Shares of the short-term rental marketplace Airbnb (NASDAQ:ABNB) have held up nicely after its blockbuster IPO. ABNB stock was up a healthy 23% since its IPO back in December.

It now trades at a parabolic valuation which is completely disconnected from its financials. Therefore, it’s tough to get excited about ABNB stock at this time.

The company recently reported its fourth-quarter results, where its net loss widened to $3.89 billion from a $352 billion loss in the same period last year. Additionally, revenues fell 22% year-over-year to $859 million, and gross bookings value also took a major hit, down 31% year-over-year in the quarter.

More importantly, the management remarked on the lack of growth trends in 2021.

Airbnb’s business model has depth and has plenty of room for more future growth. Regardless of that notion, it trades at unfathomable levels, which limits its attractiveness at this time.

Tightening Regulations

Tightening regulations could potentially constrain Airbnb’s business model. Every city has its own rules and regulations with regards to short-term rentals. Additionally, the hotel industry has been lobbying for the authorities to tighten the screws on Airbnb in line with other short-term lodging providers.

As more cities and states in the U.S. impose stricter regulations, we could see Airbnb losing out on a substantial share of revenues.

For example, Airbnb lost its largest market in 2018 when New York banned the company. A massive amount of revenue has to pour in from illegal listings from the New York City area.

However, with the new laws in place, the NYC hosts could face fines up to $2500 per day and $7500 per illegal listing. Such fines will most certainly deter hosts to list on the platform illegally.

Additionally, Atlantic city recently passed legislation directly impacting short-term rentals.

These laws primarily cover licensing fees and other regulatory requirements. Moreover,

San Francisco appears to have followed a similar model to New York.

Rentals from the platform are only allowed if the hosts are full-time residents, are registered with the city and the rentals are capped at 90 days. Santa Monica, Calif. has also instituted some strict regulations that essentially wiped away roughly 80% of Airbnb listings in the area.

However, the restrictions are not only limited to the U.S. You have major cities in Europe, such as Paris, Barcelona, Berlin, Amsterdam and others, that have instituted some significant constraints on the workings of Airbnb.

Lofty Valuation

Click to Enlarge

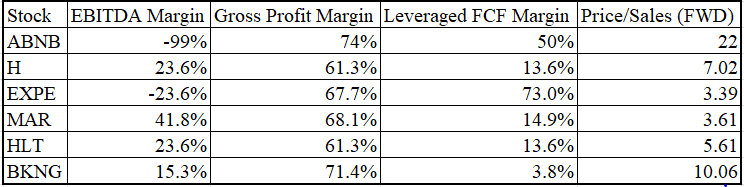

Perhaps the most significant point against buying ABNB stock is its valuation. We can see the profitability and price to sales ratio for ABNB and its peers from the table. Gross margins have been impressive for ABNB.

A large part of its healthy revenue growth in the past several years has consistently outperformed the market. Additionally, its leveraged free cash flow margins are also impressive and second only to Expedia (NASDAQ:EXPE).

However, we can see that its EBITDA margins are at a deplorable negative 99%, which is head and shoulders above its competition. At the same time, its forward price to sales ratio is 22 times, which is nothing short of extraordinary.

There is a high dispersion among analyst estimates for its ABNB stock’s price. The lowest estimate for the stock is at $130, which is roughly 29% lower than its current price.

Similarly, its highest price estimate is $240, which is 31% higher than its current price. The stock is highly volatile and one which is significantly overvalued at this time.

Final Word on ABNB Stock

ABNB stock has held its own after a rollicking IPO back in December. The problem, though, is that it has flown too high and is at a point where it’s significantly overbought.

Additionally, the weaknesses in its business model, particularly regarding its regulatory challenges, are becoming more apparent than ever.

The lack of growth trends this year is another downer that further widens its bear case. Therefore, it’s best to avoid ABNB stock for now.

On the date of publication, Muslim Farooque did not have (either directly or indirectly) any positions in the securities mentioned in this article.