The Trade Desk (NASDAQ:TTD) has become a fast-growing cash flow machine in its digital advertising business. The company is now deeply involved with “connected TV” (CTV) and audio, where people subscribe to their media channels and watch and listen to CTV ads. I estimate that TTD stock is now worth at least 28% more at $98.13, up from $76.62 as of July 2.

Click to Enlarge

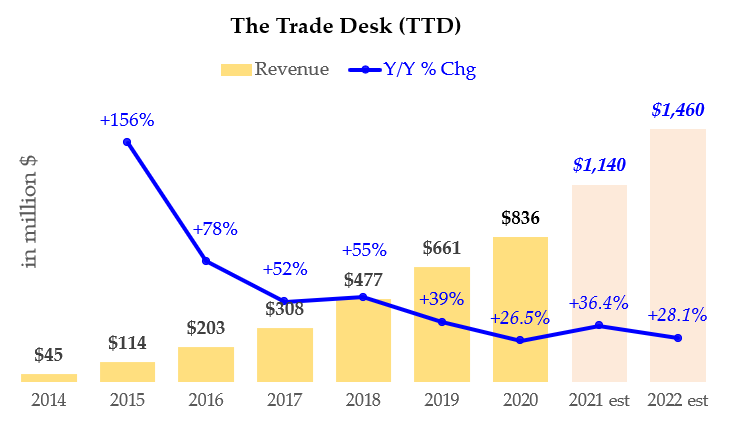

The Trade Desk makes money by charging its clients, mostly ad agencies, a platform fee based on a percentage of a client’s total spend on digital advertising. It also provides data analytics and services. As you can see from the chart on the right, The Trade Desk has been growing quite significantly.

Sales were up 26.5% last year and analysts foresee revenue jumping 36.4% this year to $1.14 billion, according to Seeking Alpha. Revenue is also projected to rise 28% to $1.46 billion in 2022. This is useful since we can also estimate its FCF and implied value from this.

Estimating FCF for The Trade Desk

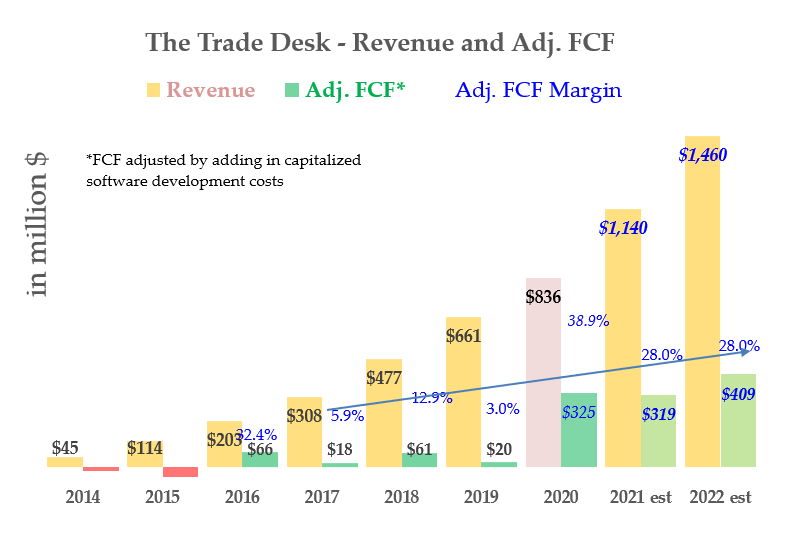

It turns out that The Trade Desk is also now very profitable. For example, in 2020 the company generated $325 million in adjusted free cash flow (FCF). The adjustment is as follows. In addition to subtracting capex spending from Cash Flow from Operations (CFFO), we also subtract capitalized software development costs. These are actual software expenses that were not expensed through the income statement. I lower the FCF figure by these costs since they are sunk cash costs that reduce cash flow.

Nevertheless, the FCF margin that The Trade Desk produces is quite high. For example, the $325 million in adj. FCF represented 39% of its revenue last year. Based on this I made some assumptions and projected out adj. FCF for 2021 and 2022. You can see this in the chart below.

Click to Enlarge

For example, just to be conservative I used a 28% FCF margin for both 2021 and 2022. This is lower than the 39% FCF margin last year, but since sales will be higher, the FCF figure will also be higher by 2022. Why did I use a 28% FCF margin? This was the FCF margin from Q1 when TDD made $60.9 million in adj. FCF on $220 million in sales (i.e., $60.9 million/$219.8 million = 27.7%).

As you can see in the chart above, the 2022 forecast adj. FCF is $409 million. This is 25.8% over the $325 million in adj. FCF generated in 2020. Keep in mind that my forecast is very conservative. This is much lower than the adj. FCF figure will be if the 2022 FCF margin is higher than 28%. This is especially so if the 2022 estimate is closer to the 39% FCF margin from 2020.

What TTD Stock Is Worth

Next, to find a valuation target for TTD stock, I use an FCF yield metric. For example, if we take the adj. FCF estimate for 2021 of $319.2 million and divide it by TTD’s market capitalization of $36.456 billion, the FCF yield today is 0.88%. Therefore, applying this FCF yield to 2022, we get a market value estimate of $46.689 billion (i.e., $481.8 million / 0.88%).

This implies that the true value of The Trade Desk is 28.1% above the market cap today of $36.456 billion. As a result, the target value for TTD stock is $98.13 per share (i.e., 1.281 x $76.62 price today). In other words, based on our assessment of its FCF generating ability, and using a 0.88% FCF yield, TTD stock is worth 28% more.

That is a reasonable return for most investors. If the adj. FCF comes in higher and if we use a similar FCF yield, TTD stock could spike even more than my estimate.

On the date of publication, Mark R. Hake did not hold a position in any security mentioned in the article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Mark Hake writes about personal finance on mrhake.medium.com and runs the Total Yield Value Guide which you can review here.