How aggressive will the Fed be now? … how gasoline saved the CPI … why oil’s disinflationary tailwinds might be dropping … a look at where inflation could go

To the casual market observer, Wednesday’s CPI report doesn’t make much sense.

Yes, the CPI came in barely higher than estimates, but it was down. Better still, it was down for the second straight month. So, why did the bottom fall out of the market?

Here are our technical experts John Jagerson and Wade Hansen of Strategic Trader to explain:

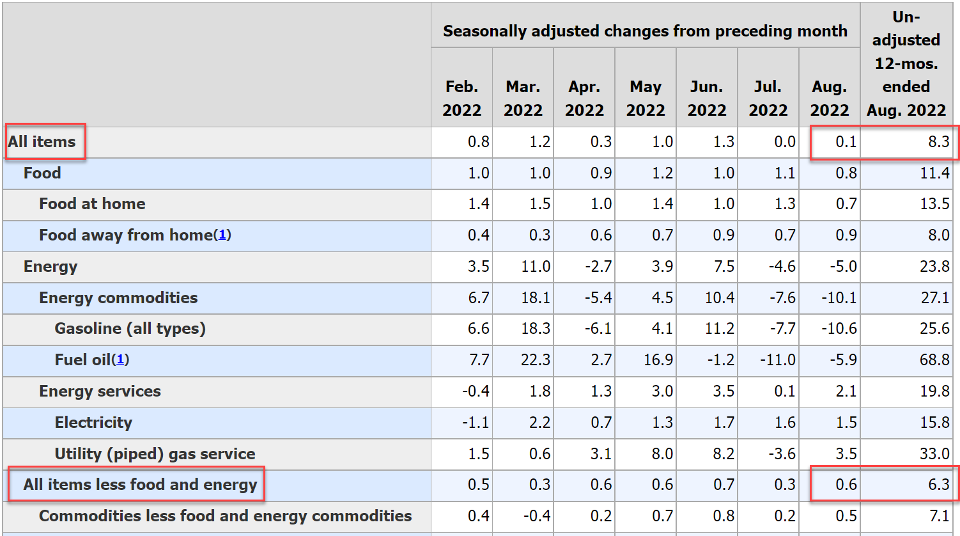

The headline inflation number was actually quite reasonable; it showed that inflation for all items had only increased by 0.1% during August – bringing the annualized rate to 8.3%.Falling gasoline prices helped keep this number lower.The surprising news came with the core inflation number (all items excluding food and energy). It showed that prices for items other than gasoline and food had risen by 0.6% during August – bringing the annualized rate to 6.3% (see Fig. 1).

Fig. 1 – Consumer Price Index Data (Source: Bureau of Labor Statistics)Wall Street knows the Federal Reserve cares more about the core inflation number than it does about the headline number because the Fed doesn’t think it can have much impact on food and energy prices with its monetary policy.That’s why traders reacted so swiftly to yesterday’s news and started selling stocks.They know higher inflation numbers are going to force the Fed to be more aggressive in their monetary policy response.

The question now is “how aggressive?”

We can get a sense for how Wall Street traders are answering this question by using the CME Group’s FedWatch Tool. This shows us the probabilities that traders are assigning to different fed funds levels at various points in time.One month ago, traders overwhelmingly believed the Fed would raise rates just 50 basis points next week. Specifically, they put 61% odds on it. A 75-basis-point hike carried the remaining 39% probability.Today, there isn’t a single trader out there who expects 50 basis-points. The odds are 0%.Instead, a full 20% of traders think we’ll see a 100-basis-point hike next week.

Now, rather than get too wrapped up in what’s going to happen next, let’s back up and come at this from a different angle.The market is watching the Fed… the Fed is watching the data… the data are largely influenced by inflation… what’s driving inflation right now?Well, here’s the Bureau of Labor Statistics:

Increases in the shelter, food, and medical care indexes were the largest of many contributors to the broad-based monthly all items increase.These increases were mostly offset by a 10.6-percent decline in the gasoline index.

In short, lots of things are driving inflation, but falling gasoline prices saved us.Take a moment to consider what kind of CPI report we would have had – and the ensuing market reaction – if falling oil prices hadn’t come to the rescue.I think it’s safe to say a headline number of 9%+ would have been in the cards.Now, the name of the game in investing is “what happens next?”On that note, we shouldn’t expect easing crude prices to continue picking up the slack for stubbornly high inflation elsewhere – at least not to the same degree they have recently. And that could actually be a de facto inflationary influence on the headline number.Meanwhile, even though the Fed doesn’t watch gasoline prices as much as core inflation, you can be sure they’ll take note if this happens.Let’s dig into this a bit more.

How will restocking the Strategic Oil Preserve impact oil prices?

A contributing factor to why prices at the pump have fallen for 13 straight weeks is because of President Joe Biden’s decision to release oil from the Strategic Petroleum Reserve back in March.Since the beginning of the summer, the Biden administration has released about eight and a half million barrels per day in an effort to take pressure off drivers.The has drained almost 140 million barrels, or about 24%, of the Reserve. Levels are now at their lowest point since 1984.This release is set to end next month. Of course, the Strategic Petroleum Reserve is for emergencies. As such, it needs to be replenished for future emergencies.This is the backdrop for unnamed sources that are saying Biden is looking to begin refilling the Reserve when crude oil prices hit a certain level.Here’s Bloomberg with those details:

The US may begin refilling its emergency oil reserve when crude prices dip below $80 a barrel, according to people familiar with the matter.Biden administration officials are weighing the timing of such a move, with an eye toward protecting US oil-production growth and preventing crude prices from plummeting, said the people, who asked not to be named sharing internal deliberations…Buying crude to refill the reserve, which is now at the lowest level since 1984 after a record drawdown last week, would be supportive for the market.

You’ve heard of the “Fed Put.”

Well, it appears we might have the “Biden oil put” – ironic since Biden’s track record is one of the most “anti-oil” in presidential history.Keep in mind, if Biden does begin to refill the Reserve, it will have a dual impact…It’s not just that he’ll be buying at roughly $80 – the market will also no longer be flooded daily with the release of millions of barrels of oil. So, it’s a double-whammy hit of decreased supply and increased demand.Now, on a consumer level, oil demand is lower in the fall. It will be interesting to see how the push/pull of these influences impacts retail prices.

But this isn’t the only potential “put” that could prevent crude prices from slipping lower

It’s not all over the news, but more than 20% of China’s population is currently under some form of coronavirus-related restrictions.From Nikkei Asia:

As of Sept. 6, lockdowns or other movement restrictions were in place in 49 cities, covering 291.7 million people, according to Nomura International (Hong Kong).Authorities in the northeastern city of Dalian have ordered residents in a major downtown business district to stay home. The restrictions originally were to run from Aug. 30 to Sept. 3. But the city decided on Sept. 10 to extend them again, and the lockdown is now expected to last until around Saturday.

With so much of the nation locked down, the Chinese economy – and by extension, demand for oil – is taking it on the chin. For example, in August, China’s private Caixin manufacturing PMI contracted for the first time in three months.But on Wednesday, we learned that China might be easing some restrictions.From Bloomberg:

The Chinese megacity of Chengdu has allowed most residents to leave their homes from noon Thursday, largely dismantling a two-week lockdown as Covid-19 cases decline…Nationwide, 949 cases were reported Wednesday, the fourth day in a row the number has held below 1,000, having fallen steadily from the most recent peak of 3,424 on Aug. 17.Beijing, which has seen flareups in a number of colleges and a high school in recent days, recorded just two cases, both of whom were already in quarantine.

Now, we don’t know when China will reopen, nor to what degree. But we do know that, in whatever form it takes, it will be supportive of oil prices.

To be clear, neither a refilling of the Strategic Petroleum Reserve nor a tepid economic reopening from China is going to result in $100+ oil

But that’s not the point.In a world where the Nasdaq crashes 5% because a CPI report missed by 0.1%, it’s clear that the tiniest influences on inflation can make a massive difference.So, what happens when oil prices stop falling, which means this part of the month-to-month CPI reading goes from “-10.6” (its latest August reading) to “0”?It doesn’t even have to be “0” by the way – any number less (actually, “more”) than -10.6 will do it.So, what’s the evidence that things are slowing down here?Well, I just looked at some recent average prices for West Texas Intermediate Crude (WTIC).The average price for July was $105.08. In August, it fell to $93.67.That’s a percentage decline of 10.86%.I just calculated the average price of for each weekday here in September. It’s $86.25.That’s a decline from August’s average of just 7.92%.Now, this won’t translate 100% to gas prices, but the point is clear: The rate at which oil prices are dropping is slowing, and that will affect month-to-month CPI readings.Meanwhile, if inflationary pressures in other areas of the economy remain the same, this will end up being an upward pressure on the CPI.This brings to mind a quote we’ve highlighted a couple times here in the Digest from Richard Curtin. He’s the University of Michigan professor who has directed the widely-referenced University of Michigan Consumer Sentiment surveys since 1976.When comparing the inflation of the 1970s with that of today, Curtin concluded:

Another critical characteristic of the earlier inflation era was frequent temporary reversals in inflation, only to be followed by new peaks.That same pattern should be expected in the months ahead.

It will be fascinating to watch how this wonderfully-complex and interrelated financial ecosystem evolves. We’ll keep you updated here in the Digest.Have a good evening,

Jeff Remsburg