Brown-Forman (BF.A) (BF.B) engages in the manufacturing, bottling, importing, exporting, marketing, and selling alcoholic beverages. It provides whiskey, ready-to-drink products, vodka, tequilas, champagnes, wines, liqueur, and other distilled spirits. This Dividend Champion has paid dividends since 1960 and has increased them for 30 years in a row.

The company’s latest dividend increase was announced in November 2013 when the Board of Directors approved a 13.70% increase in the quarterly annual dividend to 29 cents per share. The company’s peer group includes Diageo (DEO), Beam (BEAM), and Constellation Brands (STZ).

Over the past decade this dividend growth stock has delivered an annualized total return of 14.80% to its shareholders.

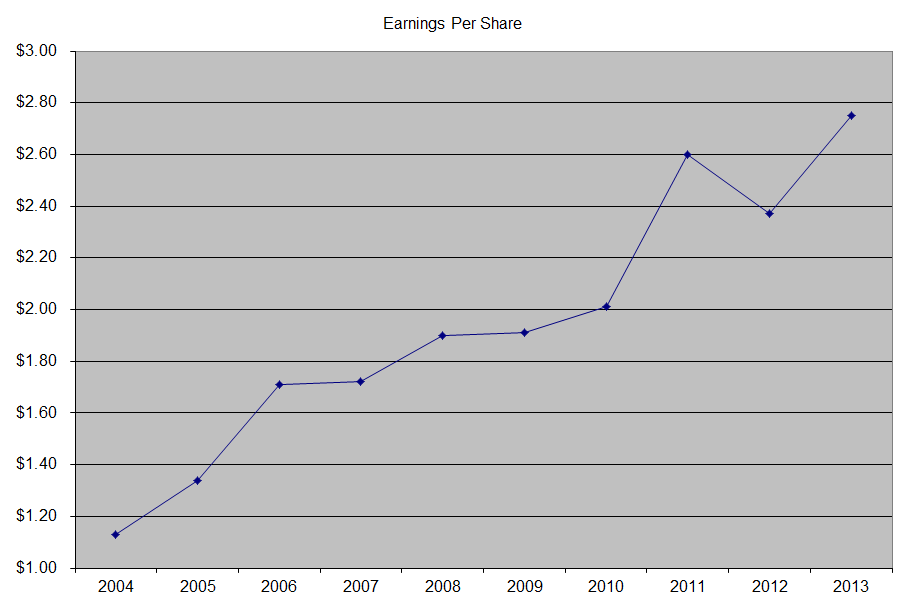

The company has managed to deliver an 11% average increase in annual EPS over the past decade. Brown-Forman is expected to earn $2.96 per share in 2014 and $3.26 per share in 2014. In comparison, the company earned $2.75 per share in 2012.

In addition, between 2004 and 2013, the number of shares decreased from 229 million to 215 million.

The company has several strong brands such as Jack Daniels Tennessee Whiskey, which accounts for a large portion of its revenues. Other brands include Finlandia and Southern Comfort. There is strong customer loyalty for company’s products, particularly for its Jack Daniels line of whiskeys, which results in strong pricing power. If you want Jack Daniels, and the store doesn’t sell it, you will likely go to another store. This is an example of a wide-moat. Another example include the high returns on equity and capital that the company has been able to generate over the past decade.

Besides growth in Jack Daniels whiskey, which has recorded 21 years of consecutive volume increases, the company grows sales through brand extensions, such as Gentleman’s Jack.

Another venue for growth includes international expansion. Currently 59% of sales come from international versus 15% that were generates 20 years ago. About 30% of sales were generated in Europe, 14% Australia, and 15% in other countries such as Mexico and Japan. As a result, I believe there is plenty of room for growth in emerging countries such as China, Brazil, and Russia, to name a few obvious opportunities.

The company owns its distribution in many markets such as Australia, Brazil, Canada, China, Mexico, Turkey etc. In other markets such as Russia, Japan, South Africa, it operates under fixed term contract with distributors. In the UK,which accounted for 9% of sales in 2013, Brown-Forman has a cost sharing agreement with Bacardi. The company is focused on investing in its distribution network, which allows it to focus on its brands and improve margins. In 2014, it will start operating its own distribution network in France.

Other room for growth could include strategic acquisitions. Previous acquisitions include Finlandia Vodka, Southern Comfort, Casa Herradura and Chambord Liqueur Brand. Interesting enough, Jack Daniel’s Tennessee Whiskey was acquired in 1956 for $20 million.

Management has been very shareholders friendly, as it has deployed capital intelligently, in order to maintain high returns on capital invested. In addition, they distributed special dividends in 2010 and 2012, when preferential tax treatments on qualified dividends were set to expire. They rank each of the company’s brands according to its return on investment. The adherence to intelligent capital allocation means that they pour dollars only into their most promising brands.

There are a couple risks that I see with Brown-Forman stock. The first risk is that the Brown family exerts a lot of control over the company through the dual-class shareowner structure. For example, the A shares have voting rights, while the B shares have no voting rights, although they do share same proportionate amounts of dividends. The Brown Family has over 66% of the voting power, through its ownership of A shares either directly or through family controller entities. Hence the company is classified as a “controlled company”.

The other risk is that there is too much reliance on Whiskey sales, which could be bad for revenue growth if consumer tastes change. Jack Daniels category accounts for over half of product volumes.

The annual dividend payment has increased by 10.20% per year over the past decade, which is slightly lower than the growth in EPS. The growth in distribution payments over the next decade will likely be equal to or slightly higher than the growth in earnings per share.

A 10% growth in distributions translates into the dividend payment doubling every seven years on average. Since 1988, Brown-Forman has been able to double dividends every eight years on average.

Not included in the chart are special dividends of $4 per share in 2012 and 67 cents per share in 2010.

The dividend payout ratio has largely remained in a range between 32% and 39% over the past decade. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

The company has a really high return on equity, which is common for most high quality dividend payers that do not require a lot of equity to operate the business. Rather than focus on absolute values for this indicator, I generally want to see at least a stable return on equity over time.

Currently, Brown-Forman stock is overvalued, as it trades at a P/E of 27.20 and yields only 1.60%. I am analyzing the company because I believe it is a quality dividend growth company, which will be a very good addition to my portfolio on dips below $60. I will still keep holding onto my existing shares, which I believe have a value of approximately 30 times earnings to a private owner. As earnings will increase over time, that value should increase as well. To put it in Warren Buffett terms, this is an excellent business, but unfortunately the price is too rich to justify an investment at present terms.

There has recently been M&A activity in the industry, as Beam is in the process of being acquired by Japanese company Suntory at 30 – 32 times earnings. It is possible that Brown-Forman shares could have been bid up because they could be a potential acquisition target by a larger competitor.

However the dual-class shareholder structure, and the fact that voting power is concentrated in the Brown family, makes a successful acquisition of Brown-Forman by someone like Diageo highly unlikely. This could be a plus however, as acquisitions of quality dividend companies rob shareholders of the acquisition target from the dividend growth potential they could have enjoyed, had the company not been bought out. If earnings per share double every decade, and dividend payout ratios are maintained, long-term investors will do just fine.

I currently find Diageo to be a much better value, at 18.70 times earnings and yield of 2.40%. Therefore, I recently purchased Diageo shares.

Full Disclosure: Long BF.B, DEO