In principle, China Automotive Systems (NASDAQ:CAAS) seems like a viable long-term investment. As our own Louis Navellier pointed out, the company is one of the leading producers of power steering components for the automotive market, particularly for electric vehicles. Naturally, that piqued interest among speculators, given the platform’s explosive popularity. As a result, CAAS stock skyrocketed.

At its peak this year, CAAS hit $10.50 on Nov. 30. However, at time of writing, CAAS stock has lost more than 34% of market value. On one hand, this may be interpreted as a sign that not all is well. But on the other hand, China is the world’s biggest automotive market, registering more than 21 million new cars last year. In contrast, the U.S. only registered just under 17 million new cars.

Therefore, anything automotive-related, whether combustion or electric, must go through China. And that puts CAAS stock in the driver’s seat. As well, it provides confidence that shares today represent a potentially profitable discount.

Further, to Navellier’s point, the Chinese EV sector recently boomed. For example, according to China Automotive’s press release, “Sales of Chinese EVs approximately doubled year-over-year to 144,000 units in the month of October 2020. With this rapid growth of EVs occurring in China, the outlook is for booming growth as the Chinese government has set an EV car target of 25% of all new cars by 2025.”

Better yet, CAAS stock is agnostic to consumer preferences. So long as consumers want EVs, the underlying company doesn’t have to make adjustments. It’s all potential sales opportunities.

Therefore, a key risk factor is taken out of the EV equation. On paper, at least, buying CAAS stock is akin to buying something like Sociedad Quimica y Minera de Chile (NYSE:SQM) for anticipation of lithium demand, not speculation on which specific EV maker will win out.

Still, is there more to this than meets the eye?

Skepticism Is the Operative Word for CAAS Stock

Based on the blistering rally that CAAS stock recently enjoyed, being cautious toward CAAS could draw quick accusations of being a soy boy. Real alphas take risks and to the victor goes the spoils, or something to that effect.

Far be it from me to deny anybody an opportunity to make money. But I also care about not losing money. Analyzing the fundamentals that impact CAAS, I believe skepticism is the better approach here.

First, you have so many EV makers, especially in China. And according to Scott Kennedy from the Center for Strategic and International studies, “The vast majority [of electric car makers] will not survive

. But how long they survive and whether industry consolidation occurs through lots of mergers or bankruptcies will depend on the willingness of the government.”

Further, Kennedy states, “Chinese auto and battery technology is still not world-class. CATL and BYD are strong battery makers, but they are still somewhat behind technologically from their South Korean and Japanese counterparts. And Chinese automakers are still second-class producers even in their own country and they have barely any sales outside China.”

It’s at least something to think about before you bet too heavily on CAAS stock.

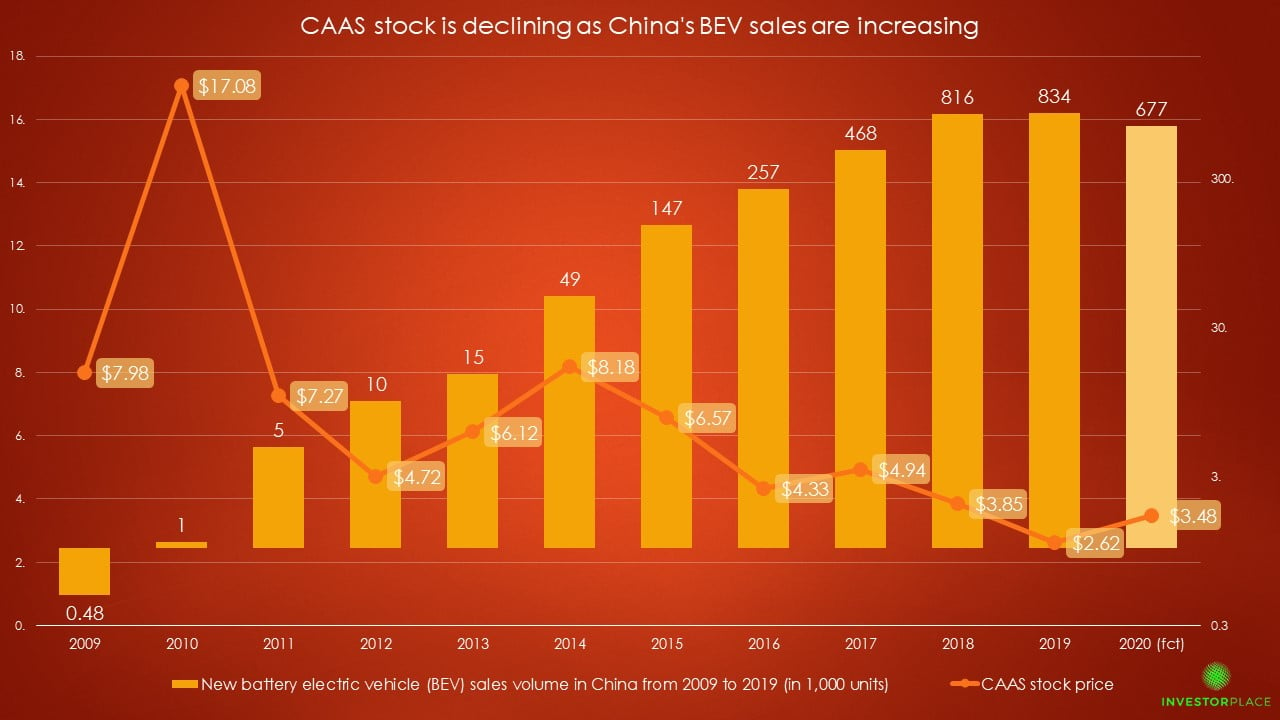

Click to Enlarge

But the biggest headwind for CAAS stock is that there doesn’t seem to be any relationship between the share price and the sharply rising demand for EVs in China. Now, earlier on, some logic did exist. Between 2012 and 2014, Chinese battery electric vehicle sales increased by nearly 15 times. During the same period, CAAS increased 73%.

However, from 2014 through 2019, when Chinese BEV sales increased 17x, China Automotive Systems declined – yes, declined! – 68%. How does that make sense?

Therefore, I believe it when Gurufocus.com declares CAAS as “significantly overvalued.” When the underlying industry is expanding by double-digit multiples, shares should be rising, not falling.

Perhaps Wait for More Consumer Data

Before you label me a hater, if you’re still interested in CAAS stock, I’d wait and take a look at BEV sales for 2020. I’m assuming due to the impact of the novel coronavirus that Chinese BEV sales this year will be fewer than 700,000 units.

But I could be wrong. Dead wrong. And it wouldn’t be the first time, nor the last I’m afraid. So, if you’re not sure how to approach China Automotive, wait for the finalized data. If pent-up demand overcomes the novel coronavirus crisis and beats out 2019 BEV sales, we could be talking something here.

However, for everyone else, I think a cautious approach – or even outright avoidance – is best. Again, EV component manufacturers should rise in valuation as the industry exponentially expands. But we’re seeing a negative correlation, for crying out loud! That to me signals rough waters ahead.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.