The whole market has been in sell-off mode in August 2019 amid escalating trade tensions, which have triggered a recession warning in the bond market in the form of a 10-2 Year Treasury Yield curve inversion. As the market has sold off, so have shares of blue-chip technology giant IBM (NYSE:IBM). Month-to-date, IBM stock is off more than 10%.

This sell-off in IBM seems overdone. Barring a full-blown recession materializing over the next few months (which I don’t see happening) there are three big reasons why IBM stock is a buy as the stock falls below $130.

First, the fundamentals indicate that IBM below $130 is sufficiently undervalued to warrant material upside over the next few months. Two, the optics surrounding IBM should improve over the next few quarters thanks to the Red Hat acquisition. Three, the technicals imply that IBM is oversold territory, and due for a relief rally soon.

Consequently, while I was optimistic on an IBM turnaround in mid-August, I am bullish on IBM in late August. The bull thesis here just looks too good to pass up on.

IBM Is Sufficiently Undervalued

I wasn’t fully bullish on IBM at $140 because the fundamentals didn’t leave much room for upside at those levels. With the stock below $130, however, I’m fully bullish now, because the fundamentals do leave substantial room for upside over the next few months.

Here’s the math. Without Red Hat, IBM is a flat growth business, with healthy cloud growth offset by legacy revenue declines. With Red Hat – a 15%-plus growth business in the secular growth hybrid cloud market – IBM is a low to mid single-digit revenue growth business. Also, Red Hat operates at 85% gross margins, so the company has the potential to be tremendously additive to margins at scale.

Net net, IBM reasonably projects as a low to mid-single-digit revenue grower over the next few years with upside margin drivers. That combination leads me to believe that IBM can reasonably do about $16 in EPS by fiscal 2025. Based on a 12-times forward multiple – where the stock traded when it was actually reporting positive EPS growth – that equates to a 2024 price target for IBM stock of about $190.

Discounted back by 6% per year (four points below 10% to account for the yield) that implies a 2019 price target of about $144. That price target points to a double-digit upside in IBM stock over the next few months, which in today’s flat market, looks pretty good – especially when you consider there’s a

4%-plus dividend yield here, too.

Improving Optics Will Drive Investor Demand Higher

The second big reason IBM looks good here at $130 is that improving optics over the next few months will drive investor demand higher, providing support for a rally back towards $140-plus price.

The logic here is simple. IBM has forever been a flat revenue grower. That’s about to change. The integration of Red Hat into the operating model will provide a meaningful lift to revenues, both at first and over the long run. Next quarter, revenues are expected to be down by about 2%. The quarter after that, they are expected to rise by almost 2%. The following year, they are expected to rise by more than 4%.

In other words, IBM’s revenue growth trajectory is in the early stages of inflecting from negative to positive. Such inflections normally have a sharply positive impact on investor sentiment, simply because investors like to buy into improving growth narratives.

Consequently, ahead of this negative to positive revenue growth inflection, I reasonably see investors wanting to pile into what has become a really cheap IBM (10-times forward earnings and a 4%-plus yield). This piling in action should give IBM the necessary firepower to shoot above $140 over the next few months.

Technicals Point to Oversold Conditions

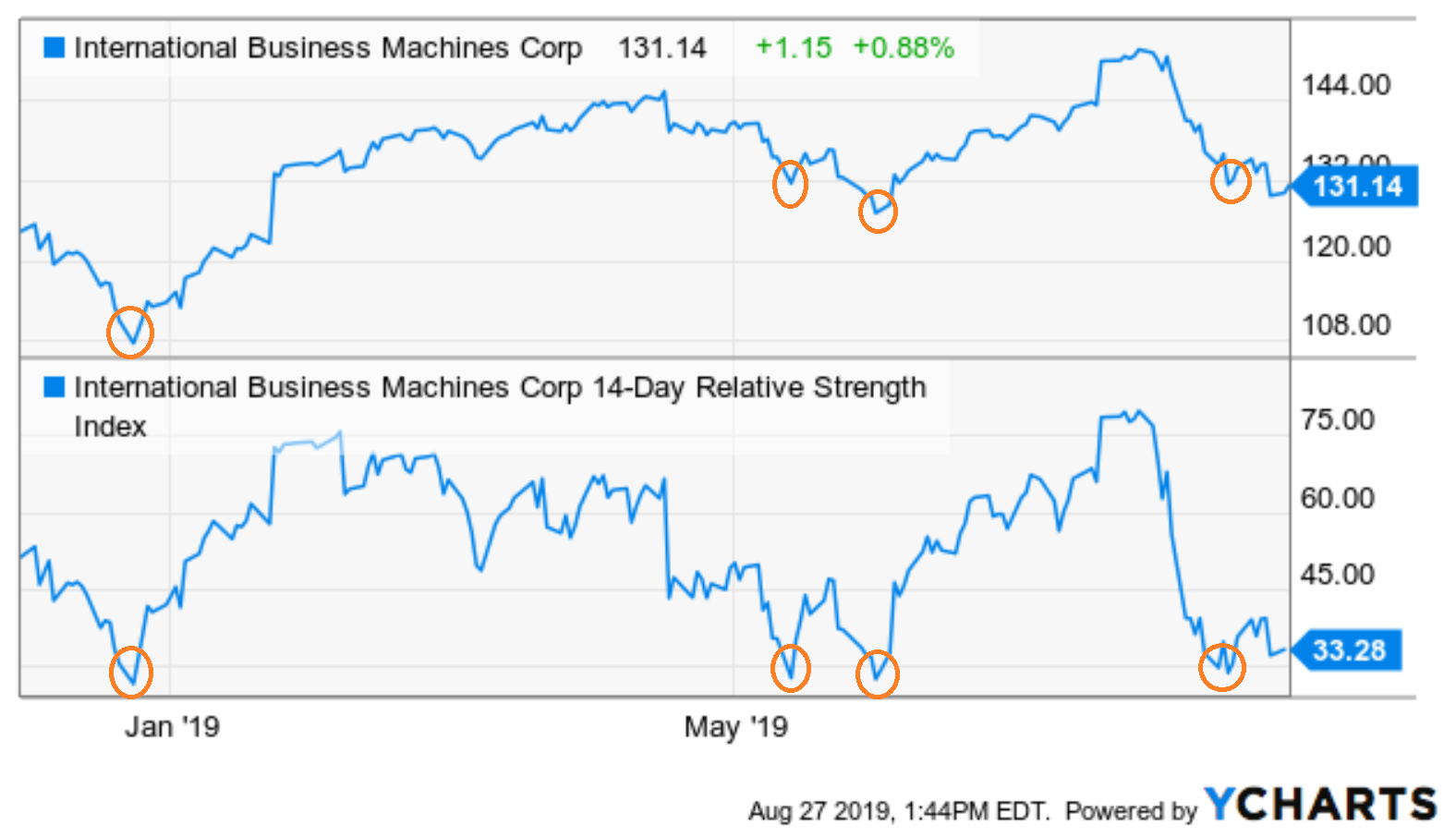

The third big reason to buy IBM here is that the technicals presently point to oversold conditions, and support the idea that IBM is due for a relief rally soon.

Click to Enlarge

Specifically, IBM’s Relative Strength Index has dropped into oversold territory in August. It has done so only a few times since late 2019. Each time it has, IBM stock proceeded to form a near term bottom and bounce back either over the new few days or months.

It appears we are due for a similar relief rally here. Whether or not this turns into a multi-day or multi-month rally remains to be seen. But, I think it will be a multi-month one, given the aforementioned fundamental and optical tailwinds.

Bottom Line on IBM Stock

In the big picture, IBM isn’t a great long term holding. The fundamentals (muted profit growth), optics (snail-like cloud turnaround), and technicals (the stock hasn’t gone anywhere in a long time) simply aren’t good enough to buy and hold IBM for the long haul.

But, IBM does look like a great trade here. The fundamentals (10%-plus undervalued relative to a reasonable 2019 price target), optics (improving revenue growth trend), and technicals (near term oversold) are good enough to warrant buying IBM stock below $130, and selling it on a rally back towards $140-plus prices.

As of this writing, Luke Lango did not hold a position in any of the aforementioned securities.