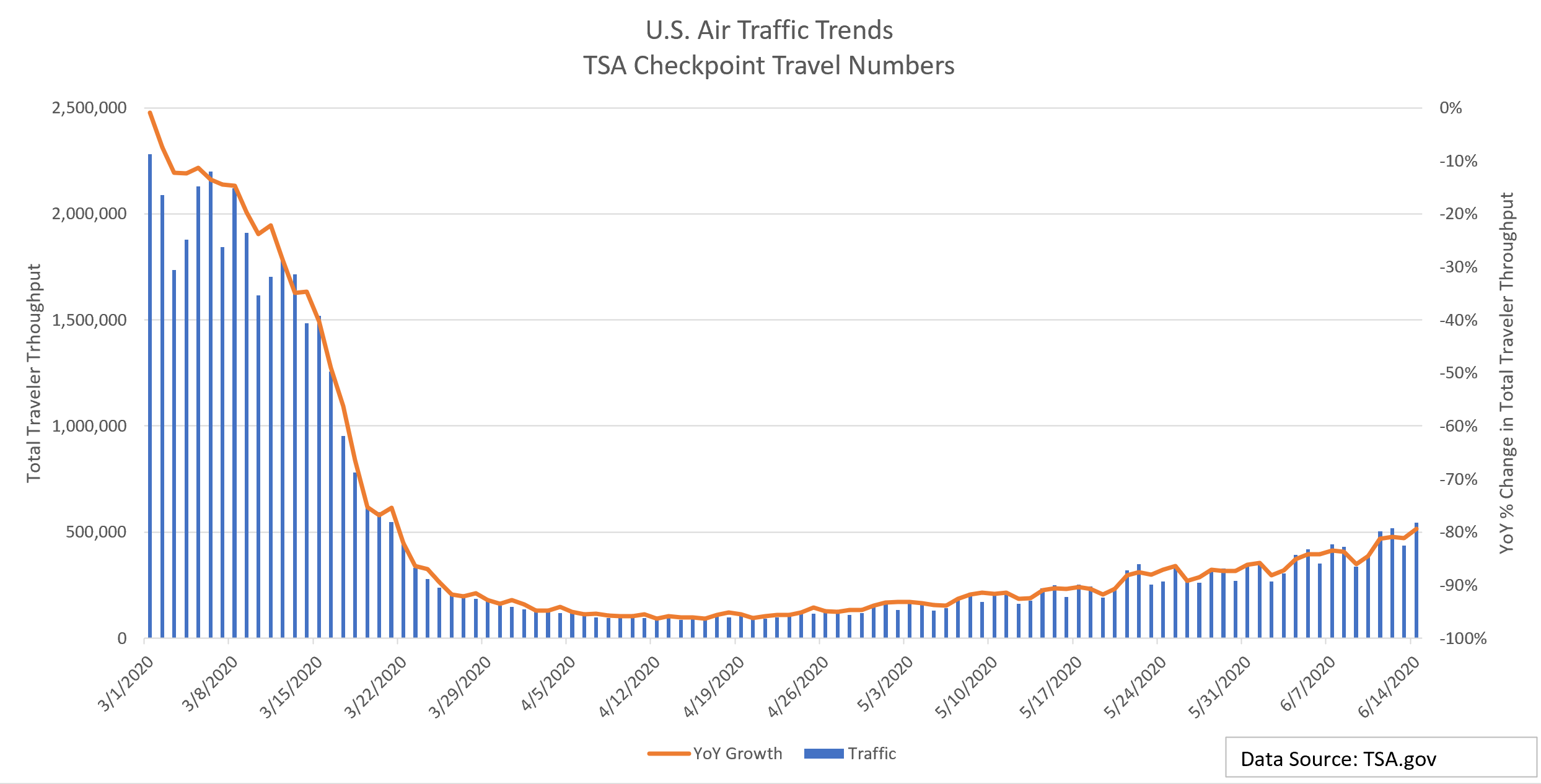

One of those things is air travel. That’s why, from its mid-April lows to today, TSA recorded total traveler throughout at airports has risen more than 500%.

Sure, total traveler throughput is still down 79% year-over-year as of mid-June. But that’s up from 90%+ declines throughout April and May, and represents the first time that the year-over-year decline has been less than 80% since March 21.

The emergence of a second wave won’t derail this recovery.

Pulling from the aforementioned logic, consumers appear committed to living their lives again, with cautious measures, and the emergence of a second wave will increase those cautious measures but not scare consumers back inside again.

Thus, between now and the end of the year, air traffic trends will significantly improve.

As they do, UAL stock will roar higher.

United Airlines Stock Is Undervalued

By my numbers, United Airlines stock is significantly undervalued, if air traffic trends can largely normalize by 2022 (which seems entirely likely).

My base case model on United Airlines assumes the following:

- United’s revenues get slammed in 2020, before strongly rebounding 2021, and sustaining that recovery in 2022. Fiscal 2022 revenues come in around $40 billion, versus $43 billion in 2019 revenues, with the difference being accounted for by marginal loss of business and personal travel.

- United’s pre-tax profit margins get whacked in 2020, before recovering in 2021 and 2022. Importantly, steady-state profit margins going forward will be lower than 2019 profit margins, because of higher costs associated with more thorough and regular cleaning. I’m looking for 7% pre-tax profit margins in 2022, versus 9%+ in 2019.

- United’s share repurchase program essentially grinds to a halt. The 2022 share count is roughly equivalent to the current share count.

Under all those assumptions, my modeling suggests that $8 in earnings per share is doable by 2022. Based on a historically average forward earnings multiple of 8, that implies a 2021 price target for UAL stock of $64.

Shares trade below $40 today.

Bottom Line on UAL Stock

United Airlines stock was beaten and bruised by Covid-19 in April, March and May. But it appears that the worst of the Covid-19 crisis is in the rearview mirror. Going forward, consumer behavior will normalize, and air travel trends will improve. As they do, grounded UAL stock will fly high again.

Luke Lango is a Markets Analyst for InvestorPlace. He has been professionally analyzing stocks for several years, previously working at various hedge funds and currently running his own investment fund in San Diego. A Caltech graduate, Luke has consistently been rated one of the world’s top stock pickers by various other analysts and platforms, and has developed a reputation for leveraging his technology background to identify growth stocks that deliver outstanding returns. Luke is also the founder of Fantastic, a social discovery company backed by an LA-based internet venture firm. As of this writing, he did not hold a position in any of the aforementioned securities.