If you are looking for the most compelling investing opportunities, look no further. The S&P 500 is rallying at breakneck speed right now. That’s all well and good, but it can leave stocks vulnerable to a pullback. In these times, I believe it’s particularly important to pick stocks with plenty of support. Here I used TipRanks’ new Smart Score tool to find seven top stock names that are poised to outperform. The Smart Score harnesses value from 8 unique data sets to create a powerful rating that is updated on a daily basis. All the stocks covered below have a ‘Strong Buy’ Street consensus.

As you will see, I also include Smart Score screenshots for each stock so that you can see for yourself how the score breaks down. Lastly, as you would expect, the Score is measured out of 10, and anything over ‘8’ is considered as an ‘Outperform’ rating. With that in mind, let’s take a closer look at why these 7 stocks score so highly now:

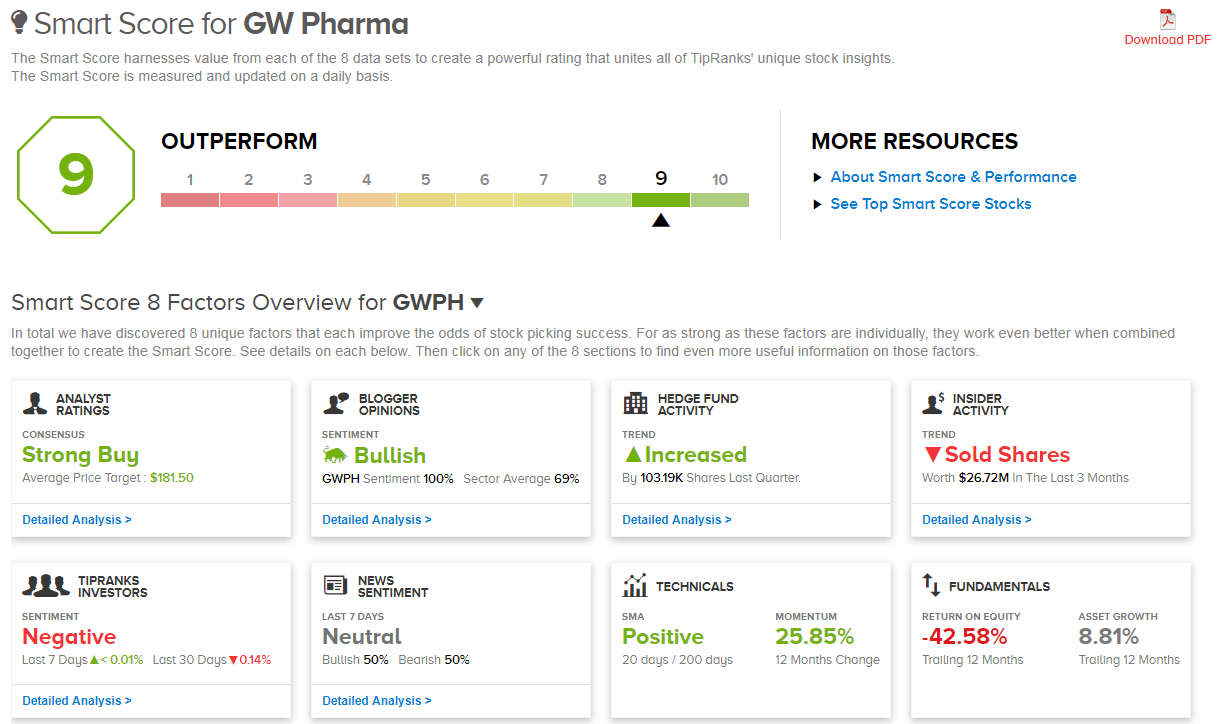

GW Pharma (GWPH)

British-based GW Pharmaceuticals (NASDAQ:GWPH) boasts the first natural cannabis plant derivative to gain market approval in any country. Mouth spray nabiximols was launched all the way back in 2010 to treat multiple sclerosis symptoms. And in 2018 this was followed by another cannabis-based product, Epidiolex for the treatment of epilepsy.

So far the Epidiolex launch has exceeded expectations, sending shares surging 76% year-to-date. In fact, the early demand was so great that GW’s specialty pharmacy distribution network and patient support services were overwhelmed. GW has now improved its patient support services and broadened its distribution network from 5 specialty pharmacies to over 140 distribution points.

Cantor Fitzgerald analyst Elemer Piros has just hosted a dinner with GWPH senior management. The meeting has furthered his conviction of the stock’s potential. “With awareness high and efficacy in devastating seizure disorders, Epidiolex’s launch has gotten off to a fast start. Management is working diligently to execute and make sure Epidiolex fulfills its potential. We continue to expect Epidiolex to achieve $1B+ in peak sales, and think GW is undervalued for its potential” writes Piros. He has a $196 price target on the stock.

Looking ahead, Piros notes that Epidiolex is also undergoing trials for tuberous sclerosis complex (TSC). A Phase III trial in TSC is now fully enrolled with data expected in Q2:19.

The stock also displays bullish blogger sentiment, increased hedge fund activity, very bullish news sentiment and positive technical on both a 20 day and 200 day basis. That’s why it has a Smart Score of ‘9.’ Get the GWPH Stock Research Report.

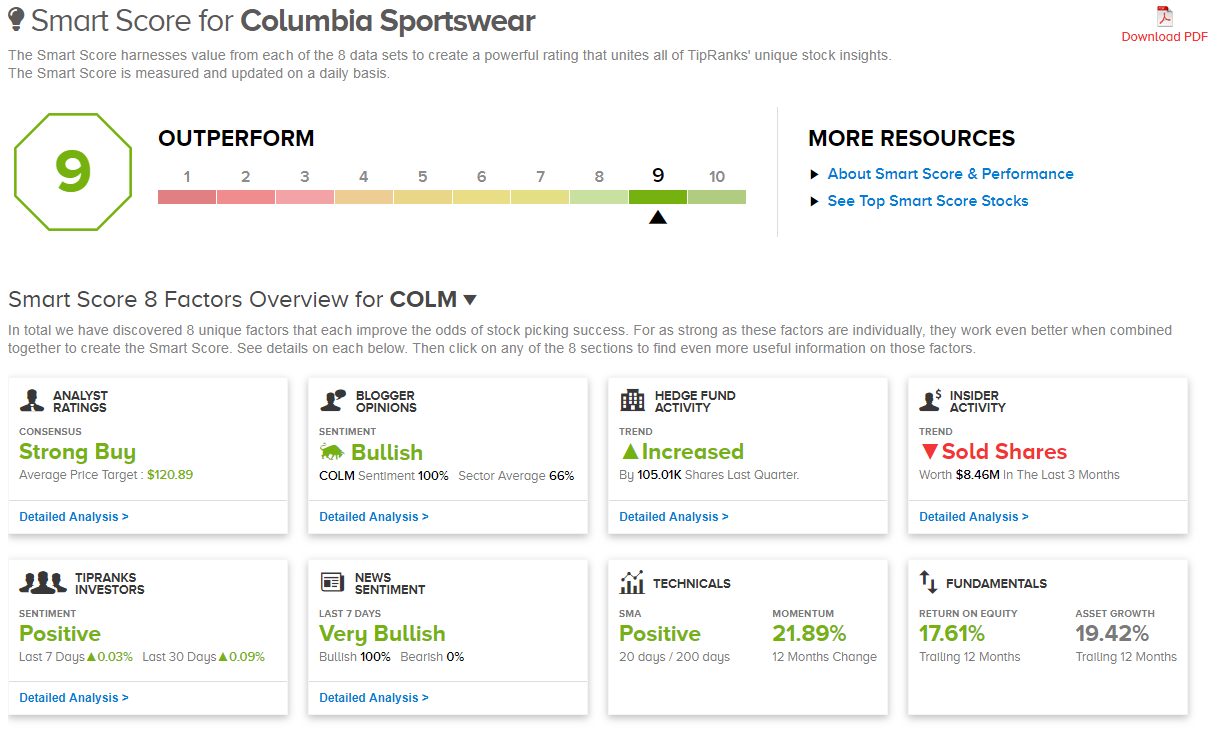

Columbia Sportswear (COLM)

The well-known sports retailer is enjoying a strong start to 2019. Columbia Sportswear Company (NASDAQ:COLM) just reported a sizable Q1 earnings beat, while also raising guidance. Sales surged 8% to $655 million with broad-based strength across brands (Columbia, Sorel, PFG).

The well-known sports retailer is enjoying a strong start to 2019. Columbia Sportswear Company (NASDAQ:COLM) just reported a sizable Q1 earnings beat, while also raising guidance. Sales surged 8% to $655 million with broad-based strength across brands (Columbia, Sorel, PFG).

COLM’s momentum has carried into 2019, cheers five-star Guggenheim analyst Robert Drbul. He has just reiterated his buy rating while bumping up the price target from $120 to $125. “We are encouraged by the continued momentum in the business and believe the company is well positioned to continue to drive outsized results, with +HSD% top-line/+DD% bottom-line growth in FY19/20, by our estimates” the analyst commented following the results release.

As for the rest of 2019, Drbul expects that Columbia and Sorel will drive top-line growth, and notes that order book trends are improving (particularly for fall 2019 in the U.S.). “We believe the channel is clean and that the company has solid visibility into back half wholesale revenues, with strong orders for fall, encouraging for the remainder of the year” Drbul tells investors.

Aside from eight back-to-back buy ratings, COLM also has the support of bloggers, hedge funds and investors. This drives a top-notch Smart Score of ‘9.’ Get the COLM Stock Research Report.

Halliburton (HAL)

Multinational corp Halliburton Company (NYSE:HAL) has not had an easy time recently. But don’t let that deter you from this intriguing investing proposition. As one of the world’s largest oil field services companies, Halliburton is in prime position to benefit from the recovery in international drilling activity. “We view Halliburton as the having the highest leverage to the growing commodity upcycle among large-cap peers and remains our highest-conviction large cap name” cheers Raymond James analyst Praveen Narra.

Multinational corp Halliburton Company (NYSE:HAL) has not had an easy time recently. But don’t let that deter you from this intriguing investing proposition. As one of the world’s largest oil field services companies, Halliburton is in prime position to benefit from the recovery in international drilling activity. “We view Halliburton as the having the highest leverage to the growing commodity upcycle among large-cap peers and remains our highest-conviction large cap name” cheers Raymond James analyst Praveen Narra.

He reiterated his ‘Strong Buy’ rating on HAL on April 23 after the company reported a Q1 earnings beat. That came with a $45 price target for upside potential of 56%. HAL revealed an 11% gain in international revenue, although North American revenue pulled back 7% due to a slower-than-expected start for hydraulic fracking.

According to Narra, the North American business has now bottomed, and investor fears for the second half of 2019 are overdone, said the analyst. Plus he commented that HAL looks appealing from both a relative and absolute perspective. Indeed, in the last three months, HAL has received only buy ratings from the Street.

According to Narra, the North American business has now bottomed, and investor fears for the second half of 2019 are overdone, said the analyst. Plus he commented that HAL looks appealing from both a relative and absolute perspective. Indeed, in the last three months, HAL has received only buy ratings from the Street.

With a Smart Score of ‘9’, this is a company with multiple positive datapoints, including a Strong Buy analyst consensus and an average analyst price target that indicates upside potential of over 40%. Get the HAL Stock Research Report.

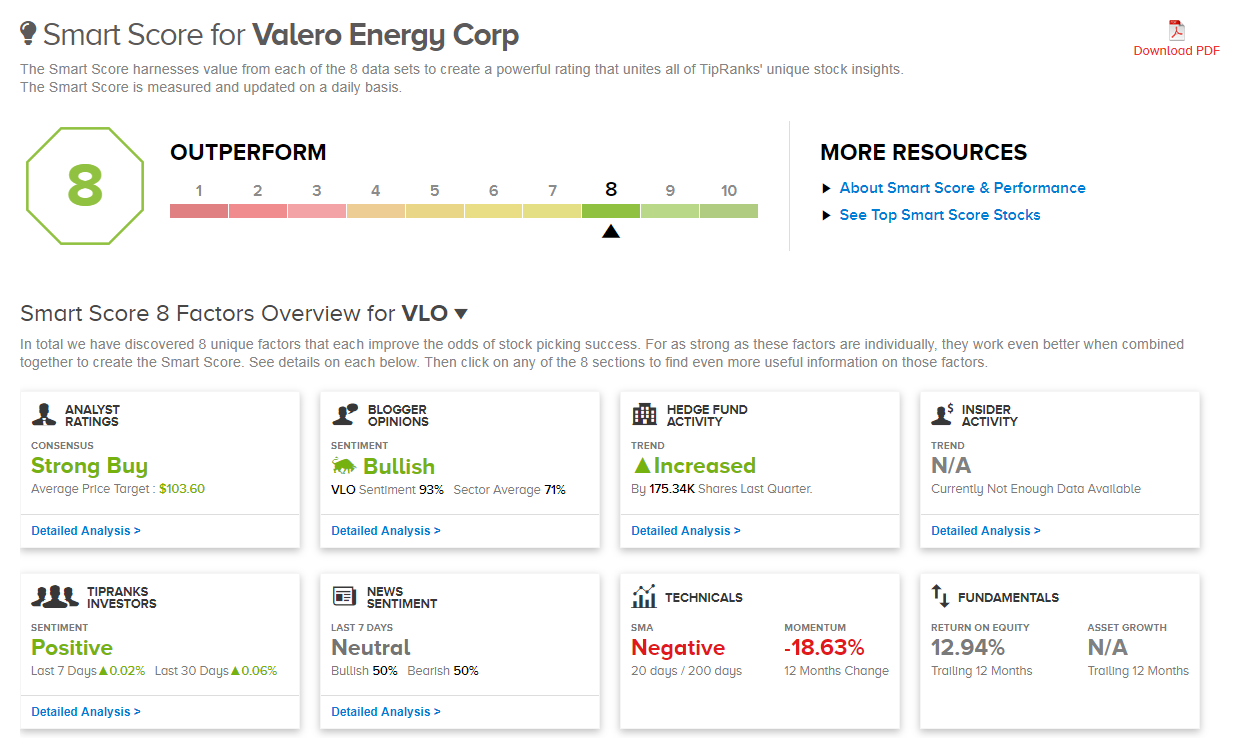

Valero Energy Corp (VLO)

Texas-based

Texas-based

Valero Energy (NYSE:VLO) is the largest independent refiner in the world. We are talking about a total crude throughput capacity of nearly 2.4 million barrels per day. And even a difficult macro environment can’t rain on Valero’s parade.

Most notably, RBC Capital’s Brad Heffern reiterated his buy rating on April 25, writing: “1Q19 EPS of $0.34 was a strong result given the worst macro environment in several years, and was made more impressive by the fact that VLO is a merchant refiner.”

Indeed, the 1Q19 refining macro environment was one of the worst in memory. Specifically VLO’s blended indicator fell to its second-lowest level going back to 2012. “We are happy to move on from this quarter, as the macro has improved significantly… but it is reassuring to see VLO can still put up positive earnings in a very weak environment” writes Heffern.

Looking forward, the analyst expects Valero to return to its strong repurchase program in the coming quarters. He sees VLO repurchasing more than 10% of its outstanding shares in 2019–20 (about $350 million in the second quarter).

As the Smart Score shows, VLO scores highly on multiple datapoints. These include a ‘Strong Buy’ consensus from analysts, bloggers and hedge funds, as well as positive news sentiment. That gives VLO an ‘Outperform’ rating. Get the VLO Stock Research Report.

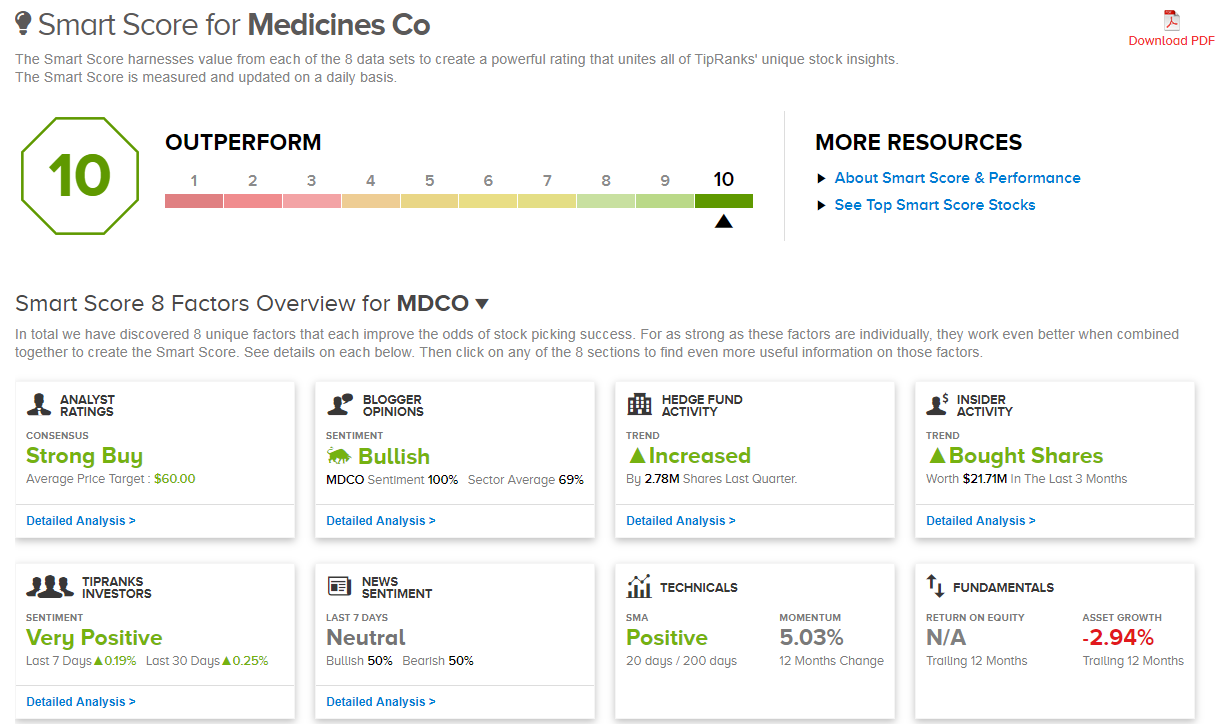

The Medicines Co (MDCO)

The Medicines Company(NASDAQ:MDCO) is focused on one of the greatest global healthcare challenges today — atherosclerotic cardiovascular disease. Atherosclerosis involves the narrowing of the inside of an artery, causing reduced blood flow and potentially a heart attack or stroke. That means MDCO is operating in a massive $20 billion market.

The Medicines Company(NASDAQ:MDCO) is focused on one of the greatest global healthcare challenges today — atherosclerotic cardiovascular disease. Atherosclerosis involves the narrowing of the inside of an artery, causing reduced blood flow and potentially a heart attack or stroke. That means MDCO is operating in a massive $20 billion market.

Its key drug candidate is cholesterol-lowering injection inclisiran. The drug, which is injected twice-a-year, is now undergoing pivotal Phase 3 trials. Ahead of 3Q19 pivotal readouts, MDCO will present interim phase II data on 18 May and on 27 May. If the data is positive, shares could move significantly higher.

Indeed, with shares now at $32, the average analyst price target of $60 suggests 88% upside lies ahead. Chardan Capital’s Gbola Amusa is even more bullish with a $90 price target (181% upside potential). This five-star analyst highlights MDCO as a Chardan Top Pick for 2019.

“Given cost-efficient execution by MDCO on advancing towards multiple inclisiran clinical readouts in the coming months, including the pivotal phase III readout of inclisiran in 3Q19, we maintain our high-conviction Buy rating and increase our PT to $90 (from $85)” the analyst wrote on April 26.

In another positive sign for the stock Goldman Sachs’ Paul Choi has now upgraded MDCO from Hold to Buy. With the phase III data release fast approaching, the Goldman analyst doubled his price target from $25 to $50. And with the highest-possible Smart Score of ‘10’, I say its full steam ahead from here. Get the MDCO Stock Research Report.

Smartsheet Inc (SMAR)

![]()

Smartsheet Inc (NYSE:SMAR) has already surged by almost 70% year-to-date, but that isn’t a reason to discount SMAR from your buy-list. Most notably, five-star Stephens analyst Dmitry Netis is still singing the praises of this software stock. For those who don’t know, Smartsheet is a work execution platform that helps teams plan, track, and manage projects in real-time.

Netis has a $55 price target on shares, suggesting that there is still 30% upside ahead. After paying a visit to SMAR headquarters, he told investors “We reiterate our Overweight rating, as we increasingly have confidence in management’s ability to scale revenues to a $1 billion revenue run rate within the next 4-6 years.” According to the analyst, SMAR stands out from both established players and smaller upstarts thanks to its customer-first culture and engaging user experience.

“We continue to be impressed with the caliber of Smartsheet’s management team and its product-focused, customer-first culture, which drives continued innovation and product development (~90% product roadmap is from customer feedback)” summed up Netis.

Overall the stock boasts a ‘Strong Buy’ Street consensus, with a Smart Score of ‘9’ reflecting positive activity from bloggers, hedge funds, investors and Very Bullish news sentiment. In fact, SMAR proved particularly popular with hedge funds in the last quarter according to 13F filings. Funds increased total holdings by 42% from 6.08 million shares all the way to 8.68 million. Get the SMAR Stock Research Report.

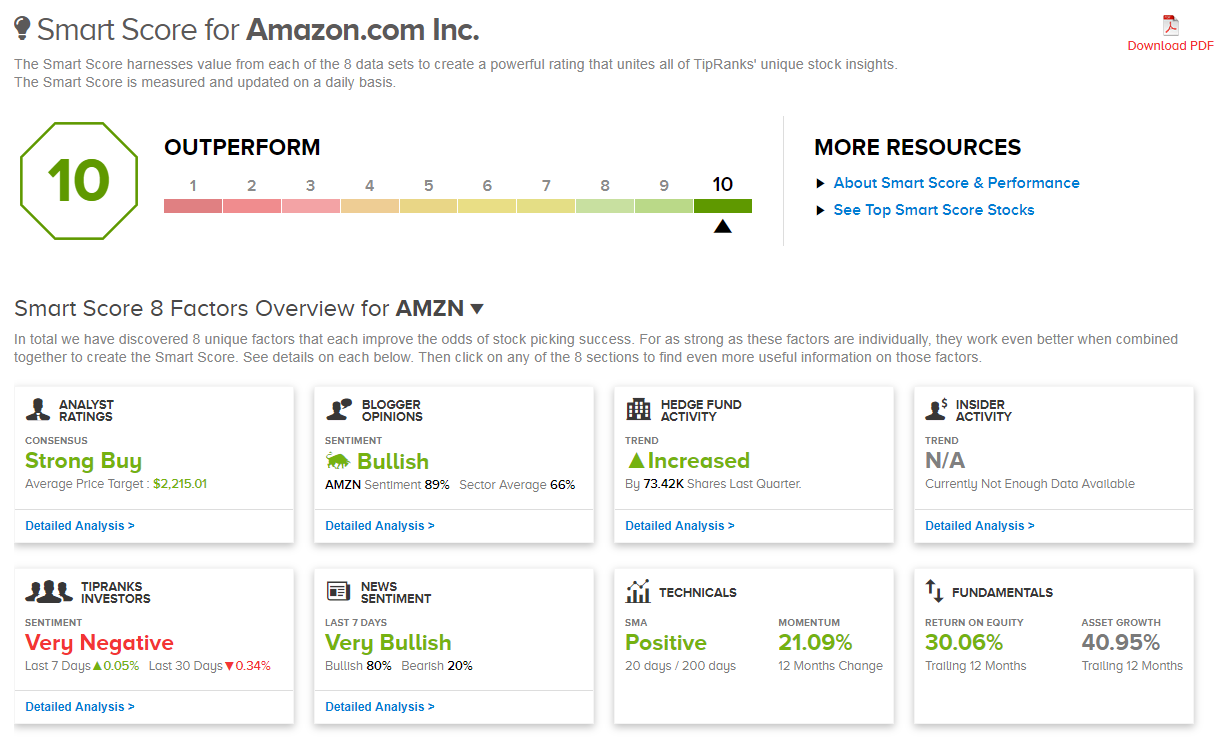

Amazon Inc (AMZN)

Our seventh top pick is A-grade mega-cap Amazon (NASDAQ:AMZN). Alongside a ‘perfect’ Smart Score of ’10’, Amazon also boasts a whopping 36 recent buy ratings from the Street. No hold or sell ratings here.

Following earnings, Goldman Sachs’ Heath Terry significantly boosted his AMZN price target from $2,100 to $2,400. From current levels that translates into a further 22% upside potential.

The five-star analyst explained: “We continue to believe AMZN represents the best risk/reward in Internet given the relatively early-stage shift of workloads to the cloud, the transition of traditional retail online, and share gains in its advertising business, the long-term benefits of each we believe the market continues to underestimate for Amazon.”

Clearly he’s not the only one who sees strong investing potential here. it now transpires that Warren Buffett’s Berkshire Hathaway fund has also snapped up Amazon shares. The investing guru told CNBC on May 2 “One of the fellows in the office that manage money … bought some Amazon so it will show up in the 13F” later this month.

Although Buffett wasn’t personally responsible for buying AMZN, he has previously spoken about his great admiration for AMZN CEO Jeff Bezos. And his regret for not buying into Amazon earlier, given the company’s tremendous success in both e-commerce and the cloud. “Yeah, I’ve been a fan, and I’ve been an idiot for not buying” Buffett said to CNBC.

But the recent news suggests that it’s still not too late to join the party. As the Smart Score demonstrates, AMZN boasts a Very Bullish news sentiment. Get the AMZN Stock Research Report.

See what the experts are saying about your stocks now at TipRanks.com. As of this writing, Harriet Lefton did not hold a position in any of the aforementioned securities.