The move in silver picks up steam… why more gains are likely… the latest trade winner from Jonathan Rose… why it still has legs… Eric Fry says it’s time to sell Amazon – what he’s buying to replace it

Wednesday brought the following headline:

As Silver Scores a Nearly 14-Year High, New Records Could Be Just Around the Corner for Precious Metals

If you acted on our early-May Digest, congrats – you’re already in this move.

In May, we highlighted the disconnect between gold and silver

While gold was setting all-time highs, silver was lagging and trading at a historically cheap level relative to its shinier cousin.

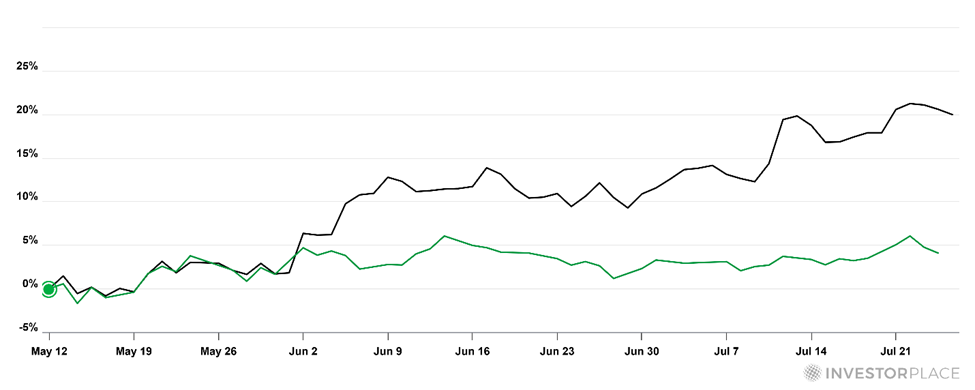

But since our May 12 Digest, silver has broken out.

As I write Friday, it’s trading at $39.06 per ounce – up 20% from our May Digest. Over that same period, gold has climbed less than 5%.

But even after this move, we think silver has more room to run.

To understand why, let’s revisit the gold-to-silver ratio

This is a key historical measure of relative value between these two metals. It tells us how many ounces of silver are equivalent in price to one ounce of gold.

In the 20th century, this ratio has averaged around 47:1. More recently, in the period from 2000 through 2020, it has averaged closer to 60:1.

Earlier this year, the ratio ballooned above 105 – just shy of its all-time high set during the COVID panic. As of our May 12 Digest, it was hovering around 102.

Today, it’s 86 and falling (bullish for silver). But as you can see below in the gold/silver ratio chart dating to 2000, the ratio still trades at elevated levels.

So, what happens from here?

Given today’s backdrop of geopolitical instability, ballooning sovereign debt, and the ongoing erosion of fiat currency credibility, we think gold’s recent gains are justified – and likely to continue. So, we don’t anticipate a meaningful decline in gold’s price beyond normal profit-taking and healthy “two steps forward, one step back” market action.

Therefore, if the gold/silver ratio is to continue normalizing toward the more recent average of around 60, it’ll be up to silver to do the heavy lifting – meaning silver’s price gains must outpace those of gold.

That’s exactly what we expect.

Supply constraints are a big reason why. According to the Silver Institute, global silver markets ran a deficit of roughly 117 million ounces in 2024 – the fifth straight year of undersupply.

And because most silver is produced as a by-product of mining other metals like copper and zinc, higher prices don’t necessarily lead to more supply anytime soon.

Then there’s the industrial side.

Silver plays a critical role in the clean energy transition, especially in solar panel production, which continues to grow rapidly. Throw in rising demand for electrification and high-tech components, and you have a metal that’s increasingly indispensable – yet still underpriced by historical standards.

Technically, the picture looks strong too.

As we noted earlier, silver just notched a 14-year high. The breakout came with solid volume, which raises the prospect of a continued run toward that 2012 peak near $48. That would be another 23% return from today’s level.

Of course, markets don’t move in straight lines. Silver’s recent strength could consolidate or even pull back in the short term. But big picture? The winds are finally at its back.

Bottom line: After years of underperformance, silver is stepping back into the spotlight. The gold/silver ratio remains elevated, the supply/demand imbalance is significant, and the technicals are breaking in the bulls’ favor.

Invest accordingly.

While silver’s breakout is drawing fresh attention to the broader metals space, one lesser-known name is breaking out

And if you’ve been trading it alongside veteran trader Jonathan Rose, you’re up 268% and counting in less than two months.

I’m talking about The Metals Company (TMC).

If you’re new to the Digest, Jonathan is the analyst behind Masters in Trading.

He earned his stripes at the Chicago Board Options Exchange, going toe-to-toe with some of the world’s most aggressive and successful moneymakers. He’s made more than $10 million over the course of his career, profiting from bull markets, bear markets, and everything in between.

As to Jonathan’s latest winner, TMC, it’s pioneering the exploration and potential commercialization of polymetallic nodules found on the ocean floor. These are rich in critical metals like nickel, cobalt, copper, and manganese – essential for powering electric vehicles, batteries, and the broader clean energy transition.

While not directly exposed to silver, TMC stands to benefit from the same global demand drivers that are pushing industrial metals higher.

On June 2, Jonathan sent his subscribers a trade brief that made the case for a bullish TMC position.

Here’s part of that brief:

Key Reasons This Is a Compelling Story

- Only Pure‑Play Exposure: TMC is the sole U.S.‑listed company exclusively focused on deep‑sea polymetallic nodules.

- Insider Alignment: Founding stakeholder Allseas’ large share and warrant purchase underscores confidence in TMC’s path forward.

Government Backing: A sitting President’s directive to accelerate critical‑minerals permitting significantly de‑risks the timeline.

First‑Mover Advantage: TMC leads the pack with the only fully filed ISA exploitation application and U.S. permit request in hand. - Massive Upside Potential: Access to vast polymetallic nodules in the Clarion‑Clipperton Zone taps into a multi‑billion‑dollar battery‑metals market.

I checked in on the trade this morning. With TMC’s stock up 74% since Jonathan’s June 2 alert, their calls are sitting on open gains of about 268%.

To help our broad Digest file who might have missed this trade, I asked Jonathan for his thoughts on TMC and the wider space looking forward

Here’s part of our conversation:

Jeff: TMC has been on a tear this year, up almost 600%. Is there still a trade here?

Jonathan: I think there is. And actually, this might be just the beginning of a longer-term revaluation.

What’s happening isn’t just about hype or momentum. It’s a convergence of really powerful tailwinds: We’ve got a potential 50% copper tariff about to kick in, a major executive order streamlining deep-sea mining approvals, and TMC already submitted the first commercial application.

That kind of regulatory and policy alignment is rare, and it’s happening fast.

Jeff: And didn’t I just read that Korea Zinc Co. invested $85.2 million in TMC last month? That seems like a big deal.

Jonathan: Huge. It’s not just $85 million in funding – it’s strategic. Korea Zinc brings R&D and refining infrastructure to the table, which helps de-risk TMC’s downstream operations.

Jeff: So, for someone late to the move, is it still worth chasing?

Jonathan: I’d say don’t think of it as chasing. Think of it as catching a secular wave early.

Yes, it’s up big year-to-date, but it’s still a micro-cap in a market that’s only just waking up to the geopolitical importance of seabed minerals.

It’ll be volatile – micro-cap stocks usually are – but if tensions with China stay elevated, the U.S. will need new, reliable sources of nickel, copper, cobalt. And TMC is literally sitting on the seabed supply. That narrative has legs.

Jeff: Thanks, Jonathan

Jonathan: Happy to help.

To get a better sense for Jonathan and his trading, check out his special seven-day intensive dedicated to showing traders how to spot the big institutional moves before anyone knows about them.

It walks you through the exact process Jonathan uses to follow the “Big Money Tell” and turn unusual options activity into real opportunity. Just click here to learn more.

Finally, a warning to Amazon investors

As an investor in Amazon, I perked up reading Eric Fry’s latest issue of Smart Money. He’s recommending selling the retail giant today.

Given Eric’s multi-decade career with more than 40 investments that have risen 1,000%+, it’s worth paying attention to such calls. But before we get to his rationale, let’s back up…

Eric began his latest update by contextualizing where we are at this moment in history:

Two giant economic forces are slamming into the U.S. stock market at the same time…

- We are living in the fastest rate of technological change that humankind has ever experienced, with artificial intelligence threatening to make the world we know unrecognizable in just a few years…

- Trade relationships and peace deals are hanging on by a fraying thread. If that thread breaks, it will unleash an unrelenting and painful era of chaos.

For Eric, this reduces to one takeaway…

It’s critical to correctly identify which companies to run from and which to run toward. Easier said than done in the age of exponential progress and mind-warping technological advances.

Now, Amazon is one of today’s market darlings – also an AI darling. But if Eric is right, this is a “run from” stock:

Amazon is going to be one of the prime (no pun intended) victims of the current administration’s trade war.

Up to 70% of what you see on Amazon comes from China. Tariffs on those goods means that Amazon could lose their competitive edge entirely.

Plus, Amazon’s cloud service division has missed analyst expectations for three-straight quarters. That’s the part of Amazon’s business that they consider to be their “growth driver.”

That is why CEO Jeff Bezos is panic-pumping $100 billion into this lagging part of their business. However, that investment is bleeding the company dry.

Amazon is scheduled to report Q2 earnings next Thursday. To Eric’s point, we’ll be listening for commentary on cloud service capex spending – and earnings forecasts.

For more on what stock Eric recommends you replace Amazon with, he just released a new “Sell This, Buy That” research package that goes into more detail.

Here he is with more:

It is a virtually unknown, fast-growing online retailer that could be like buying Amazon twenty years ago, but with even bigger competitive advantage.

And the smart money is already moving away from Amazon and toward this online retailer. Projections are showing that it could become 700% more profitable by 2027.

You can get more details right here.

We’ll keep you updated on all these stories here in the Digest.

Have a good evening,

Jeff Remsburg