Like many of its peers, Regeneron Pharmaceuticals Inc (NASDAQ:REGN) is anxious to get back on the right track. Last year, REGN stock pulled in more than 32% returns for investors. This year, Regeneron is staring at steep, double-digit losses. Armed with a number of therapies in its impressive product pipeline, REGN should — in theory — be a market leader. However, will buyers respect the fundamental outlook?

On the bullish side, the immediate picture looks fairly positive. Regeneron stock gained 4% since last week’s closing price, partly due to an agreement reached with the U.S. Department of Health and Human Services.

On the bullish side, the immediate picture looks fairly positive. Regeneron stock gained 4% since last week’s closing price, partly due to an agreement reached with the U.S. Department of Health and Human Services.

The deal calls for Regeneron to “manufacture and study two antibody therapies for the prevention and treatment of Middle East respiratory syndrome (MERS),” according to Zacks Equity Research.

Tailwinds for REGN Stock

The announcement is particularly enticing for REGN stock as an officially approved treatment or vaccine does not exist for MERS. Despite its name, MERS is not limited to the Middle East, where the disease originated.

Due to the proliferation of global tourism, infections have been reported from the U.S. to Thailand. Since September 2012, there have been nearly 1,800 confirmed cases of MERS, and 640 deaths resulting from the disease.

Prospects for REGN stock are additionally buoyed by the company’s “rapid response platform,” which targets new infectious threats. True to its name, Regeneron is developing a preclinical program to attack the Zika virus. Once considered a regionally isolated problem, Zika could potentially affect Florida’s multibillion-dollar tourism industry.

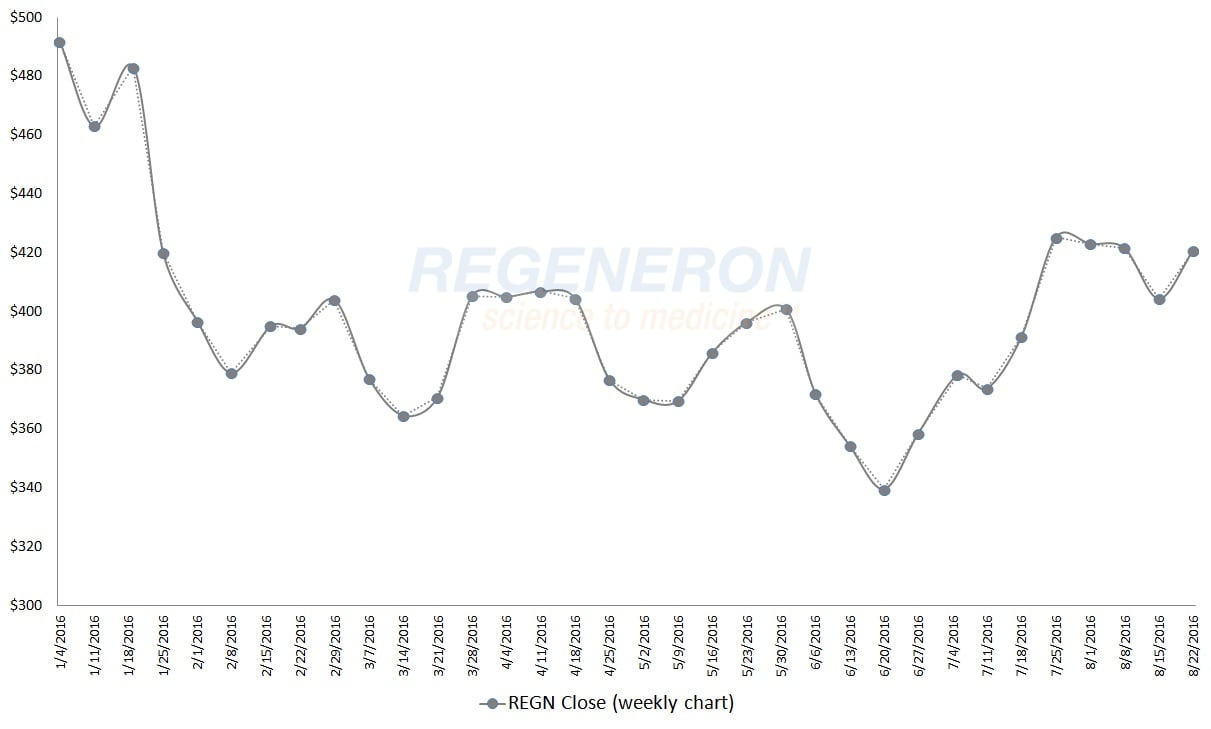

Yet for all its industry tailwinds, Regeneron stock has had an alarming lack of upside momentum. After briefly touching the $600 level last year, REGN never looked the same.

Regeneron Hurt by High Expectations

Some of that is attributable to its mixed second quarter of fiscal year 2016 earnings report. Although Regeneron beat its consensus earnings target by nearly 7%, revenue was a different story. Total sales registered at $1.21 billion, which is a 21% increase year-over-year but fell short

of expectations at $1.24 billion.

It was a rather unfortunate miss. Eylea, Regeneron’s flagship drug, continued to earn its reputation with revenues of $831 million against a forecast of $812 million. However, collaboration revenue between REGN and Sanofi SA (ADR) (NYSE:SNY) missed by $60 million.

True, sales from such partnerships are difficult to predict, and it would be unfair to judge REGN stock on that alone. At the same time, shares are down 5% since the Q2 release. Clearly, Wall Street is concerned about something.

This is where Regeneron could do itself a lot of good. Despite the recent volatility, REGN stock is still trading over $400. A stock split is just what the doctor ordered.

Click to Enlarge

First, it’s common practice for companies to dilute their outstanding shares. Psychologically, it would allow investors of more modest accounts to consider buying REGN stock. Current shareholders don’t have a problem with it because the market capitalization remains the same.

To the former point, it also increases the units of shares owned. Finally, REGN stock is underperforming its peers, and it is priced higher on paper. Regeneron would have nothing to lose with a little gamesmanship.

Bottom line for REGN

Regardless of whatever path it chooses, the bottom line is that REGN has enviable problems. Taking aside high expectations from analysts, its profit margins and revenue growth are among the best of the pharmaceutical industry. REGN has to spend money to make money, and that inevitably means there will be a few disappointing financial reports.

But optimism towards REGN stock has to be tempered. The fact that the paper price of Regeneron stock is so lofty suggests that many of its shareholders are well-to-do. In fact, the latest read on institutional ownership is up there at nearly 93%.

If the big money is worried, that’s a more reliable gauge than any analyst’s ratings.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.