To say analysts aren’t wildly bullish on Qualcomm (NASDAQ:QCOM) would be a considerable understatement. This community of professional stock handicappers collectively rate QCOM stock closer to a hold than a buy. And, were it not for its high-profile name and the slightly bullish bias most analysts don’t even realize they accommodate, the consensus call could be even less thrilling.

To that end, while the pros may be leaning in a bullish direction in terms of stances on the telecom-tech giant, they’re still not budging in terms of a target. The current consensus price target on Qualcomm stock is $80.41. That’s just above the time of writing price of $78.23. The 64% advance since January’s low hasn’t inspired many analysts to raise the bar as such a move normally would.

This is a case, however, where the analyst community may have talked themselves into overlooking the company’s full potential. They’re also obsessing too much about current headlines. Thus, they can’t see clearly enough to give QCOM stock the bullish assessment it deserves.

Headwinds Galore

There’s no sense in ignoring the 800-pound gorillas in the room.

One of them is the fallout from making Huawei a political pawn. This has strained the working agreements (royalties Huawei pays for IP in particular) it’s had with Qualcomm in the past. And, with or without Huawei as a frenemy, Samsung Electronics (OTCMKTS:SSNLF) is coming on strong. It’s competing aggressively in the low-end and mid-tier 5G handset market, albeit with help from Qualcomm’s tech.

Huawei is also taking aim at a wide swath of the handset market.

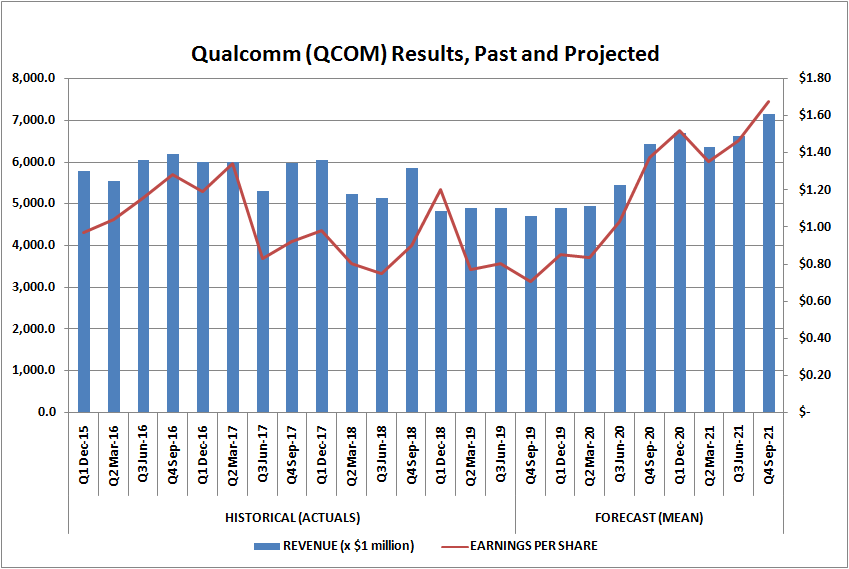

Click to Enlarge

Another gorilla involves a legal headwind. The Federal Trade Commission has made a cogent antitrust argument against Qualcomm. True, the 9th Circuit Court of Appeals has granted a stay that suggests the previous adverse ruling will be reversed. However, the legal battle in and of itself serves as a barometer of the litigation being thrown at the organization.

Never even mind the secondary and even tertiary impact of the ongoing tariff war between China and the U.S. Though it’s apt to end soon, the seeds of distrust and isolationism have already been sewn.

In this light, a hesitant analyst crowd is perfectly understandable.

It’s just that none of these impasses truly, ultimately matter.

Much Working in Favor of Qualcomm Stock

Kudos to Huawei for coming up with a powerful 5G handset chip that powers its Kirin 990 device. At a recent media event, it demonstrated wireless download speeds of 1.7 gigabits per second (Gbps). That’s faster than many wired broadband speeds.

We should also commend Samsung for powering its 5G-capable Exynos 980 with its own processor and chipset. The company has priced the Exynos for the middle of the 5G handset market.

Outside of China, however, Huawei gets little traction. And, as impressive as Samsung’s in-house 5G neural processing unit may be, the bulk of its most notable mobile devices like its Galaxy series still employ Qualcomm-made 5G chipsets.

Qualcomm is also still the high-end market leader for mobile CPUs. Dethroning it, by working around its expansive IP portfolio, won’t be easy. That’s the case even if regulators are effectively forcing it to dial back its aggressive licensing approach.

Essentially, QCOM is too desirable of a platform and has a sizable technology lead.

Largely lost in the discussion, though, is a surprisingly meaningful development: Qualcomm is driving a resurgence in interest toward WiFi, which of course would boost its own business. Last month, the company unveiled a lineup of WiFi 6 chips that could lead an evolution in the near-range connectivity industry.

Though distinctly different from 5G connectivity tech, the two are expected to work in tandem in the future. This may involve seamlessly transferring phone calls from one connection to another. WiFi 6 will also allow large areas to be better covered by connection sources, making it easier for sprawling campuses and factories to manage a fully unified so-called “mesh” network.

Most prospective users don’t even realize they should already be interested in the prospect. Certainly no other connectivity tech provider has been as interested.

Bottom Line for QCOM Stock

The lackluster enthusiasm analysts are demonstrating for QCOM makes a certain amount of sense, but only from a distance. A closer inspection makes clear that this name is a category leader for a reason; several reasons, actually, one of which is a recurring effort to create technologies that make its own wares obsolete.

Click to Enlarge

More than anything though, Qualcomm is a solid buy because it takes a holistic, top-down view of its own space. Telco industry analyst Paolo Pescatore commented earlier this month, “Qualcomm have done a phenomenal job to drive the 5G ecosystem,” adding “It’s going faster than anyone could have ever imagined.”

The WiFi 6 ecosystem may well be next, particularly now that the company has tiptoed into netbook/notebook processor waters that will further blur the lines between WiFi and 5G.

Bottom line? There’s little doubt it’s still the name in the business to beat. Even the analyst community that doesn’t love QCOM stock here expects to see firm sales and earnings growth into the future, more than a year down the road.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about him at his website jamesbrumley.com, or follow him on Twitter, at @jbrumley.