Ford Motor Company (NYSE:F) is one of the cheapest stocks in the S&P 500. But is this icon of American automaking a buying opportunity or is F stock a value trap destined to get ever cheaper in the road to eventual bankruptcy?

Let’s take a look.

If you’ve been waiting for a turnaround in Ford stock, you truly have the patience of a saint. The past decade hasn’t been kind to American automakers, but it’s been particularly brutal for Ford.

Ford stock is down by nearly two thirds from its old 2011 highs.

And keep in mind, these declines came during one of the bull markets in history of American capitalism. Over that same time period, the S&P 500 has more than tripled in value.

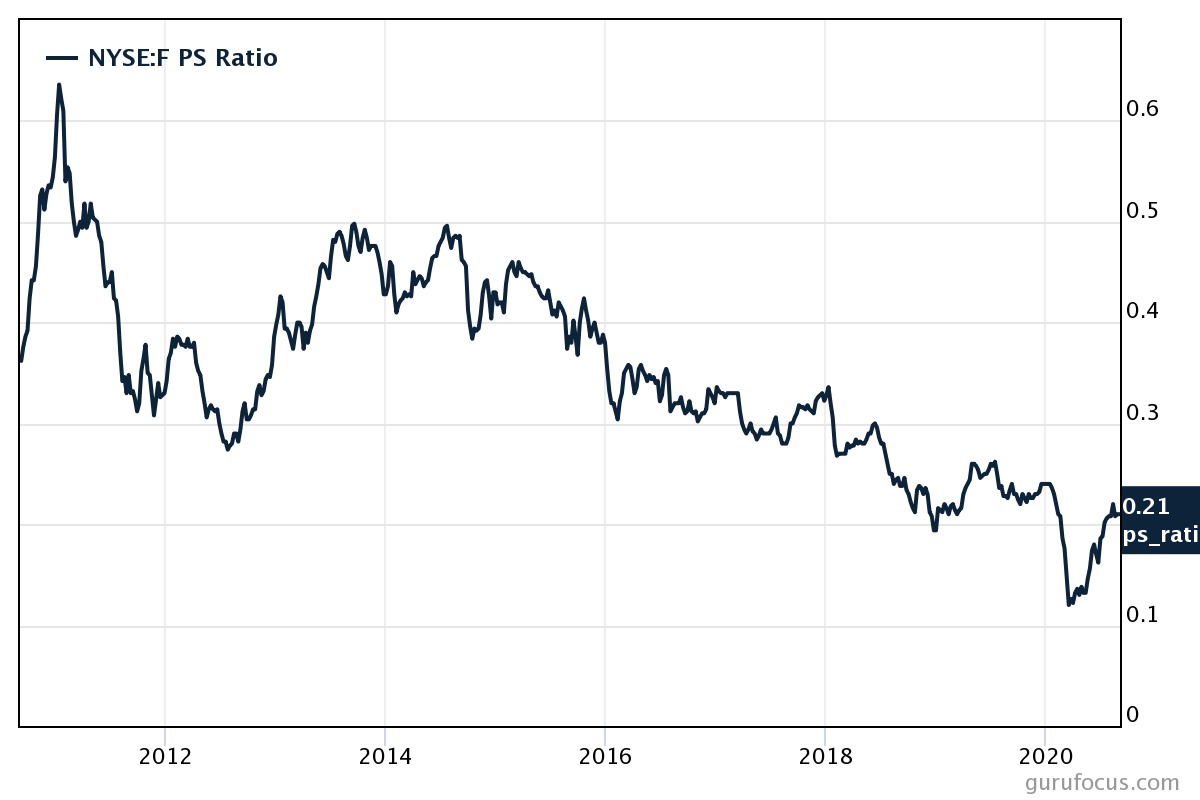

After a decade of inexorable declines, Ford stock looks cheap, at least on the surface.

The stock trades at just 0.21 times sales. To put that in perspective, the S&P 500 trades at 2.5 times sales. By this metric, Ford is 92% cheaper than the stock market as a whole.

I’m not just cherry picking. By nearly every other common valuation metric, Ford stock would seem to be cheap. It doesn’t have a calculable price-earnings ratio due to the company currently operating at a loss, but it trades at a cyclically-adjusted price-earnings ratio (“CAPE”) of 3.9 and a price-book ratio of just 0.97.

These are extraordinarily cheap metrics for a company of any size or name recognition.

Ford Stock: What’s the Catch?

But while Ford is cheap, there’s no obvious catalyst to make Mr. Market revalue it. The auto industry was due for a cyclical slowdown even before the novel coronavirus pandemic struck. Now, with unemployment still near generational highs and small businesses across the country utterly wrecked by months of social distancing requirements, the downturn in auto sales looks to be deep and long lasting.

That would be bad news for any company. But it’s potentially devastating for an over-leveraged company in a mature and brutally competitive industry with far too many marginal players.

As a quick and dirty gauge of Ford’s safety, let’s take a look at its Altman Z-Score, a metric developed in 1967 by New York University Professor Edward Altman to gauge bankruptcy risk. By Altman’s calculations, the score is over 80% accurate in determining whether a company will ultimately go bankrupt.

The Z-Score is based on five financial ratios:

- working capital/total assets

- retained earnings/total assets

- EBIT/total assets

- market value of equity/total liabilities

- sales/total assets

Ford scores poorly on all of these metrics because it is an asset-heavy business with large debts and a dearth of profitability. I’ll spare you the math of how the score is calculated, but a score over 3 means the company is healthy, and a score less than 1.8 means it is likely on the road to bankruptcy.

Well, in looking at Ford stock’s Altman Z-Score, the results aren’t pretty. At no point in the past 10 years has the score been higher than 1.8. Today, the reading is just 0.77 and has been sliding all year.

Now, we shouldn’t put undue emphasis on a single metric like this.

But the takeaway is clear.

The Bottom Line on F Stock

Ford is not a healthy company. In fact, it is a very sick company that has managed to limp along because the economy, up until March, had been healthy and interest rates low.

Ford’s ultimate fate may depend on its ability to secure a governmental bailout package. But that’s not a game you should play with your nest egg. For now, F stock is best avoided.

On the date of publication, Charles Sizemore did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Charles Lewis Sizemore, CFA is the principal of Sizemore Capital Management, a registered investment adviser based in Dallas, Texas.