- SoFi Technologies’ (SOFI) fintech angle appears a no-brainer as a long-term concept.

- However, the housing boom is not what you think it is.

- You must separate what you want out of SOFI stock versus what it is.

Among a growing number of financial technology (fintech) firms, SoFi Technologies (NASDAQ:SOFI) initially garnered attention for facilitating broader access to capital but what if a key bullish thesis was instead a myth? Though mainstream headlines will scream that such a notion is ludicrous, the math says otherwise, which is incredibly problematic for SOFI stock.

To be clear, I’m not suggesting that SoFi’s underlying business model is fundamentally flawed. Given the rise of the blockchain and the decentralization of financial transactions and even outright ecosystems, it’s clear that digitalization in money-related endeavors is the future. You’re not going to put that genie back in the bottle, which in the long run could be beneficial for SOFI stock.

However, enthusiasm toward a publicly traded security eventually must tie in with a substantive narrative. Moreover, this narrative must itself be tied to a reasonably viable framework. For many folks, that tie-in is the robust housing market. With prices soaring to the moon — in part contributed by historically low interest rates — SOFI stock was (and arguably still is) a beneficiary.

Fair enough. But what if the housing boom isn’t what you think it is? What if there really is no shortage of housing?

| SOFI | SoFi Technologies | $9.77 |

Early Enthusiasm of SOFI Stock Based on a Myth

No housing shortage? Are you crazy? A litany of experts from mainstream media sources will contradict such a nation every which way till Sunday. In fact, NPR just recently released an article entitled, “There’s never been such a severe shortage of homes in the U.S. Here’s why.”

At the risk of writing yet another whopper — of which I have many, too many perhaps — I just don’t find the mathematical justification for this housing shortage concept. According to the data, it’s not “fake news” but it’s not totally accurate.

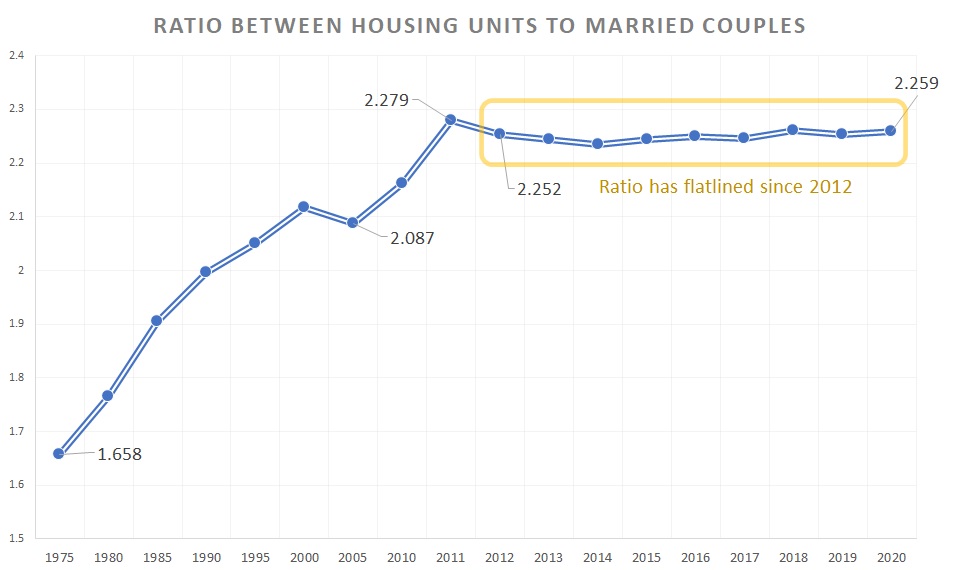

Let’s get into it. According to data compiled by Statista — which likely came from government sources like the U.S. Census Bureau — the number of total housing units measured 140.8 million in 2020. On the other hand, the number of married couples — the key demographic of prospective homebuyers — in that year was 61.45 million.

Click to Enlarge

On average, this translates to 2.26 housing units per each married couple. In fact, this number hasn’t fluctuated much since the Great Recession. At the post-recession peak, there were 2.28 housing units per couple in 2011. A year earlier, the ratio was 2.16.

Put another way, this consistent assertion that housing shortages are crippling homebuyers isn’t supported by the data. Since 1990, there have always been at least two housing units available per married couple. Therefore, plenty of housing exists — the ratio of the likeliest homebuyers versus total housing units has contextually stabilized.

Does that mean homebuyers aren’t getting blasted? Of course not! The Covid-19 pandemic eliminated available inventory in the market and soaring consumer inflation performed a blitzkrieg on homeownership aspirations.

But a housing shortage? The data doesn’t support that idea and thus I would be cautious about buying SOFI stock on the thesis that housing prices will continue moving higher.

But Why Does the Housing Shortage Crisis Myth Persist?

Although the data might sound initially convincing, the question becomes why does the housing shortage argument persist? After all, experts always say that housing units are short a few million. Compounding the problem, homebuilders are simply not building enough of them.

While I can’t address every report, what I can say is that when discussing housing market dynamics, you must be selective in your data. For instance, you can’t say there’s a shortage of cars in America because we have 330 million people — and that’s a lot.

Well, not every one of those 330 million are of legal driving age. Further, not everyone can legally drive. In order to make a shortage argument, you must narrow your population data to relevant subsegments; hence, married couples in the U.S.

But even if you just took adults in the U.S., the housing shortage argument doesn’t become any stronger. In 2020, there were 258.3 million adults, meaning that each adult had access to 0.545 housing unit. While that sounds like a shortage, in 1980, there were roughly 176 million adults per 87.74 housing units, translating to a 0.50 housing-unit-to-adults ratio.

Granted, in 2010, this ratio boomed to 0.557 but it wasn’t sustainable. Why? Just like the relationship between cars and people, not everyone can (or should) drive. When you whittle down housing data to the folks that can and should be buying homes, the fundamentals haven’t changed as much as some would have you believe.

Not an Attack on SOFI Stock

Before I get inundated with angry messages, please oh please keep this in mind. I am not attacking SOFI stock. The business of bringing more access to financial and investment instruments to regular folks is a noble one.

However, the business also has to make sense for SOFI stock and therein lies the rub. As my InvestorPlace colleague Chris Lau pointed out, “the Biden administration quietly extended the federal student loan payment moratorium.” As Lau bluntly stated: “Students have no incentive to pay back their loans.”

Exactly. And no matter how you feel about SOFI stock, losing a revenue source like that will hurt. What I’m saying is to watch out about this housing boom argument. Housing experts say that shifting supply demand conditions have created an extraordinarily bullish opportunity. Likely, this is a distortion of the facts.

On a per-capita basis of credible prospective homebuyers relative to housing units, the fundamentals have not materially changed. Let me repeat, the fundamentals have not changed.

What did change? Covid-19 disrupted the housing market but that will eventually fade out. In my view, the biggest impact is that the Federal Reserve unilaterally diluting consumer’s purchasing power. That’s why many cannot afford a homes.

And SOFI stock will also suffer along with everybody else.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.