Editor’s note: This column is part of InvestorPlace.com’s Best Stocks for 2021 contest. Charles Sizemore’s pick for the contest is Enterprise Products Partners (NYSE:EPD) stock.

With one quarter left in 2021, Enterprise Products Partners (NYSE:EPD) stock is still in the race.

At this point, EPD is in second place of the InvestorPlace Best Stocks Contest for 2021 with a total return of 18% year-to-date. That’s still well within striking distance of the top spot, but Enterprise Products Partners still has work to do.

So, in order for EPD stock to win this time around, we’ll need to see a pretty significant pop in the next three months. We’ll see if that happens. Ultimately, the market will do what it does, and we can’t control that.

But we can allocate our capital where we see the best bargains. And Enterprise Products remains an exceptionally cheap income-paying workhorse in a market where value is hard to come by.

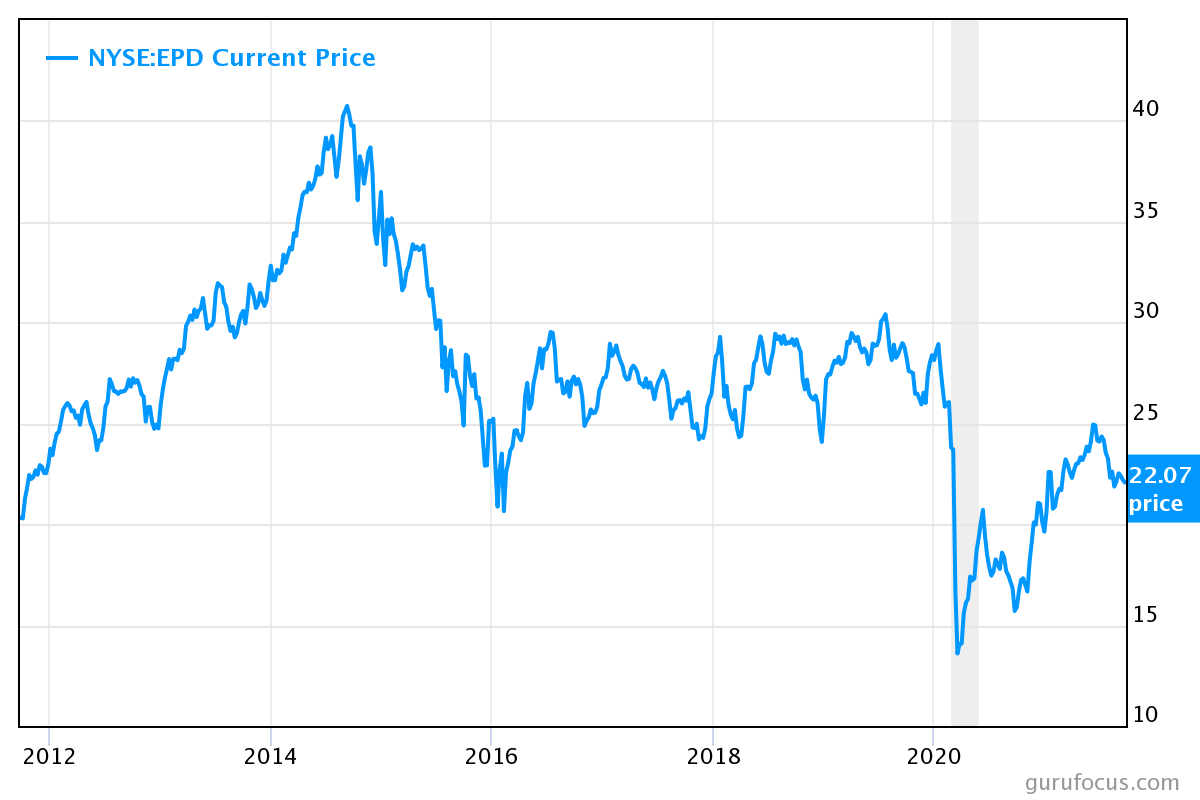

Click to Enlarge

EPD Stock at a Glance

Enterprise Products’ price has dipped since our last quarterly update. But it’s important to consider this move within the context of the past year and a half. After trading in a tight range for several years, the EPD stock price took a swan dive during the early stages of the pandemic. Apart from the typical volatility that rocked the entire market, EPD stock got sucked into that particular nightmare that plagued the energy sector. Remember when crude oil prices briefly went negative last year?

Overall, Enterprise Products and its peers are first and foremost infrastructure companies. They

move energy. They don’t produce it. Still, the fear last year was that a wave of bankruptcies in the energy patch would lead to broken contracts with the midstream pipeline operators like EPD.

The worst-case scenario never quite played out, and EPD stock enjoyed a spectacular rally. Some of the weakness we’ve seen of late is profit taking and sector rotation.

Still, the investors taking profits in EPD may wish they had stuck around a little longer. The shares still trade well-below their trading range of 2017-2019, and they weren’t exactly expensive even then. Currently, the shares trade at levels first seen in 2011 — a decade ago.

You know Warren Buffett’s old saying: Price is what you pay, value is what you get. Thus, let’s compare EPD’s enterprise value (EV; the value of its combined equity and debt) to its earnings before interest, taxes, depreciation and amortization (EBITDA). Master limited partnerships have notoriously quirky accounting that make traditional earnings or sales-based valuations tricky. But the EV/EBITDA ratio strips out those quirks and gives us a decent view of the companies valuation.

At current prices, EPD trades at a multiple of 10.38, That’s obviously more expensive than during the pits of the pandemic. But it’s still very cheap by the standards of the past decade. Investors have largely fled the broader energy sector, leaving us with valuations I would have considered impossible even a few years ago.

Furthermore, if you’re familiar with Enterprise Products, then you know the stock is first and foremost an income stock. And while I expect to see major capital gains from current levels, most investors buying shares do so because they are attracted to the high and consistently growing distributions.

Well, at its current price, EPD yields a whopping 8.26%, That’s lower than the yields we saw during the COVID panic and during the worst months of the 2008 meltdown. But if you strip away those two crisis moments, the current yield is the highest we’ve seen in 20 years. Meanwhile, the company continues to consistently raise its payout.

So, will EPD take the crown in this year’s Best Stocks contest? That remains to be seen. Regardless, EPD is a solid income-paying value stock priced to deliver outstanding returns in the years ahead.

On the date of publication, Charles Sizemore has a long position in EPD. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Charles Sizemore, CFA is the principal of Sizemore Capital Management, a registered investment adviser based in Dallas, Texas specializing in income and retirement strategies.