|

September was painful. And if you’re like many investors, you’re looking at your portfolio, wondering if it needs pruning. After all, when markets turn south, mediocre stocks that were riding the coattails of a bullish market are often exposed for the imposters they are – because they drop fast. So, what’s a powerful-yet-simple approach to portfolio maintenance? That’s what our macro specialist and the editor behind Investment Report, Eric Fry, details today. As he writes below, “You don’t want to pursue investment success by betting on flukes. Instead, you want to stack the odds in your favor as much as possible.” If September weakness has revealed you have some “flukes” in your portfolio, this is the Digest for you. I’ll let Eric take it from here. Have a good weekend, Jeff Remsburg |

Does Your Portfolio “Spark Joy”?

Eric Fry

Marie Kondo, the “decluttering” guru, has made millions of dollars by devising and popularizing a common-sense method for purging a home of unnecessary and unwanted “stuff.”

Kondo’s decluttering strategy – called the KonMari method – follows six basic steps. It begins with an explicit commitment to tidying up and features one essential question: Do the items you wish to keep “spark joy”?

Those items that do spark joy should remain; those that don’t should go away. And this method isn’t just limited to the dusty, unread books in your collection, the waffle maker you haven’t used since you got married, or the contents of your attic…

Investors could stand to enrich themselves as well, simply by applying some of Kondo’s cleanup tactics to our portfolios.

Even some of the most seasoned and savvy investors fail to tidy up their portfolios as they should. That’s because tidying up a portfolio requires an explicit commitment to do so… along with a dispassionate analysis that asks a version of the question, “Does this item spark joy?”

Not every worthwhile investment will “spark joy,” of course, but it should spark some sort of powerful and obvious positive reaction.

Remember, like the KonMari method, your goal is to identify the items you wish to keep, not the ones you wish to discard. The discard pile is simply the by-product of what you wish to keep.

Spark “Yes!”

If you examine each stock in your portfolio and ask yourself honestly, “Will this stock make me rich?” or “Will this stock be a 10-bagger?”, the answer should always be a resounding, “Yes!”

But if the answer is “No,” the stock doesn’t belong in your portfolio, even if it’s a solid blue chip or a popular household name.

Those sorts of investments may be fine. But very few investors set their sights on just “fine,” because in the investment world, “fine” is synonymous with “opportunity cost.”

That’s certainly not fine in my book.

“Opportunity cost” is a term of regret that ruefully refers back to “what could have been”; it describes the consequences of making a misguided or suboptimal choice between competing possibilities.

Analyzing opportunity cost can and should be part of an investment discipline that insists on buying extraordinary investments, rather than ordinary or “fine” ones.

Obviously, none of us knows exactly what the future will hold. Therefore, analyzing opportunity cost is an inexact science. In fact, it’s an educated guess.

Based on decades of stock market history, we know a few key details about what produces investment success over time. For example, we know that:

- Fast-growing companies tend to produce better investment results than slow-growing ones…

- Cash-rich companies tend to produce better investment results than heavily indebted ones…

- And companies that possess a formidable “moat,” as Warren Buffett calls it, tend to produce better investment results than companies without any special competitive advantage.

So, when we examine the stocks in our portfolios, we should favor those that possess one or more of these winning traits.

Now, some stocks that possess serious flaws will buck the odds and perform well anyway. Sometimes heavily indebted, slow-growing companies find a way to reverse their declining fortunes and become major successes. But companies like that are rare outliers.

You don’t want to pursue investment success by betting on flukes. Instead, you want to stack the odds in your favor as much as possible.

And I’ve discovered a way to do that…

The “Portfolio Purge” Formula

Calculate the size of a company’s net debt, and then divide that figure by the company’s annual revenue… to produce a simple ratio:

[Net Debt Divided by Trailing 12-Month Revenues]

Generally speaking, the higher the ratio, the worse a stock is likely to perform over the following five years. The lower the ratio, the better a stock is likely to perform over the following five years.

That’s it. That’s the entire process.

I routinely use this simple test to identify potential investments. (Obviously, my research does not end there.) But once I identify a potential investment, I qualify that stock by conducting additional targeted qualitative and quantitative research.

Some investment candidates make the cut. Most don’t.

But here’s the crazy thing: This simple two-part test, all by itself and without any additional research, can produce impressive investment results.

As you know, investors are always compounding something – either successes… or mistakes… or boredom. That’s why intelligent stock avoiding is as important as intelligent stock picking.

Knowing which stocks to avoid can work wonders for your portfolio – and can protect you from the perils of opportunity cost.

But what many investors fail to realize is that opportunity cost often hides in what seem like good stocks – in well-known, popular stocks. Overtly risky securities claim few victims. Everyone knows they’re risky and prepares accordingly. But familiar, “safe” securities are often the ones that produce disappointing, if not disastrous, results.

The Secret Ingredient

This “Portfolio Purge” Formula becomes even more effective by adding one small refinement to it.

I’m not going to reveal that specific refinement because I consider it proprietary to my investment process, but it turns out that by adding this refinement, the predictive value of my debt-to-sales analysis becomes even more reliable.

Furthermore, my refined analysis doesn’t merely identify a “Bottom 10.” It also identifies a “Bottom 25″… or an even greater number of sickly stocks, depending on market conditions.

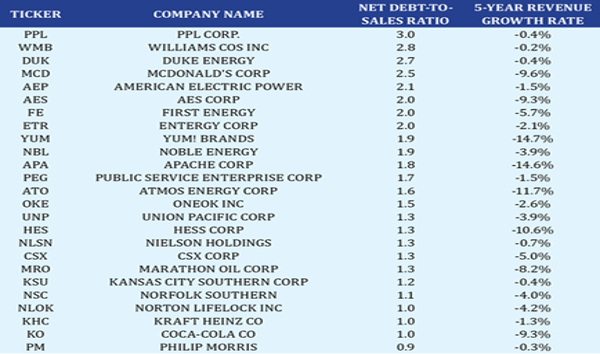

At year end 2019, I ran my refined debt-to-sales filter on the S&P 500 Index, ex-financials, and it produced the “Bottom 25” list below. Based on historic tendencies, these slow growing, heavily indebted stocks, as a group, will struggle to keep pace with the overall stock market during the next five years.

Then, on June 30, 2021, I calculated their results for that time frame. On average, this group performed as poorly as I expected. 80% of them performed worse than the S&P 500 during the measurement period, including nine of the 25 stocks that produced a loss.

Therefore, even though five of the 25 stocks managed to top the S&P’s performance, the average return of all stocks in the group was 12%… or just one-third the 36% gain the S&P 500 delivered over the same time frame.

A few weeks ago, I ran all the mid- and large-cap stocks on the New York Stock Exchange through my proprietary filter once again, and it kicked out the 12 stocks you see below. Already, most of the stocks on this list are performing poorly. Since the date I created this list, only two of the 12 stocks have performed better than the S&P 500 Index.

If these companies continue piling up debt faster than revenues, they will struggle to maintain their dominance. The dustbin of financial history is packed full of famous American companies that eventually lost their way… and perished.

Somewhat surprisingly, this updated list includes some iconic American names like McDonald’s Corp. (MCD), IBM Corp. (IBM), and The Coca-Cola Co. (KO). But even world-dominating companies like these are subject to the basic laws of economics.

To be clear, I am not suggesting that either McDonald’s or Coca-Cola is in any immediate financial peril. But what I am suggesting is that these companies have become so debt-laden that their stocks are likely to perform relatively poorly over the next few years.

That’s what a portfolio purge is all about – avoiding underperformers so that you can make room for outperformers.

Regards,

![]()

Eric Fry