Yesterday, the stock market crashed. It was Wall Street’s worst day in over two months. The Dow Jones lost about 1,000 points. The S&P 500 shed more than 3%. The Nasdaq crashed nearly 4%.

The catalyst? In a short speech Friday morning, Federal Reserve Chair Jerome Powell said the central bank will keep its foot on the gas when it comes to rate hikes.

Of course, now there’s one big question on everyone’s minds. Is this a healthy pullback in a new bull market, or the return of a nasty bear market?

We think the evidence strongly suggests the former.

Moreover, we think the evidence strongly suggests that stocks are nearing a local bottom. At that point, they’ll reverse course – and soar more than 20% into the end of the year.

Amidst that rally, we believe certain high-growth stocks can rise 100-plus.

So, if you’ve been waiting for an opportunity to buy into the summer stock market rally, now is your chance.

Here’s a deeper look.

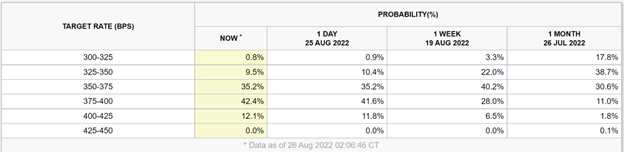

Chart 1: Federal Reserve Chair Powell’s Remarks Weren’t That Hawkish

They say a picture paints a thousand words. So, in the spirit of that idea, we’ve compressed our bullish evidence into five simple charts.

The first chart shows that Powell’s remarks– while construed as super hawkish by the equity markets – were actually not that hawkish at all.

In listening to the speech, we didn’t notice out-of-the-norm hawkishness in Powell’s words or tone. He basically said what he has been for months. In short (paraphrasing): “We’re going to keep fighting inflation until inflation dies. And if the economy has to take a hit in the cross-fire, so be it. We have to kill inflation.”

Very normal. The stock market, however, reacted negatively. And that’s puzzling because no other market reacted negatively.

Of particular interest, the Federal Reserve funds futures market – which gauges market expectations of the course of monetary policy – didn’t budge!

Before Powell’s speech, that market was pricing in a 35% chance the target rate would hit 350 bps by February 2023, a 42% chance it would hit 375, and a 12% chance it would hit 400. After the speech, none of those odds moved more than a percent.

In other words, the market isn’t suddenly pricing in a more hawkish Fed. It’s pricing in the same Fed it was pricing in on Thursday, when stocks were rallying.

This makes yesterday’s selloff look like technical selling, and nothing more. And that implies it could be a great buying opportunity.

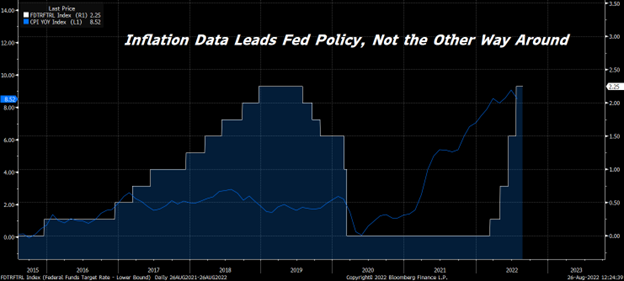

Chart 2: Federal Reserve Policy Is Reactive, not Proactive

Our second chart illustrates why the big focus on Federal Reserve policy is quite silly. And that’s because Fed policy is reactive, not proactive.

Indeed, Jerome Powell is not the driver of the macroeconomic action. He’s a byproduct of that action.

That is, the Fed isn’t setting monetary policy on its own. It is, in its own words, data-dependent. It’s setting monetary policy based on the incoming data – specifically, based on the incoming inflation data.

Just look at how the Federal Reserve funds target rate consistently lags the inflation rate.

Therefore, it can be concluded that Powell’s commentary and the Fed’s action are themselves byproducts of the inflation data.

If the inflation data improves over the next few months, Powell’s commentary will shift increasingly dovish. And the Fed’s rate-hike cadence will slow. If the inflation data worsens over the next few months, Powell’s commentary will shift increasingly hawkish. And the Fed’s rate-hike cadence will accelerate.

Basically, Fed commentary and policy are the output, while inflation data is in the input. Therefore, we should care less about what Powell is saying about Fed policy and more about what the data is saying about inflation.

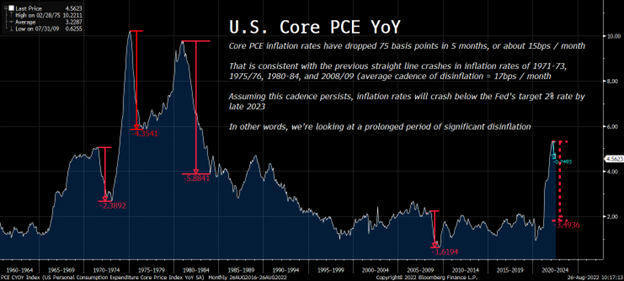

Chart 3: Inflation Is Collapsing

The third chart paints a very compelling picture of why we see inflation rates collapsing over the next several months.

Yesterday, Personal Consumption Expenditures (PCE) data was released for the month of July. And it was very bullish.

Headline PCE rose just 6.3% year-over-year, below expectations for a 6.4% rise and far lower than the prior month’s 6.8%. Same story on the core side. Core PCE rose 4.6%, below expectations for a 4.8% jump and slower than the prior month’s 4.8%.

On a month-over-month basis, core prices rose just 0.1%, while headline prices actually dropped.

Inflation is clearly slowing. Importantly, the cadence of this slowdown is consistent with previous crashes in inflation.

That is, core PCE rates have now dropped about 75 basis points over the past five months. That’s about 15 basis points per month. That cadence of disinflation is consistent with previous eras of crashing inflation, like 1971-73, 1975-76, 1980-84, and 2008-09. In those periods, the average cadence of disinflation was 17 basis points per month.

In other words, the current trend of disinflation is nearly identical to prior periods of crashing inflation.

This implies we’re in the early stages of an inflation crash. If the trend persists and history repeats, inflation rates will crash below 2% by late 2023.

If inflation steadily drops from 6% to 2% over the next 18 months, stocks will rise meaningfully in that period.

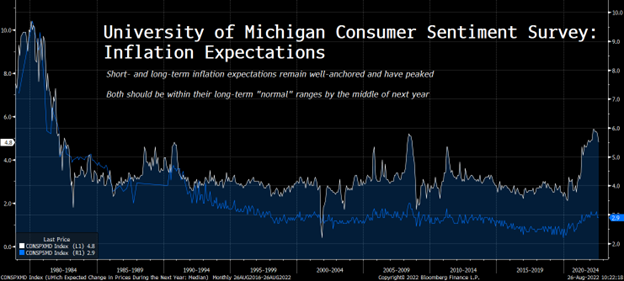

Chart 4: Inflation Expectations Are Collapsing, Too

The fourth chart shows that it’s not just inflation rates that are dropping right now. It’s inflation expectations, too. And they themselves are very important to the overall course of inflation.

About an hour after July PCE data was released yesterday, the University of Michigan reported the results of its monthly consumer sentiment survey.

The most important tidbit from the survey was that inflation expectations are crashing.

Long-term inflation expectations have dropped to 2.9% and are now within their historically normal range of 2% to 3%. Meanwhile, short-term inflation expectations have dropped sharply over the past few months to 4.8%. That still puts them above the historically normal range of 2.5% to 3.5%. But at current deceleration rates, we should be there in no time.

This is important because well-anchored long-term inflation expectations will help accelerate the decline of inflation and the timeline to a dovish pivot from the Federal Reserve.

Of course, those things will help propel stocks higher.

Chart 5: Technical Support Shows Up Very Soon

Our final chart illustrates that last week’s stock market crash happened within the bounds of an uptrend channel for stocks. And solid technical support should arrive soon for the market.

On a technical basis, there is nothing unusual about the current market selloff. Stocks formed a new uptrend channel in mid-June. We still haven’t reached the support line of that channel – just above 4,000 for the S&P 500.

Therefore, so long as all this volatility occurs above 4,000 and within the bounds of this new uptrend channel, the technical picture will continue to support a 20% move higher in equities into the end of the year.

The Final Word

They say money is made in bull markets – but fortunes are made in bear markets.

Right now, we could be on the cusp of a fortune-making transition from a bear to a bull market. If so, investors who buy the right stocks today could see 100%-plus returns over the next few months alone.

We already got a taste of this from mid-June to mid-August. In that rally, the markets rose about 20%. And our favorite stocks to buy today roared about 60% higher!

If this current market selloff does make a U-turn and transforms into a big rally into the end of the year, our portfolio of stocks could easily rise 100%.

If I were you, I’d want to find out the names of the stocks in this explosive portfolio – at the very least.

To do just that, click here.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.0