Peloton Interactive (NASDAQ:PTON) stock plummeted by over 32% in after-hours trading on Nov. 4 following weaker revenue growth and a wider earnings miss in a quarterly report released after markets closed.

PTON’s latest quarterly earnings shook stock investors’ confidence in the company’s ability to ever turn profitable. And honestly, now may be the time to take a breather in Peloton.

Let’s look at the pros and cons in Peloton.

PTON Disappoints on Both Top and Bottom Lines

Peloton Interactive’s quarterly revenue of $805.2 million showed a 6% year-over-year growth and exceeded the company’s prior guidance for $800 million. However, PTON stock investors expected $808.9 million revenue, or a 6.7% annual growth.

The topline miss appears narrow but still confirms that the triple-digit growth rates seen during the pandemic could be a thing of the past. Perhaps indoor fitness is no longer a hot sell as masses embrace their freedom from home confinement post-Covid-19. Gyms are back on the fitness enthusiast’s menu.

Most noteworthy, Peloton’s quarterly GAAP earnings per share (EPS) loss of $1.25 compared poorly against a market consensus for a $1.05 loss. That was too wide an earnings miss, one could say.

Reading deeper into the company’s latest earnings results, there’s a lot for PTON stock investors to concern themselves with going forward.

Weak Margins, Ballooning Operating Expenses Weigh on PTON stock

Peloton Interactive’s gross margins are going down, and they could remain depressed for much longer.

Gross profit margins for the September quarter at 32.6% represented a 20% year-over-year decline. The reading was weaker than the company’s own guidance of 33%, which was given in August.

The company’s guidance for the next quarter (ending in December) is for $1.1-1.2 billion revenue with gross margins declining further to 24%.

Interestingly, management hopes that a growing subscriber base could help lift total margins back to 32% for the year. Subscription revenue carries strong, up 94% year-over-year. However, the picture remains gloomy still.

Peloton’s Fiscal Year 2022 Guidance

| Prior Guidance | Updated Guidance |

| 3.63 million ending Connected Fitness Subscribers | 3.35 million ending Connected Fitness Subscribers |

| $5.4 billion total revenue | $4.4 billion – 4.8 billion total revenue |

| Gross profit margin of approximately 34% | Gross profit margin of approximately 32% |

| $325 million adjusted EBITDA loss (6% of revenue) | $425 million – 475 million adjusted EBITDA loss (nearly 10% of sales) |

Management at PTON revised its revenue guidance for the fiscal year 2022 downwards, seeing slower growth in subscriber base, weaker margins and deeper losses.

The Ugly Side to PTON’s Aggressive Pricing Strategy

PTON’s new growth strategy attempts to lure new customers through price discounts and longer 39-month credit terms. Unfortunately, the result is still slow growth, weaker margins, a sudden drop in operating cash flows and worse losses.

To support its aggressive price reductions, the company increased its marketing and advertising expenditures and invested heavily in inventory. Operating expenses grew by 140% year-over-year (to constitute over 77% of total revenue) for the quarter.

One could justify ballooning expenses by pointing to an increase in employee headcount, growing research and development (R&D) spending and the impact of the new subsidiary Precor’s cost structure.

However, this is nothing new. The company’s ugly history of severe operating losses remains intact.

Can PTON Arrest Operating Expenses Growth for Stock Investors’ Comfort?

Peloton Interactive failed to break even when it experienced an unexpected demand surge during the pandemic. Without a pandemic catalyst, the rapid uptake of its bikes, treads and app membership growth throughout 2020 and into the first half of the calendar year 2021 could have taken the company many years to achieve.

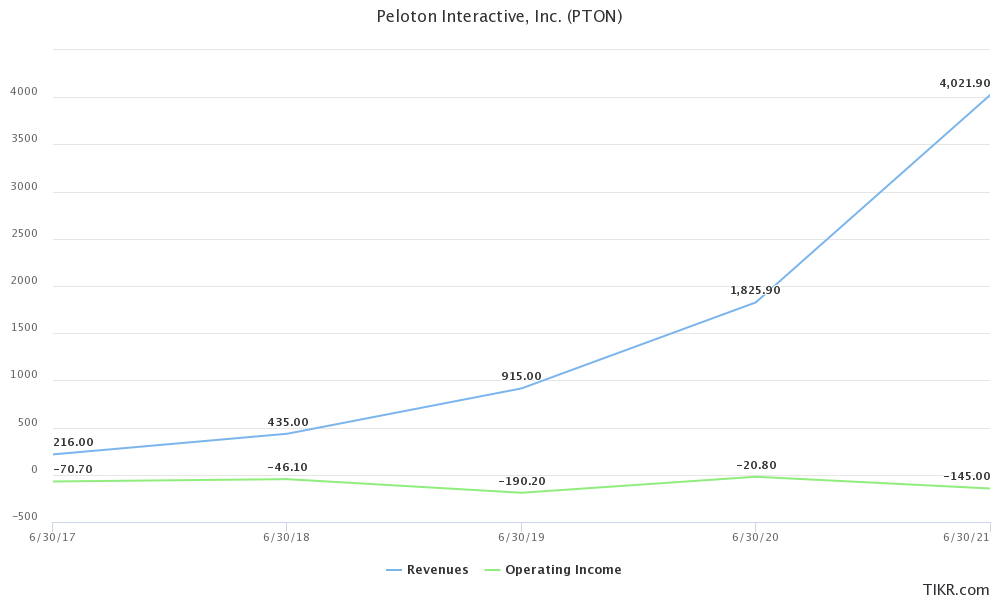

But revenue growth was still accompanied by wider losses.

<em>PTON’s strong revenue growth left operating earnings behind. Chart courtesy of <a href="https://tikr.com/">TIKR.com</a> </em>

Peloton’s revenue grew faster over the past five years, but operating earnings weren’t responsive at all. Revenue growth left operating earnings behind by a wide margin.

The company is making more operating losses as revenue grows. This leads PTON stock investors to question the business model. Perhaps Peloton’s operating model and cost structure aren’t conducive to profitability.

Pressure is mounting on Peloton’s management to look deeper into the business’ operating model as a matter of agency. Recent evidence has shown that scaling up alone won’t deliver desired profitability.

And management knows it. Here’s how the company puts it:

“In conjunction with our revised demand forecasts, we will be taking concrete steps to re-examine our expense base and adjust our operating costs to better align our investments with our revised growth expectations.”

Buy the Dip or Bail Out on Peloton Stock?

Peloton stock may still have a place in a long-term-growth-oriented growth portfolio given its sustained double-digit growth rates in subscribers. Gross margins expand as subscriptions rise to form a significant component of total revenue. Right now, margins remain under pressure as price cuts drop hardware sales margins to around 7%.

PTON stock may still rally again once the market has better visibility on the cost management front. More so if subscriptions maintain current strong growth run rates. However, it’s still a catch-22 situation since high subscriptions growth also requires sustained high marketing budgets and price inducements. The company could find it hard to maintain subscriptions growth and contain operating costs at the same time.

Most noteworthy, considering the high operating cash burn during the past quarter which could persist as the company finances its customers through lengthy credit terms, Peloton could be in the market looking for a new cash injection soon as its capital gets tied up in customer accounts.

Beware of the potential upcoming dilution which could cause further weakness on Peloton stock!

Watching PTON stock from a distance could probably be a stress-reducing exercise right now.

On the date of publication, Brian Paradza did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Brian Paradza is an investing enthusiast who was awarded the CFA Charter in 2019. A strong believer in fundamentals-based long-term investing, Brian learns from gurus like Warren Buffett but acknowledges human behavioral tendencies that drive short-term “madness”. You may find him inquisitive as he examines tech investing opportunities, cannabis, blockchains and the new cryptocurrencies asset class.