If I were a screenwriter, I could not make up the 2024 presidential election scenario.

On the right, we have former president Donald Trump. He was tried for impeachment twice in 2019, was found guilty of several felonies, and is currently facing a slew of other indictments and court cases. And on July 13, he was the victim of an assassination attempt.

And on the left, President Joe Biden was the Democratic nominee… until he stepped aside and endorsed Vice President Kamala Harris. And since Harris did not go through the traditional primary process (running against an opponent), some voters were dismayed at their lack of choice in the matter.

RFK Jr. was running as an independent, and was expected to peel away votes from both candidates. But in a surprising move, on August 23, he announced that he would remove his name from the ballot in key swing states. This effectively ended his candidacy. And in an even bigger surprise, he endorsed Donald Trump.

That means we have two presidential candidates to choose from right now. Neither one is particularly popular, and it’s unlikely either one will receive 50% of the overall vote.

But the reality is that, for investors, it doesn’t matter who wins the election in November.

In this report, let’s explore why that’s true. Plus, I’ll show you the first step you need to take protect your portfolio during this chaotic year, regardless of what happens between now and November…

An Age of Chaos – but Still Good for Stocks

Presidential election years can be chaotic, but they are typically good for the stock market.

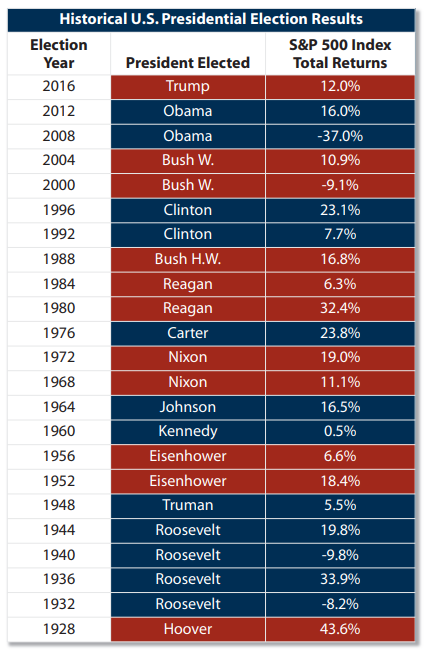

Between 1928 and 2016, there were 23 presidential elections. According to First Trust, in 19 of the 23 election years, the S&P 500 posted positive gains. When a Republican won, the average gain was 15.3%, and when voters selected a Democrat, the average gain was 7.6%. For all presidential election years, the average S&P 500 gain was 11.28%.

You can see the individual market performance during the past 23 elections in the chart below.

Source: First Trust

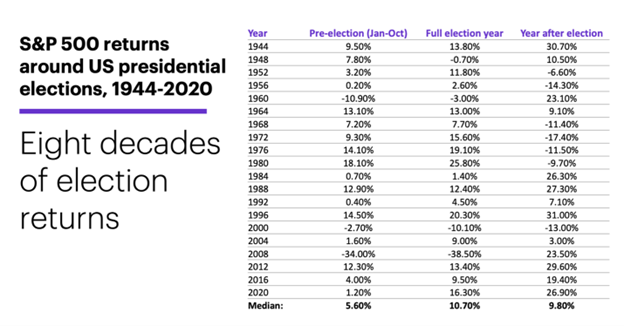

The months leading up to the presidential election are historically good for the stock market, too. For example, between 1944 and 2020 there were 20 presidential elections, and the S&P 500 posted a positive return in 16 of 20. In the 10 months before the election, the S&P 500 gained a median 5.6%. You can see for yourself in the chart below.

Source: E*TRADE

This presidential election year is shaping up to be no different. The S&P 500, Dow and NASDAQ have hit a slew of record closing highs and, at this writing, are up 9.4%, 3% and 9.9% year-to-date, respectively.

The fact of the matter is the stock market traditionally rallies right up to the presidential election because candidates tend to lift both consumer and investor spirits with their endless promises. That’s because they promise the sun, the moon, the stars and the sky to voters in order to get elected.

We get excited.

The good news is the economy is now the No. 1 election issue, followed by border security and foreign wars. The U.S. economy is good for the top 20%, but bad for the bottom 20%. The top 20% tend to own homes and stocks, which are appreciating, while the bottom 20% are struggling with inflation and, frankly, unaffordable homes.

The bottom line: We need to be prepared for some twists and turns in the presidential race this year.

And no matter who comes out on top, we need to be prepared.

So, in order to help you do just that, my staff and I poured through the stocks in my Portfolio Grader database. And we’ve produced a list of five stocks to survive the election chaos.

While a vigorous amount of number-crunching goes on behind the scenes, Portfolio Grader is designed to give you my analysis in easy-to-interpret A to F letter grades.

A=Strong Buy, B=Buy, C=Hold, D=Sell and F=Strong Sell.

As of this writing, my Portfolio Grader rates each of the stocks I’m about to share with you as either “Buys” or “Strong Buys”. That means these stocks not only boast superior fundamentals, but they also have robust institutional buying pressure. So the reality is they should not only survive – but thrive during election season and beyond, regardless of who wins the election in November.

Let’s take a look…

Election Chaos Stock # 1

TransDigm Group

Sector: Aerospace & Defense

Market Cap: $72.6 billion

Portfolio Grader Rating: A

(Market cap and Portfolio Grader rating as of 5/17/2024)

With the ongoing Russia-Ukraine war and escalating tensions in the Middle East, TransDigm Group Incorporated (TDG) should experience an increase in demand for its products.

The company develops and produces components, systems and subsystems for aircraft. The company is a vital equipment supplier to aerospace and defense companies, as its products are used in practically all commercial and military aircraft that are in service today.

TransDigm operates through 48 independent companies, and it operates about 60 manufacturing facilities throughout the United States. The company develops ignition systems, pumps and valves, actuators and controls, AC/DC electric motors and generators, audio systems, cockpit security components, advanced cockpit displays, lighting, seatbelts and much, much more.

Interestingly, TransDigm boosts its revenue in two ways. First, TransDigm’s parts are sold as original aircraft equipment. And then, it generates recurring aftermarket revenue over the life of an aircraft, or for about an average of 30 years.

TransDigm recently increased its outlook for fiscal year 2024. Full-year sales are now forecast to be between $7.68 billion and $7.8 billion, up from previous estimates for $6.59 billion. Adjusted earnings per share are expected to be between $31.75 and $33.09, compared to previous estimates for $25.84. Both outlooks are nicely higher than the consensus estimate, which calls for earnings of $31.86 per share and sales of $7.73 billion.

Let’s face it: The world is a tinderbox. And as tensions escalate, defense budgets are only expected to grow. That should prove to be a nice tailwind for TDG.

Election Chaos Stock # 2

Lockheed Martin

Sector: Aerospace & Defense

Market Cap: $111.3 billion

Portfolio Grader Rating: B

(Market cap and Portfolio Grader rating as of 5/17/2024)

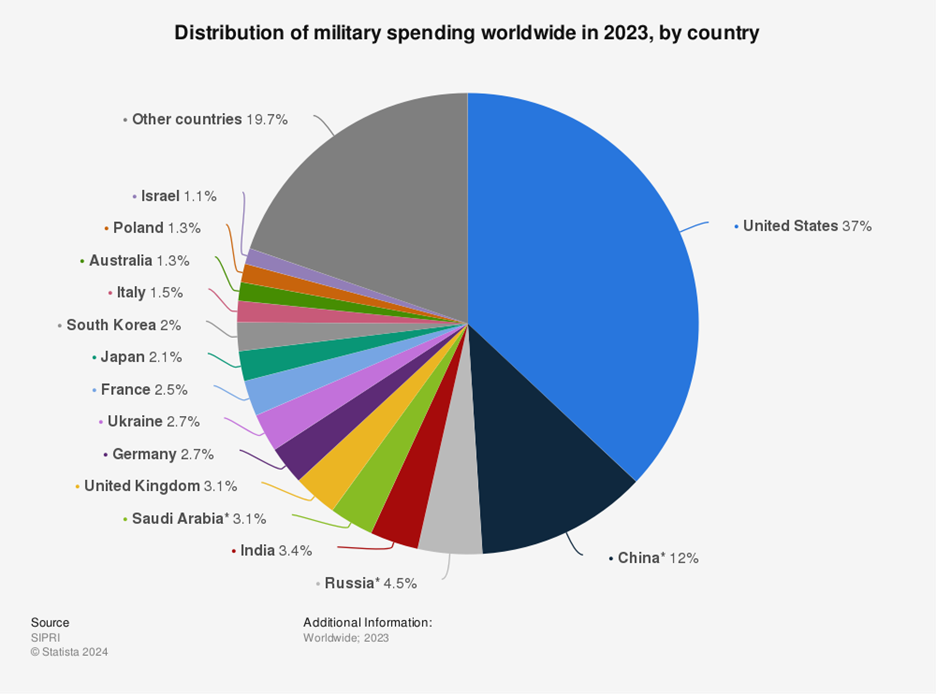

Dwight D. Eisenhower, the victorious Allied commander in World War II and U.S. president during the early years of the Cold War, warned us to beware of the “military-industrial complex.” It seems that no one heeded his warning because the United States spends more on its armed forces every year than the next 10 countries combined… and most of those countries are friendly allies!

Source: Statista

Yet, military spending remains wildly popular with voters… so it shouldn’t be surprising that leading defense contractor Lockheed Martin Corp. (LMT) has crushed the S&P 500 over the long term, with LMT up roughly 275% as of this writing – compared with the S&P’s 178%.

That’s not too shabby at all.

Interestingly, it’s also a winner every presidential election cycle. In every presidential year since 1980 – that’s 11 elections and counting – Lockheed Martin has been a positive trade between May 21 and August 14. In that roughly three-month window, Lockheed has averaged 11.35%, which translates to an annualized 48.74%.

Looking forward, Lockheed Martin expects full-year 2024 earnings per share between $25.65 and $26.35 and revenue between $68.5 billion and $70.0 billion. The outlook is nicely higher than analysts’ current estimates for earnings of $24.42 per share and revenue of $65.21 billion.

The argument for this one is simple. The one thing we know is that military spending always rises – and it should do so for the foreseeable future, regardless of which party is in power.

Election Chaos Stock # 3

NVIDIA

Sector: Semiconductors

Market Cap: $2.3 trillion

Portfolio Grader Rating: A

(Market cap and Portfolio Grader rating as of 5/17/2024)

In case you’ve been living under a rock, NVIDIA Corporation (NVDA) is a major player in the computer hardware arena. It is a leading computer graphics company, making graphic processing units (GPUs) for consumers and businesses. It has over 7,000 patents relating to computer graphics, the largest portfolio of its kind.

The company has been in the computer graphics business for more than two decades – it invented the GPU in 1999 – so it is a well-established player. Since 2014, the company has shifted its focus to five major markets – gaming, professional visualization, data centers, self-driving cars… and, as we all know by now, artificial intelligence.

Not content to rest on its laurels, NVIDIA is already making another huge shift. For decades, it has focused solely on microchips. But more recently, data centers have quietly become a larger and larger share of its revenue. For example, in the company’s fourth quarter, data center revenue hit $18.4 billion – a new quarterly record.

I should also add that NVIDIA CEO Jensen Huang doesn’t even consider them as AI data centers. He calls these hyperscale data centers “AI Factories.”

The hyperscale data center industry is worth nearly $50 billion a year, and it’s expected to grow 20% year-over-year for the next decade.

Huang expects $1 trillion to be spent on these AI data centers, with Amazon, Alphabet, Microsoft and Meta accounting for almost all of that spending.

For the first quarter in fiscal year 2025, the company expects revenue of about $24.0 billion, which represents 268% year-over-year revenue growth. Clearly, NVIDIA will be just fine no matter who is in the Oval Office in 2025. Over at my paid service Growth Investor, we’ve owned NVDA since May 2019. And during that time, we’re up by more than 2,000%.

It’s one of my top picks for growth-minded investors, and I think the best may still be yet to come.

Election Chaos Stock # 4

Novo Nordisk

Sector: Biotechnology

Market Cap: $586 billion

Portfolio Grader Rating: B

(Market cap and Portfolio Grader rating as of 5/17/2024)

This year, Novo Nordisk A/S (NVO) will celebrate 100 years of developing treatments to combat diabetes, obesity and other chronic illnesses, as well as rare blood and rare endocrine diseases.

With headquarters in Copenhagen, the biotech company long has dominated the diabetes treatment market. Its long-term goal is to develop a cure for Type 1 diabetes and help prevent Type 2 diabetes and obesity.

Novo Nordisk offers a variety of insulin pens for folks to administer their diabetes medication, as well as provides injection needles and growth hormone pens. The company has also developed several medications for the treatment of obesity, diabetes, hemophilia and growth disorders, as well as hormone replacement therapies.

You’ve likely seen commercials for one of Novo Nordisk’s diabetes treatments, Ozempic. The company has experienced runaway demand for the drug as well as its recently approved weight-loss drug, Wegovy.

Despite supply constraints, Novo continues to ship more and more doses of these popular treatments – which is fueling rapid sales and earnings growth as a result.

During the first quarter, Wegovy sales more than doubled to $1.35 billion. In U.S. dollars, Novo Nordisk achieved earnings of $3.7 billion, or $0.83 per share, and revenue of $9.52 billion in the first quarter.

Thanks to this ongoing demand for its obesity and diabetes treatments, Novo Nordisk recently increased its outlook for fiscal year 2024. The company now expects full-year sales growth between 19% and 27%, up from previous forecasts for 18% to 26%.

The reality is that demand for these treatments is only beginning. The evidence is mounting that these drugs do much more than help people shed unwanted pounds. The company recently revealed that, in what was the longest study conducted for Wegovy so far, the majority of weight lost thanks to Wegovy stayed off. Specifically, folks who took Wegovy maintained an average 10% weight loss after four years on the drug.

Novo Nordisk is hopeful that the new, long-term data could convince more health insurance companies and global governments to cover or reimburse the costs for Wegovy. In fact, JP Morgan Research forecasts the diabetes and weight-loss drug market will exceed $100 billion by 2030. That makes Novo Nordisk a screaming long-term buy.

Election Chaos Stock # 5

CrowdStrike

Sector: Software-Infrastructure

Market Cap: $83.2 billion

Portfolio Grader Rating: A

(Market cap and Portfolio Grader rating as of 5/17/2024)

CrowdStrike Holdings, Inc. (CRWD) is on a mission to thwart cyberattacks and data breaches on and off businesses’ networks.

The company offers real-time endpoint security, threat intelligence and cloud workload protection. Through its CrowdStrike Falcon platform, it provides 16 modules for next-generation antivirus protection, firewall management, malware search engine and analysis, threat intelligence and threat hunting.

With more folks working remotely and businesses relying on the cloud to connect their employees and make their data/resources available, CrowdStrike’s software is more important than ever. So, it’s not too surprising that it’s seen a surge in customers recently.

For its fiscal year 2024 (which ended in January 2024), CrowdStrike achieved earnings of $751.8 million, or $3.09 per share, and total revenue of $3.06 billion. That represents 104% annual earnings growth and 36% annual revenue growth. These results also beat expectations for full-year earnings of $2.95 per share and revenue of $3.05 billion.

CrowdStrike also provided a positive outlook for fiscal year 2025. The company expects full-year 2025 revenue between $3.925 billion and $3.989 billion and earnings per share between $3.77 and $3.97.

Because we rely so heavily on the internet, we are increasingly vulnerable to cyberattacks. In fact, more than 2,200 cyberattacks occur each day, which equates to about one attack every 39 seconds, according to Security Magazine.

It’s no surprise that cybercrime is an expensive business. In 2018, it cost $1.5 trillion for businesses to protect themselves against attacks. By next year, that number is expected to hit a stunning $10.5 trillion, according to Cybersecurity Ventures.

So, do yourself a favor. First, you should probably change your passwords – just in case. Then, instead of panicking, why not profit from this tailwind?

The unfortunate reality is that no matter who wins in November, one thing is for sure… cybercrime will continue to be a problem that grows with every passing year. That’s great news for a company like CRWD.

Summing Up

Let’s not sugar coat it. It seems like the world is growing increasingly volatile.

Inflation is high. Energy prices are soaring. A global food crisis could be in the cards. The situation with Russia could get way worse. The situation between Israel and Hamas could deteriorate even further. We’re seeing the early stages of “deglobalization.”

That’s just to name a few. Throw in the 2024 election, and we’re looking at a powder keg that could usher in a new age of volatility in financial markets – an Age of Chaos.

But each of the picks we’ve discussed today is profiting from strong catalysts that should hold up during the storm. Heck, some of them are even profiting from it. So, with these picks in your portfolio, you can rest easy knowing that you should be able to profit no matter who wins in November.

I hope you found this special report useful. Before we go, let me remind you that you’re now also a member of my free Market 360 newsletter.

In Market 360, we discuss a variety of topics, ranging from the latest happenings in the markets to updates on stocks, earnings, exciting new trends and much, much more. Keep an eye on your email inbox for my next Market 360 article soon. I typically send them every Tuesday, Thursday, Friday and Saturday. In the meantime, you can check out the Market 360 archive by clicking here.

And if you haven’t yet, I recommend giving Portfolio Grader and Dividend Grader a spin. These are incredibly powerful tools that individual investors can use to help find the best stocks… as well as which investments to stay far away from.

Sincerely,

Louis Navellier

Editor, Market 360