After months of bullish price action, investors are seeing volatility re-enter the stock market. While that volatility has had an impact on Alibaba (NYSE:BABA), shares are not getting hit as hard as some investors may have thought. In fact, Alibaba stock is holding up pretty well.

From peak to trough, BABA stock fell about 10.8% over a four-day stretch. However, we’re seeing the stock start to hammer out an attractive low near current levels.

Couple that with its solid fundamentals and the current dip is shaping up as a buying opportunity.

Alibaba Dominates Chinese E-Commerce

If Alibaba were an American company, it’s likely it would command a much higher stock price. That’s due to company recognition among investors. Simply put, many American investors are not that familiar with Alibaba and its various business units.

They are also not familiar with the size of its market.

China has a population of roughly 1.4 billion people. That’s more than four times the size of the United States population. The size of China’s middle class population is estimated at more than 400 million people, which is larger than the entire U.S. population (~330 million people). In a few years, this group is forecast to climb toward 550 million people.

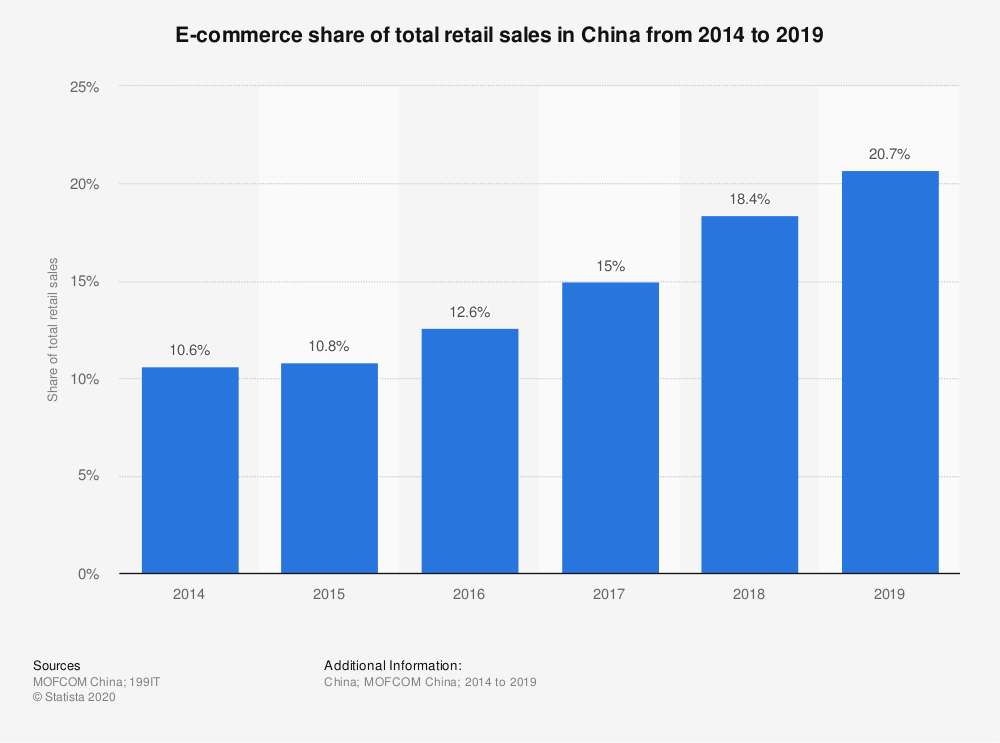

Click to Enlarge

The size of China is simply stunning and with the way its economy continues to grow, it’s no wonder companies like Alibaba are in prime position to benefit.

Check out the data. As you can see on the image, e-commerce continues to make up a larger and larger portion of retail sales. Growth was basically flat from 2014 to 2015, before doubling from 2015 to 2019.

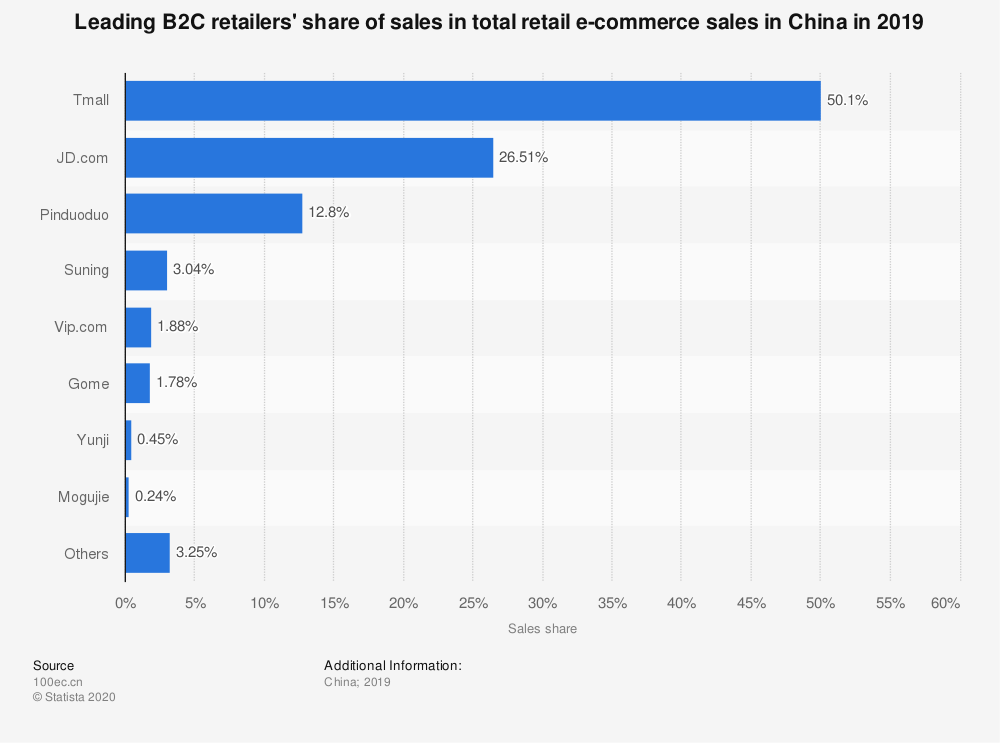

Now, look at the way Alibaba is dominating the Chinese e-commerce market. As you can see on the next graphic, Tmall held a 50% share of business-to-consumer online sales last year.

That’s roughly double the next closest competitor.

Click to Enlarge

In a nutshell, we have a growing economy, a deep middle class and an e-commerce market that continues to make up a larger share of retail sales. Within that e-commerce market, one major player dominates and that’s Alibaba.

Alibaba Has Attractive Fundamentals

The deeper look into Alibaba’s online dominance is always a reassurance for me. However, so is a look at the fundamentals and consensus expectations.

Consensus expectations call for earnings of $9.28 per share this year. If that comes to fruition, it will represent growth of about 23% and leaves Alibaba stock trading at 29 times earnings.

To some investors, that’s an expensive valuation. To me though, that seems reasonable if not downright cheap given that Alibaba is able to churn out such strong growth during a global pandemic. Speaking of that growth, estimates call for revenue to climb 35% this year. For a company of this size, these are impressive numbers.

Next year, analysts expect 25.5% revenue growth and an acceleration up to 25% earnings growth. Looking out this far is obviously not an exact science, but the point is, Alibaba has secular growth powering its business. That should have investors embracing short-term volatility as an opportunity rather than a warning sign.

Bottom Line on Alibaba Stock

Click to Enlarge

With solid growth forecasts and a dominant position in China’s e-commerce market, it’s worth pointing out Alibaba’s other positives. For instance, the company continues to push its business into other growth areas. Digital entertainment is one area, while advertising and cloud computing are other areas.

These units are still dwarfed by Alibaba’s e-commerce presence, but it still represents long-term growth opportunities.

As for other attributes, consider the fact that it’s now dual-listed in the U.S. and Hong Kong. That not only reduces Alibaba’s risk with U.S.-China tensions, but can also help with its valuation. With shares trading elsewhere, it can help elevate demand for the stock.

Let’s not forget another soon-to-be Chinese listed security: Ant Inc.

Alibaba stock owns a one-third stake in Ant, which is seeking a valuation of $200 billion or more. It’s also looking at a potentially record-breaking IPO as it aims to go public in China in September or October.

It’s my belief that Alibaba stock does not get the credit it deserves. Its latest dip is simply an opportunity for investors to get involved, particularly as former resistance at $265 now appears to be acting as support. This conglomerate has too many strengths to ignore for too long.

On the date of publication, neither Matt McCall nor the InvestorPlace Research Staff member primarily responsible for this article held (either directly or indirectly) any positions in the securities mentioned in this article.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now. As of this writing, Matt did not hold a position in any of the aforementioned securities.