The agreement last month by SPAC stock Pivotal Investment Corporation II (NYSE:PIC) to merge with privately held electrical vehicle company, XL Fleet will be a big deal for PIC stock investors and the target company’s owners.

Shares of the special purpose acquisition company should move substantially higher both before and after the deal’s expected fourth-quarter closing. The merged company will then be called XL Fleet, trading under a new ticker, XL. There are several reasons why PIC stock should move up in value.

Why PIC Stock and XL Fleet Are Undervalued

XL Fleet is a substantial player in the commercial EV market with a lot of momentum vs. its peers. This company, which makes hybrid and electric vehicle powertrains for commercial and municipal fleets, is head-and-shoulders ahead of its peers, including Hyliion Holdings (NYSE:HYLN) and Workhorse (NASDAQ:WKHS).

To begin with, XL Fleet is already producing revenue. The management team’s presentation (p. 25 and shown below) — including summary financials for 2019 and the next five years are shown — shows revenue last year was $7.2 million, with$21 million forecast for 2020. After that, the growth is non-linear and exponential.

In 2021 revenue is forecast at $75.3 million, and $281 million in 2022. By 2023 it expects to make $647.7 million in revenue and $1.377 billion in 2024. The latter two forecasts are important for its valuation, as we will see later.

By contrast, Hyliion expects to have $1 million in revenue in 2020 and $8 million in 2021, according to its June 2020 presentation. However, by 2023 it projects more than $1 billion in revenue, topping $2 billion by 2024. These are much more aggressive estimates than XL Fleet’s, which is already producing significant revenue.

Moreover, XL Fleet’s presentation (p. 11) indicates that by 2020 year-end the cumulative number of units sold will be 4,284 electric and hybrid vehicles. By 2021 it will have sold 9,234 units.

Hyliion will only have 20 units sold in 2020 and 320 by 2021. Even Workhorse will have just 10% of XL Fleet’s cumulative units sold by 2020 year-end, at 400. By 2021 it will have 2,400 units sold or 26% of XL Fleet’s cumulative number.

The bottom line is that XL Fleet is a more accomplished and substantive company.

Estimated Value for PIC Stock / XL Fleet

As usual with most SPAC merger presentations, the documents present management’s estimate of the company’s valuation. I find this useful, as most IPO prospectus documents don’t do a good job of forecasting value for investors.

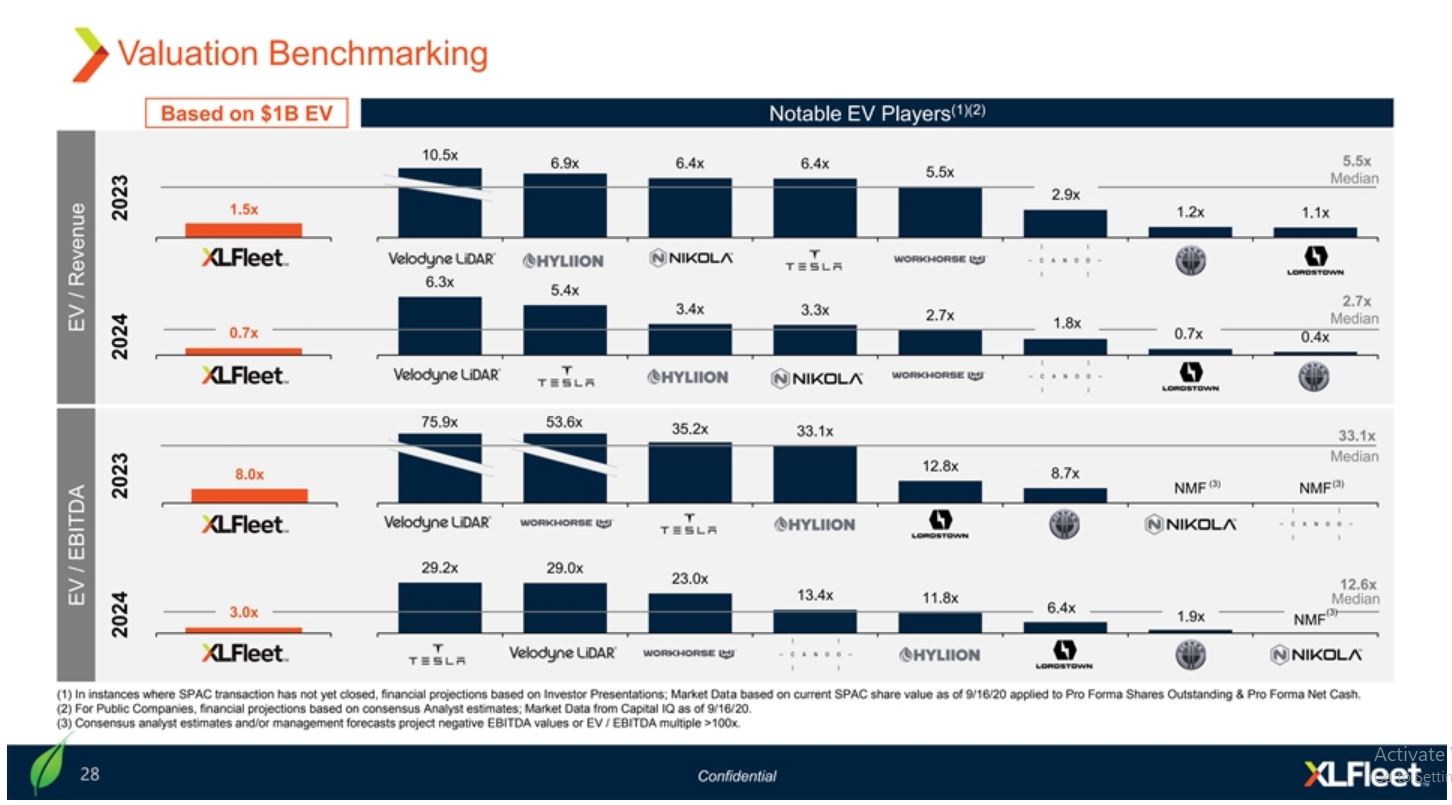

For example, on pages 27 (right) and 28 (below) of the slide presentation, XL Fleet presents its present value and its comparative value vs. its peers.

Click to Enlarge

At a recent price of $10.33 per share, PIC stock has a pro forma market value of $1.485 billion. XL Fleet will have $350 million in cash on the balance sheet (post-merger) with no debt. Therefore the pro forma enterprise value (EV) will be $1.135 billion.

By contrast, Hyliion, which recently completed its merger on Oct. 16 and closed at $21.27 on Oct. 27. It now has a market capitalization of $3.273 billion on 161.16 million shares. Even though it has much less unit production than XL Fleet, its market value is 2.4 times PIC stock / XL Fleet’s $1.485 billion market value

Moreover, XL Fleet expects to make $1.377 billion in revenue by 2024. That puts it on an EV-to-revenue market ratio of 0.82x management’s 2024 forecast revenue. Divide its $1.135 billion pro forma enterprise value by the 2024 forecast revenue of $1.377 billion.

By contrast, Hyliion’s revenue forecast revenue of $2.09 billion is probably too high. Its 2024 EV-to-revenue ratio is still higher than XL Fleet’s, at 1.45x. (Take its $3.56 billion market value, subtract $520 million in cash, and divide that number by $2.09 billion in revenue).

Bottom Line on PIC Stock

The rest of page 28 (right) of the presentation compares other companies with XL Fleet, but the conclusions are similar. The bottom line is that XL Fleet is worth at least 240% more than its present price, which obviously bodes well for PIC stock investors.

Click to Enlarge

This is especially true in a comparison with Hyliion, which has lower expected production than XL Fleet, but its market value is over 240% higher than the pro forma market value for PIC stock /XL Fleet.

Hedge funds and other professional investors will likely take advantage of this discrepancy. It is likely a very good arbitrage opportunity. Astute investors will look to make money from PIC stock’s undervalued situation.

On the date of publication, Mark R. Hake did not have (either directly or indirectly) any positions in any of the securities mentioned in this article.

Mark Hake runs the Total Yield Value Guide which you can review here.