Over the years, Groupon (NASDAQ:GRPN) has attempted to recapture investor enthusiasm as its underlying business continued to decline. Despite best efforts, GRPN stock has been a source of frustration since late 2013. But this year, shares have finally rocketed to life. Not only that, this enthusiasm is coming ahead of the company’s earnings report for the fourth quarter.

Although cheap stocks are usually cheap for a reason, it’s also difficult to ignore the robust bullishness. No matter the worrying dips in revenue growth, Groupon has a fundamental catalyst: everyone loves discounts. As consumers search for retail opportunities on the platform, they have exposure to new products, services and experiences.

But is that enough to have confidence in GRPN stock? From a technical perspective, InvestorPlace contributor Tyler Craig notes that a bullish divergence is developing in the equity’s sentiment indicators. Furthermore, the markets operate in cycles. After several dismal earnings reports, Q4 could be the “ray of hope,” using Craig’s words.

To be frank, I’m not entirely convinced on Groupon’s recovery narrative. Every major metric suggests that the company is losing relevance with the consumer. But that doesn’t necessarily mean that management can’t turn things around.

First, GRPN stock benefits from brand awareness and part of that stems from its brilliant name. By mixing “group” and “coupon,” Groupon perfectly communicates its purpose to the audience.

Second, fears about the coronavirus from China incentivizes Americans to think domestically for travel services. This has obvious synergies for Groupon’s travel deals, along with local deals (its biggest revenue generator).

But for me to get truly comfortable with GRPN stock, I need the discount specialist to improve its trajectory in these three charts.

Active Customer Count Must Move Higher for GRPN Stock

When Groupon first entered the mainstream consciousness, its chart for active customers was a thing of beauty. In Q2 2009, the online discount specialist had 40,000 active users. A year later, this figure jumped to 2.38 million, or a year-over-year lift of 5,850%.

Click to Enlarge

From there, it was a veritable catapult launch to its peak of 53.9 million active customers in Q4 2014. Over this timeframe, YOY growth averaged a remarkable 783.6%.

But starting from Q1 2015 onward, the user trajectory went from flat to decidedly negative. With the online discount space becoming more crowded and with businesses directly offering their own price cuts, Groupon steadily became an unnecessary third wheel. Not surprisingly, YOY active-user growth between Q1 2015 through Q3 2019 dipped to a loss of 2.2%.

For the upcoming Q4 report, I don’t need to see an outrageously bullish number. However, I must see some positive traction. Otherwise, it’s easy to assume that the user base will continue eroding.

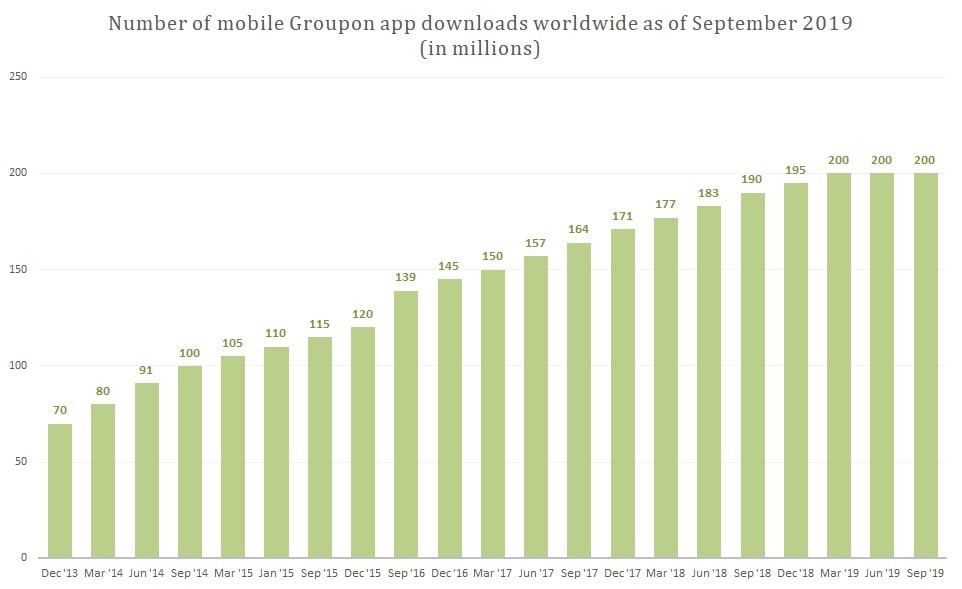

App Downloads Must Also Improve

The days of being tethered to a personal computer are over. Nowadays, if you’re not mobile, you’re not even a thing.

To Groupon’s credit, management has been developing their mobile app since early last decade. As well, the overall growth in app downloads have impressed. From December 2013 through March 2019, downloads have increased nearly 186%.

Click to Enlarge

Unfortunately, this is where the good news ends. Since March of last year, the number of app downloads worldwide has been stagnant at 200 million. In order to justify the company’s international ambitions, this figure must improve, if only by a little. Otherwise, GRPN stock appears unreasonably risky.

Keep in mind that as of now, Groupon’s global revenue peaked in 2016 at just over $3 billion. In 2018, this tally dropped to $2.64 billion. Thus, any boost in user interest and engagement could be huge for Q4.

Gross Billings Looking for a Spark

In Q4 2014, Groupon’s quarterly gross billings peaked at $1.72 billion. A year later, the company almost challenged that level with gross billings of just under $1.71 billion. Since then – as with the company’s other key performance metrics – billings have slipped.

Click to Enlarge

What’s worse, the billings have slipped across Groupon’s three main categories: local deals, travel deals and deals on goods. Of these categories, goods have fallen off the map. Therefore, the other two segments must pick up the slack.

In the year-ago quarter, total gross billings were just under $1.43 billion. To have confidence in GRPN stock, I’d like to see a strong comparative performance in Q4 2019. Otherwise, I’d look for another cheap stock opportunity.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.