TransEnterix (NYSEAMERICAN:TRXC) now has plenty of cash to survive well into 2024, which will allow the laparoscopy robotics company to eventually produce revenue. As a result, TRXC stock has a chance of eventually doing quite well for itself and investors.

Some of TransEnterix’s competitors have massive market values, giving hope to owners of TRXC stock that it could reach that level. For example, Intuitive Surgical (NASDAQ:ISRG) now has an $89 billion market capitalization. Based on my estimate of TransEnterix’s shares outstanding (about 211.76 million) TRXC stock has a market cap of $885 million, as of Feb. 8.

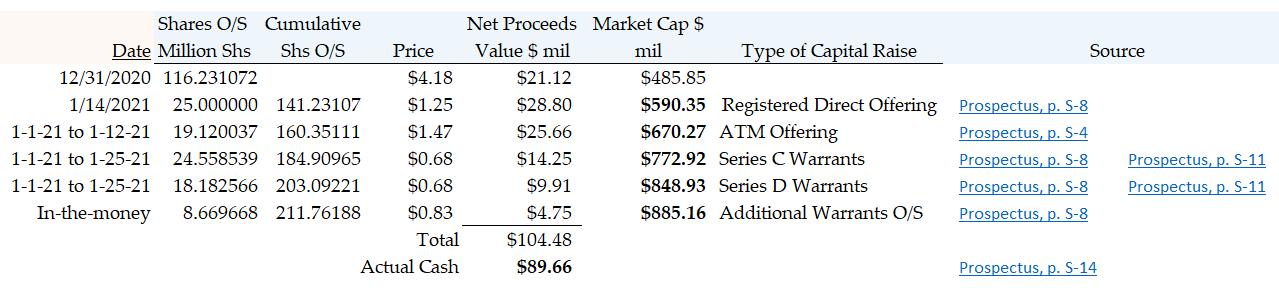

Cash, Cash Flow, and Market Cap

I estimate, after reviewing the company’s latest prospectus supplement as of Jan. 28 that TransEnterix has raised approximately $90 million ($89.66 million) after expenses. That means that its cash at that point was about 10.1% of its previously mentioned $885 million market capitalization.

The company has raised this cash through a series of capital raises, and warrant exercises. Most of these are detailed on pages S-4, S-8, and S-11 of the prospectus. This assumes all the in-the-money warrants exercise their option to buy shares at their exercise price.

Click to Enlarge

I have prepared a table above, which you can click on to see more in-depth, of my best guess of the capital raises and total shares outstanding.

Hopefully, this will be helpful for those interested in TRXC stock. Moreover, on page S-14 of the prospectus, the company says that after this filing it will have $89.66 million. In addition, on page S-4, TransEnterix says this:

“We believe that cash on hand, proceeds from the Registered Direct Offering, the ATM Offering (prior to its termination) and the Series C Warrant and Series D Warrant exercises, as well as the proceeds from this offering will be sufficient to fund our operations into 2024.”

This assures investors that TRXC stock is not going to go to zero. But whether the company can get profitable will depend on how well it can commercialize its medical devices.

For example, as of Sept. 30, TransEnterix has made negative cash flow from operations (CFFO) in its first nine months in 2020. Page 5 of its latest 10-Q shows that CFFO was negative $33.91 million. Therefore on average, the company burnt through $11.3 million each quarter.

With $90 million in the bank, TransEnterix can last at least eight quarters at this rate. However, the truth is the company is likely to continue to raise capital, especially as its stock price rises. Therefore I don’t think that TransEnterix will run out of cash to fund its operations.

What To Do With TRXC Stock

The hard fact is that TransEnterix is in only 11 hospitals right now that have performed more than 100 operations per year with their micro-robotic laparoscopic medical devices. This is what the company said on page S-2 of their latest prospectus update.

They are approved in a number of countries to use their devices. But in the U.S. they have submitted an application for 510(k) approval for an expanded General Surgery indication for use for the Senhance Surgical System to the FDA. This is their main product.

Until the company can expand the number of hospitals and surgical procedures with their devices, revenue will not be able to begin. So far the company is not taking in revenue, but instead is using its devices in various studies.

However, I suspect that as the stock price rises, along with expectations from investors, the company will move to begin commercializing its devices sooner. At that point, expect to see a major jump in the outlook for TransEnterix as well as its stock. However, there is no guarantee that will happen anytime soon.

Until then, most investors are betting on the come with TRXC stock, hoping that its ability to produce revenue and profits arrives sooner than later.

On the date of publication, Mark R. Hake does not hold a long or short position in any of the stocks in this article.

Mark Hake writes about personal finance on mrhake.medium.com and runs the Total Yield Value Guide which you can review here.