Big talk on curbing inflation … what happened the last time the Fed was in this situation … weighing the pros and cons of different approaches

Before we begin today’s Digest, a quick note…

Our InvestorPlace offices and Customer Service Department will be closed this Monday, 1/17 in honor of Dr. Martin Luther King Jr.

If you need assistance, we’ll be happy to help when we re-open on Tuesday.

***Yesterday, Federal Reserve Governor Lael Brainard spoke before the Senate Banking Committee

From her testimony:

Inflation is too high, and working people around the country are concerned about how far their paychecks will go.

Our monetary policy is focused on getting inflation back down to 2 per cent while sustaining a recovery that includes everyone.

This is our most important task.

This “most important task” now has many thinking we’ll see three or four rate hikes this year alone.

As regular Digest readers are aware, we’ve watched a massive sector rotation in stocks as a result of this forecast of rising interest rates. Money has fled the rate-sensitive tech sector in favor of value plays.

But even with Brainard’s comments, there can be a stark difference between big-talk projections and what will actually happen.

And if we use past as a guide, the Fed may be more talk than action.

***The last time the Fed attempted to both shrink its balance sheet and hike rates led to huge volatility in the market

Here’s Josh Brown from The Reformed Broker, reminding investors of what happened in this situation back in 2018:

It was a disaster…

Two separate major corrections occurred that year, culminating with a nasty 20% crash into Christmas Eve which finally forced the Fed to say “Okay, just kidding. Not only are we not raising rates anymore, actually, the next few moves will be cuts. Merry Christmas, we’re sorry.”

I’m paraphrasing, but that’s literally what happened.

The Fed had gotten up to 2.5% Fed Funds and both the stock and bond market called “Bullshit!” on them – meaning, the economic growth story was no longer being bought.

By Q3 2019 the yield curve had inverted and in 2020 we were maybe on track for a recession, with or without Covid.

***So, are there similarities between today and 2018?

And speaking of the yield curve, what’s its shape right now, and what is that telling us?

The “Bond King,” Jeffrey Gundlach of Doubleline sounded off on this earlier in the week.

From MarketWatch:

Today [Tuesday] sounds like Jay Powell repeating the 2018 formula: end QE and raise official short-term interest rates,” Gundlach said in a webcast to clients that was live tweeted late Tuesday.

He said that he’s not “predicting a recession yet” but sees those pressures building.

He said the yield curve had seen “pretty powerful flattening” and was “approaching the point where it signals economic weakening.

At this stage, the yield curve is no longer sending a don’t-worry-be-happy signal, says Gundlach. It is instead signaling investors to pay attention, he said.

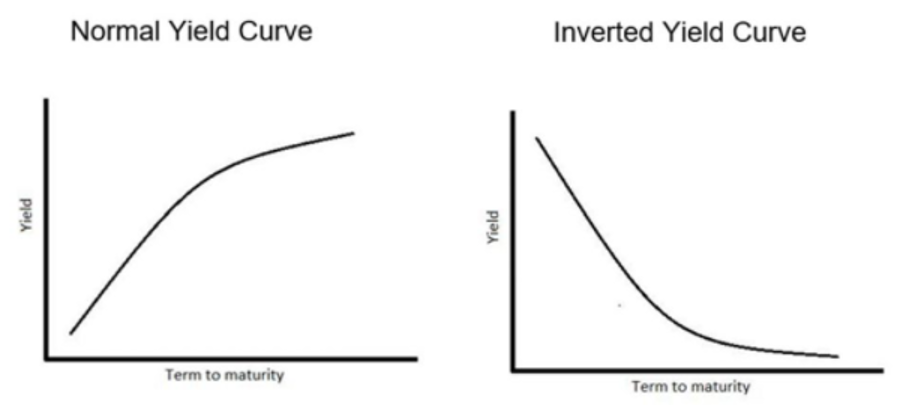

To make sure we’re all on the same page, a yield curve is a graphical representation of the yields of all currently available bonds – from short-term to long-term

In normal times, the longer you tie up your money in a bond, the higher the yield you would demand for it. So, you’d expect less yield from a two-year bond and more yield from a 10-year bond.

Given this, in healthy market conditions, we usually see a “lower-left” to “upper-right” yield curve.

But when economic conditions become murky and investors aren’t sure what’s on the way, this can change. Specifically, uncertain economic times tends to flatten the yield curve.

And if the yield curve actually inverts, history has shown that it serves as a highly-accurate predictor of recessions, though the timing of those recessions is varied.

From Reuters:

Yield curve inversion is a classic signal of a looming recession.

The U.S. curve has inverted before each recession in the past 50 years. It offered a false signal just once in that time.

***So, with 2018 as our guide, the markets will not react well to “too much, too fast,” especially in light of today’s flattening yield curve

With all this in mind, let’s jump back to Josh Brown:

And now, four years later, there are people who want to tell you that the Fed is anxious to repeat this experiment?

Lift-off in rates while simultaneously shrinking its balance sheet and tightening financial conditions, upending stocks and bonds while it seeks to normalize policy.

With Omicron running circles around the CDC and local governments?

Yeah, okay. That’s a dumb f***ing bet. Powell is smart.

If you got spooked by the Fed Minutes (last) week, where one or two members were sort of maybe discussing the possibility of run off, it’s understandable. A lot of very serious, very (self-) important people were doing TV hits actually taking this scenario seriously.

Don’t.

…they’re not looking to go so fast as to repeat the mistakes of 2018.

Why would they? Where is the gun to their heads?

It’s an interesting point.

***From the Fed’s perspective, you generally have two not-great options on the table in front of you

Option A, you repeat 2018’s formula of letting assets run off the balance sheet while hiking rates. Of course, as today’s Digest has highlighted, Powell is very aware of how the market responded the last time he did this.

It wasn’t pretty, and Powell was dragged through the mud in the financial press.

Option B, Powell moves slower. Not so aggressive with the bond portfolio. And perhaps instead of four rates hikes this year, there’s three. Maybe two.

The risk here is that inflation lingers. But who knows? Perhaps that’s offset as supply chains get back to normal. Maybe it ends up being the best of both worlds.

And perhaps moving slower is given cover by underwhelming economic data.

For example, what happens if Omicron or a new variant causes more lockdowns? Or what if it complicates supply chain problems? What if the employment trend worsens? What if trade issues with China flare up?

There are any number of potential variables that Powell could point toward as valid reason to slow things down on tightening.

Now, let’s say he does. Under this Option B, who suffers most of the collateral damage?

Well, primarily lower income and fixed income individuals who are more sensitive to inflation than wealthier Americans who have assets that climb in value alongside with inflation.

Now, I might be cynical, but the following tradeoff has likely crossed Powell’s mind…

In one corner we have the risk of deep-pocketed, powerful investors who are furious over an imploding stock market, calling for Powell’s head because he moved too fast.

In the other corner, there’s the risk of lower-income Americans losing some of their purchasing power to lingering inflation, though Powell can point toward an assortment of reasons why a more cautious approach was warranted.

If I was a betting man, I would wager that if Powell is going to misstep, look for him to favor inflation over heightened market turbulence.

***So, what does this mean, bottom-line?

It clears the path for the market to continue climbing in the coming months.

Yes, expect volatility. There is still uncertainty and the market hates uncertainty.

Plus, we’re just entering earnings season and it’s unclear how beats or misses will impact broad investor sentiment.

But looking further out over 2022, as Wall Street comes to the realization that Powell might not be in quite the hurry that many fear, it could serve as a pressure release, helping support a broad move higher.

In any case, it will be fascinating to watch. We’ll keep you updated here in the Digest.

Have a good evening,

Jeff Remsburg