On Thursday Sept. 26, Costco Wholesale (NASDAQ:COST) reported earnings. The retailer delivered a sizzling result, but that didn’t translate to success for the stock price. Costco stock ultimately fell about 1.3% on Friday, but was down almost 3.5% at one point.

I could see that type of sell-the-news reaction to the quarter if the broader market was under severe pressure. After all, the market has had some pretty rough days as of late. However, the Nasdaq Composite jumped 2.26% and the S&P 500 rallied 1.6% on the day!

So, why the selloff?

I’m not sure, and to be honest, I don’t really care. What I care about is the quarter, and the quarter was great. In turn, that’s got us taking another look at COST stock.

Lights Out Earnings

Earnings of $3.13 per share coasted past estimates by 30 cents. Revenue of $53.38 billion grew 12.5% year over year and smashed expectations as well.

Making it even more impressive is the fact that Costco provides monthly sales updates for investors. That is a pro and a con in this case, though.

On the one hand, it made it so the quarterly result wasn’t a huge surprise. After all, we have continued to see strong growth in Costco’s business for the last few months. At the same time, even with these updates, consensus expectations were notably low. The analysts short-changed Costco in sales, while earnings came in higher than expected.

Whether that’s what set up Costco stock for a sell-the-news event or not doesn’t really matter. The fact is, this was a great quarter — and it goes beyond the headline results.

Moreover, Costco generated U.S. comp-store sales growth of 13.6%. Internationally, comp-stores sales grew 18.8%, as total company comps jumped 14.1%. Those figures are excluding fuel and forex headwinds. Including them, and each figure was slightly lower but still impressive. Finally, e-commerce sales growth exploded more than 90% in the quarter.

Additionally, there’s also this: “This year’s fourth quarter was negatively impacted by incremental expense related to COVID-19 premium wages and sanitation costs of $281 million pretax ($0.47 per diluted share).”

Costco Is an Anointed Retailer

Was the quarter perfect? No. But this stock should be up, not down on the results. A top- and bottom-line beat, along with almost triple-digit e-commerce growth, and enviable comp-store sales should trigger buy orders, not sell orders.

But alas, that is not the reaction and in reality, that is great for long-term investors. They get clarity on the business and a discount on the stock. That sounds like a win to me because at the end of the day, Costco is an anointed retailer.

It’s one of several retailers that are seeing strong growth amid the pandemic. There are other big-box retailers and home improvement stores that are doing well too, but it’s not a zero-sum game. Just because one of them does well doesn’t mean Costco isn’t. This group is dominating in a post-coronavirus world, and I don’t expect that to stop anytime soon.

Costco has a unique business model where customers with larger orders (particularly those with families) save a ton of money. In turn, that generates demand and that demand is translated to growth.

That said, analysts expect a steady ascent in revenue for the new fiscal year, calling for about 6% growth. On the earnings front, consensus estimates call for 7.8% growth. For both metrics, analysts expect an acceleration in growth for fiscal 2022 (next year) to 7.5% and 10.5%, respectively.

The Bottom Line on Costco Stock

Click to Enlarge

When a company reports earnings, investors can’t fight what the market wants to do. Sometimes the reaction is the start of something big, and sometimes it’s a mistake. If the broader market takes a tumble, COST stock will likely struggle too. However, if the market is stable (or even rallies) then Costco should do well.

That’s because this was a good quarter. However, let’s look at the two reasons why shares are likely under pressure. The event set up as a sell-the-news reaction due to the monthly sales updates and Covid-19 expenses continue to hit the bottom line.

In both cases, though, results continue to top expectations. I’m sorry, but for me that makes these selloffs a short-term event and an opportunity.

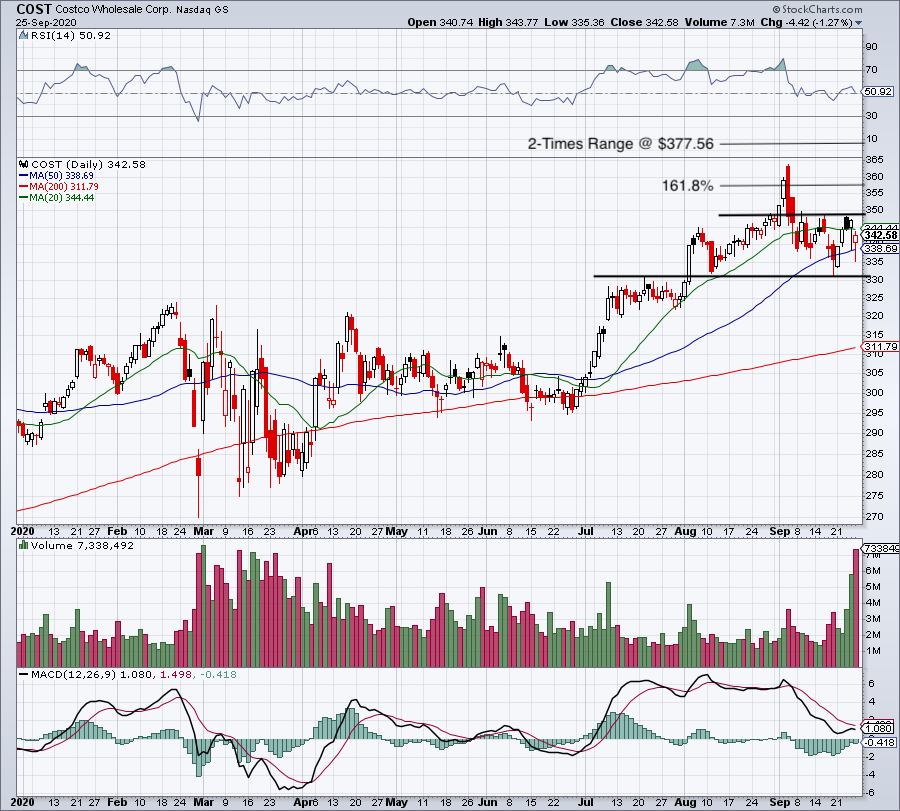

On the dip, Costco stock held the 50-day moving average, which is healthy price action. Now I want to see shares rotate higher and take out resistance near $348. Above opens the door to the 161.8% extension near $358, the all-time high up near $364 and eventually, the two-times range extension at $377.56.

If Costco loses the 50-day moving average, however, it puts the $330 area in play. Above that mark and shares are still healthy, in my opinion. In fact, even a dip to the 200-day moving average represents more opportunity than risk for long-term investors.

On the date of publication, neither Matt McCall nor the InvestorPlace Research Staff member primarily responsible for this article held (either directly or indirectly) any positions in the securities mentioned in this article.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now.