European charging company EVBox is moving forward with its merger with SPAC (special purpose acquisition company) company TPG Pace Beneficial (NYSE:TPGY). The deal was announced on Dec. 10, but no date has yet been set for its closing. Nevertheless, my analysis shows that TPGY stock (to be changed to EVB stock after the merger) is at least 147% undervalued.

This might seem aggressive, especially since it has fallen over 31% year-to-date and 30% since Feb. 18 when I last wrote about TPGY stock. Since then the company has resubmitted a new slide deck presentation.

I compared that with the prior one and found there were only minor differences. The bottom line is that I estimate that TPGY stock (EVB) is worth $44.61 per share. This is 147% above the Friday closing price of $18.10 per share. Here is how I came up with this.

TPGY / EVB Valuation

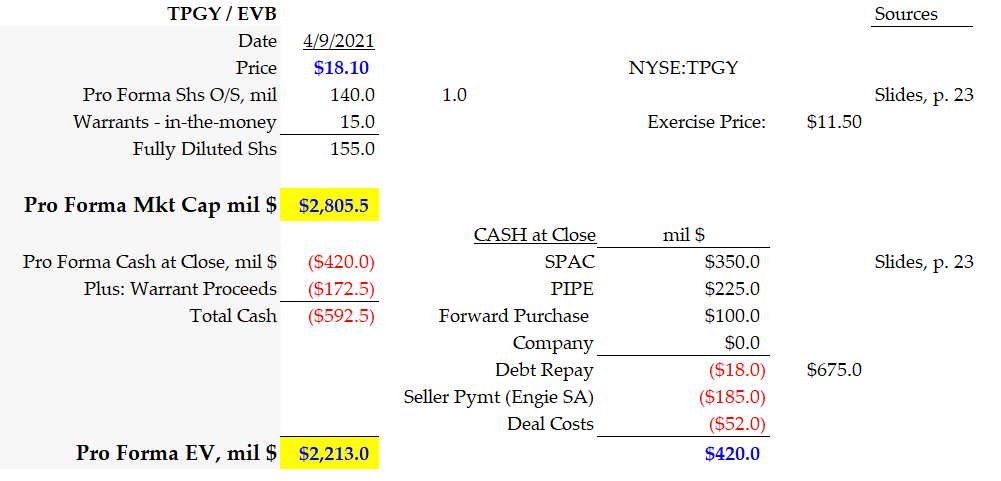

Using the same method as in my last article, we can see that the pro forma market value for TPGY stock is $2.8 billion at today’s price. The enterprise value (EV), after deducting the cash provided to EVBox at the closing ($420 million), was $2.213 billion.

Click to Enlarge

This also includes $172.5 million from exercised warrants which will happen within a month or two after the close. You can see these calculations in the table above on the right.

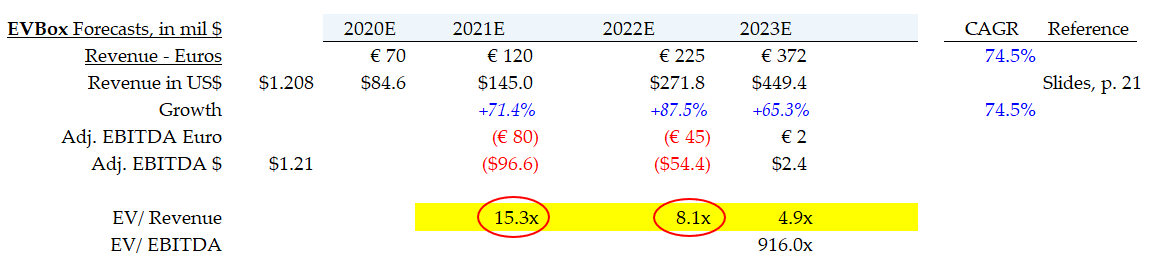

We can use this to determine the value metrics for the company. For example, EVBox kept its forecasts for 2021 and 2022 revenue stable at $145 million and $272 million respectively (in Euros).

Click to Enlarge

You can see in the table on the right that TPGY stock trades at just 15 times 2021 revenue and 8 times 2022 using Enterprise Value (EV).

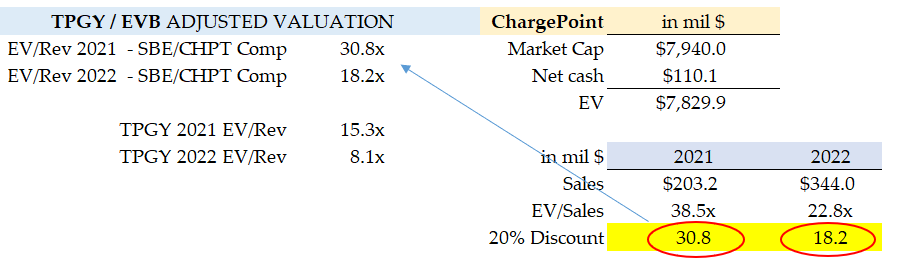

But this is too cheap, especially when compared with ChargePoint Holdings

(NYSE:CHPT). For example, you can see in the table below that TPGY stock trades at half the value of CHPT stock.

Click to Enlarge

For example, CHPT stock trades at 38.5 times 2021 revenue and 22.8 times 2022 revenue. However, I took a 20% discount to be conservative, and since EVBox will have to increase its operations in the U.S. Even at 30 times 2021 revenue and 18 times 2022 revenue, these metrics are twice those of EVBox.

What TPGY Stock Is Worth

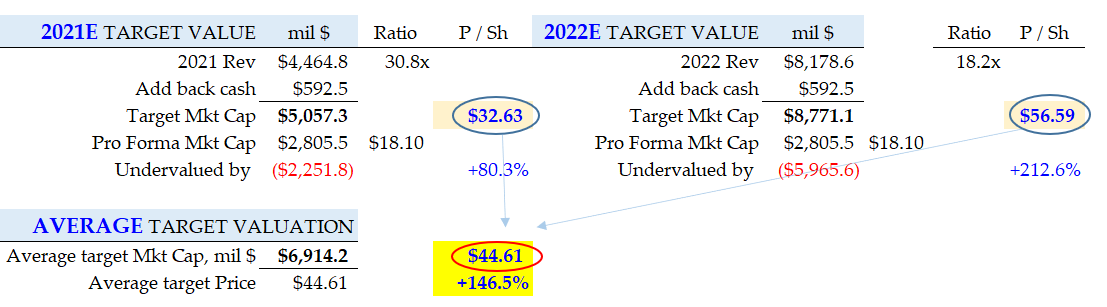

We can now apply these ratios to the estimates for EVBox using their own forecasts that the company gives for 2021 and 2022. TPGY stock is worth between $32.63 (2021 forecast using a 30.8 multiple) and $56.59 (using an 18.2 multiple for 2022).

Click to Enlarge

You can see these calculations in the table on the right. It shows that the average price target after applying these multiples is $44.61, or 146.5% above today’s price.

In other words, EVB is worth well over double its present price, when compared to ChargePoint. Both are major charging station companies. They should have similar valuations.

In fact, even if discounted the CHPT stock 2021 multiple by 50%, or 19.25 times, this is still 26% above TPGY’s present multiple of 15.3 times. This shows you just how deeply undervalued EVBox presently is, prior to its SPAC deal closing.

My price target for EVBox at $44.61 is slightly lower than my prior target in Feb. of $49.32. However, since then ChargePoint has closed its SPAC merger deal. However, CHPT stock has not fallen like TPGY stock. It seems that the latter has really been overly punished by the market.

I suspect that once the deal closes, EVB stock (the new symbol) will move back up closer in line with the valuation of ChargePoint. That suggests that TPGY is likely to move up well over twice its present price to $44.61 per share. Astute investors will take advantage of its present depressed price to earn this high ROI.

On the date of publication, Mark R. Hake did not hold a long or short position in any of the securities in this article.

Mark Hake writes about personal finance on mrhake.medium.com and runs the Total Yield Value Guide which you can review here.