When I first discussed Vroom (NASDAQ:VRM) in mid June, I mentioned that the online used car retailer was a relevant business. However, I also cautioned that Vroom stock was debuting at an “awkward time.” Sure, the underlying company offered contactless service, which is a huge bonus during this novel coronavirus pandemic. But we’re also in an economically constrained period, to say the least.

Therefore, even for the consumer, the choice they face is awkward. On one hand, you don’t want to get Covid-19. Despite assurances from right-wing media sources that this is all “fake news,” the health risks seem awfully real. But on the other hand, no one truly feels comfortable about their financial situation. It behooves everyone to get as best a deal wherever possible. Ultimately, I felt the convenience narrative fell short, writing:

“But in exchange for that convenience and for your time saved, VRM charges you a premium. Of course, that’s the potential profitability angle for Vroom stock. In the pre-pandemic era, this made sense. When you consider the collective time spent at work – i.e. commuting and the hours at the office – Americans are increasingly tethered to the cubicle for longer than before.

Thus, Vroom and Carvana (NYSE:CVNA) makes sense, especially if you have a high hourly wage. But because of the transition to remote work, many white-collar workers have much more time on their hands. In this situation, it’s more economically palatable to go analog, haggle a little and get a much better deal.”

To be completely transparent, Vroom stock has moved significantly higher since my skeptical article was published. However, in looking at the details of the company’s second-quarter earnings report, I will reiterate my skepticism.

Poor Q2 Earnings Could Haunt Vroom Stock

On the surface, Vroom’s Q2 results didn’t seem all that bad. As Investors.com contributor Brian Deagon noted, “The online dealer of used autos reported an adjusted loss of 23 cents per share on revenue of $253.1 million. Wall Street expected a loss of 60 cents on revenue of $234.9 million.”

However, management stunk it up when it disclosed its Q3 forecast. “Vroom expects revenue in the range of $268 million to $290 million. The Wall Street estimate calls for $344.6 million, according to FactSet,” wrote Deagon. Because of this bad miss against expectations, Vroom stock quickly bled red ink on the charts.

But in my view, the most important reason why investors should be cautious against Vroom stock is the actions management took in Q2 that could have long-term repercussions. As Vroom CEO Paul Hennessey explained:

“In response to the drop in demand and uncertainty around vehicle pricing early in the pandemic, we chose to de-risk the business by significantly reducing our inventory during the first half of the quarter.”

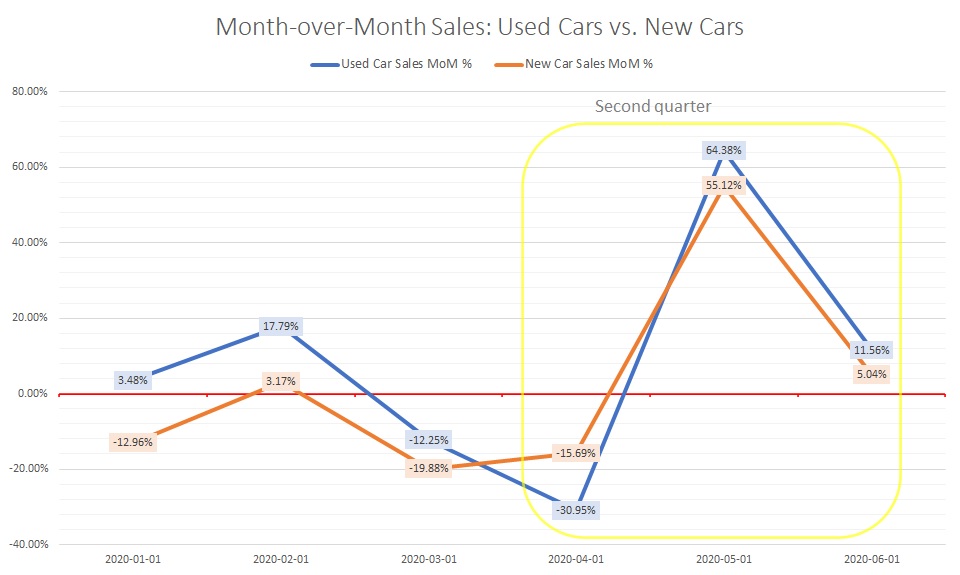

Unfortunately, Vroom de-risked the business at just the wrong time. That’s because in the middle of Q2, car sales (both used and new) skyrocketed. Further, this enormous demand continued into the end of the quarter. Essentially, VRM dumped inventory right when that inventory was about to enjoy a premium.

Click to Enlarge

That said, it’s hard to blame Hennessey; I probably would have done the same. Nevertheless, on a year-over-year basis, Vroom’s sales dropped 3%. In sharp contrast, rival Carvana increased

sales over the same quarter 13.4% YoY.

Eventually, the de-risking is going to haunt VRM stock. The almost irrational bullishness in car sales won’t last forever.

Longer-Term Headwinds Coming Up

Earlier this month, The Wall Street Journal wrote what I considered an alarming article. Despite the pandemic and the economic challenges that it poses, many people rushed out to buy used cars. Now, what was an unlikely bonanza has turned into a nightmare. Used car dealers are now desperate to buy cars — even ones they normally wouldn’t look at — just so they can move some product.

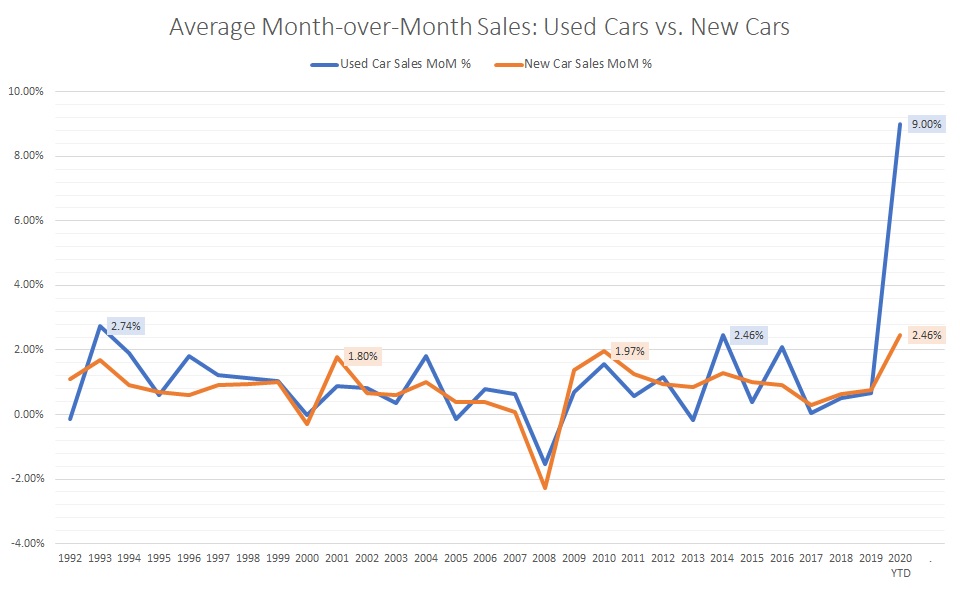

Further, government data on both used and new car sales growth indicates that the WSJ’s assessment is spot on. The month-to-month used car sales growth rate up to June-end of this year averages 9%. If the year were to end then, it would be a record statistic by a long shot.

Click to Enlarge

This enormous demand spike is all-the-more glaring when you compare it to new car sales, with monthly sales growth averaging 2.46%. This too would be a record since data was kept if the year ended in June.

But the key issue for Vroom stock is that this outsized growth in used car sales will not last. As the WSJ has pointed out, used car dealers in late July/early August are desperate for inventory. Therefore, it’s possible that Q3 revenue for Vroom could be even lower than management estimated.

It’s so weird to say this but today, used cars are precious commodities.

Best to Sit on the Sidelines

Eventually, though, this strange phenomenon on the automotive landscape will probably come crashing down. Up until the end of July, you had the federal government supporting millions of workers. That sent a measure of confidence to consumers, driving up car sales.

But without a second relief plan in sight, I see demand falling considerably, as the WSJ article confirmed. That means inventory will again rise for used car dealers. This time, though, the demand won’t be there. And that’s a huge warning sign for Vroom stock.

Like I said earlier, I like the underlying business. But that awkward timing I mentioned? Yeah, it’s a lot more awkward than I initially realized.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.