Stocks are getting crushed. It increasingly appears that we’re spiraling into a recession. But luckily for investors, the bottom may not be far away.

Let me be clear: The U.S. economy is in bad shape. Indeed, all the ingredients that tend to produce economic contractions are present today. We have runaway inflation, Fed rate hikes, spiking Treasury yields, soaring oil prices, and falling consumer confidence.

With all those headwinds, it’s very likely that the U.S. economy does fall into a recession in 2023.

But given the strength of the labor market, the consumer, and corporate balance sheets, it’s equally likely that any recession we do experience will be short and shallow.

Here’s the kicker. Based on our analysis, stocks are already priced for a short and shallow recession. That means that even if the U.S. economy enters a recession next year, stocks will likely move higher from here.

The investment implication? It’s time to go dip-buying.

The Earnings Outlook

The first part of our analysis on why stocks might’ve bottomed centers around how corporate earnings usually fare during recessions.

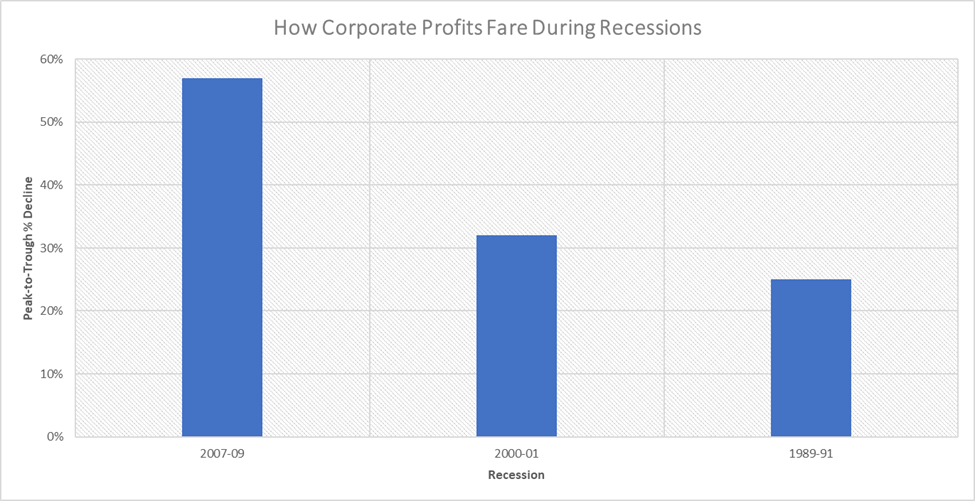

Over the past 40 years, excluding the very temporary COVID-induced recession of 2020, we’ve had three major economic recessions. Of those three, one has been deep (2007-09) and two have been shallow (1989-91 and 2000-01). The deep recession caused a near-60% drop in corporate earnings per share (EPS) over the course of two years. The shallow recessions resulted in ~30% drops in corporate EPS over the course of one to two years.

Let’s say that we’re at the corporate earnings peak today and that the coming recession is a shallow one. That means that over the next 12 to 24 months, corporate EPS will drop about 30%.

Corporate EPS today sit around $216. A 30% haircut would put EPS at $150 within the next to 12 to 24 months.

While that’s a big drop, our analysis suggests stocks are already priced for it!

What About Multiples?

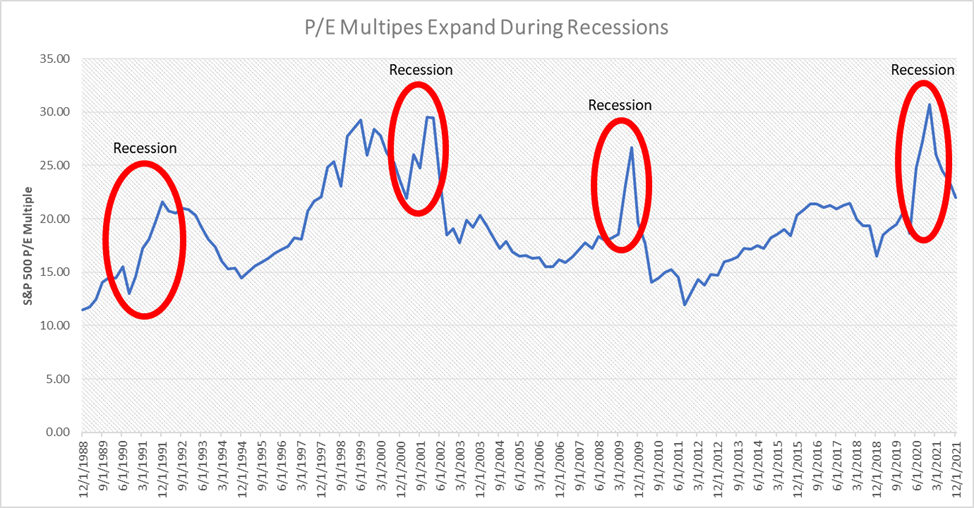

It’s also true that during recessionary periods, equity multiples tend to expand as earnings drop. That’s because:

- Treasury yields tend to drop as investors pile into bonds for safety.

- Investors start to price in better earnings in the future.

Therefore, historically speaking, recessions are defined by this tug-of-war between drops in EPS and rises in the equity multiple.

For example, in 2007-09, the S&P 500 expanded to a 25X trailing price-to-earnings (P/E) multiple at the market bottom (from 17X at the peak). In late 2001, the price-to-earnings multiple got as high as 30X (from 25X at the peak). In 1991, it got all the way up to 22X (from 12X at the peak).

It even happened during the 2020 mini recession!

Let’s do some math.

Historically, the P/E multiple on the S&P 500 has expanded to about 27.5X during previous recessionary periods. Given Treasury yields are lower than where they’ve been during previous recessions, that seems totally reasonable this time around.

A 27.5X P/E multiple on $150 in EPS gives the S&P 500 a 12- to 24-month price target of $4,125.

That’s above where the index trades today.

Therefore, even if the U.S. economy falls into a shallow recession in 2023, stocks should pop over the next year.

The Final Word on a Possible Recession

We’re in a bear market. That’s scary.

But it pays to remember that every bear market eventually turns into a bull market. And those who buy high-quality stocks in bear markets and wait for the bull market to carry them higher make fortunes.

The key to beating a bear market, then, is to simply find those high-quality stocks, buy and hold.

That’s what we’re doing in our flagship Innovation Investor research service. We’re ignoring the macroeconomic noise because its temporary and will pass. In the meantime, it’s giving us the opportunity to buy truly fantastic companies at fire-sale prices. And it’s allowing us to create a portfolio of stocks that will soar more than 5X over the next five years.

If those are the kind of returns you’re looking for, then you need to click here to learn more.

P.S. Charlie Shrem and I will be holding an emergency briefing on June 14 at 7 p.m. Eastern, wherein we’ll discuss how the phenomenon plaguing the crypto markets could mint a new wave of crypto millionaires.

Despite all the negative headlines we’ve been seeing, a new day is dawning. And a select few off-the-radar coins will emerge as the new leaders of the cryptocurrency markets.

If you want to get ahead of this phenomenon, sign up for my free Crypto in Crisis event now.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.