Are you ready for risk-off? … two trades from Eric Fry looking poised to generate strong returns … two hedge trades to balance your portfolio

In 2022, which of the following will have better returns?

Volkswagen or Tesla?

Gold or Bitcoin?

Intel or NVIDIA?

Got your picks?

Our macro specialist, Eric Fry, is going with…drumroll…Volkswagen, gold, and Intel.

A few of you might suddenly be choking on your dinner. So, let’s jump straight to Eric for more color:

I expect the “character” of the financial markets to shift noticeably from a “risk-on” bias to “risk off.”

In other words, I expect investors to behave more cautiously and timidly than they did in 2021.

Generally speaking, therefore, I’m expecting relatively cautious investments to outperform their relatively risky counterparts.

“Caution” certainly feels appropriate after the market’s selloff in recent weeks, including today’s massive turnaround that saw the Nasdaq go from 2% gains to a loss (as I write, near the end of the day).

Yesterday, the Nasdaq slipped into an official correction. Meanwhile, the S&P and Dow are down roughly 6% and 5% from recent highs.

So, what 2022 trends will present investors that wonderful combination of returns and caution?

In Eric’s latest issue of Investment Report, he detailed several. Today, let’s peek into the issue to find out what opportunities Eric sees outperforming in 2022.

***A fantastic setup in commodities

For newer Digest readers, Eric is our global macro specialist and the editor behind Investment Report. As a macro investor, he evaluates markets and asset classes from a big-picture perspective to identify attractive opportunities.

Once a macro trend is in his crosshairs, he digs down to find the right, specific investment to play the opportunity.

It’s been a powerful strategy. In his decades in the business, Eric has dug up more 1,000%+ gaining investments than anyone we know of in the newsletter industry.

Returning to cautious approaches to 2022, Eric points toward commodities.

Now, regular Digest readers are familiar with Eric’s bullishness on the copper trade. In fact, yesterday’s Digest touched on this.

We won’t rehash those details again, but here’s Eric’s quick take:

Bottom line: Robust future demand growth for copper is fairly certain, but the mining industry’s capacity to satisfy that growth is not.

That’s the sort of equation that should put upward pressure on the copper price for many years to come.

But copper isn’t the only commodity Eric likes in 2022.

The second is something our world wants to do without, but addictions are hard to break. And this one is likely to generate great returns before it kicks the bucket.

From Eric:

No matter how “doomed” crude oil may be over the long term, it could deliver some spectacular short-term gains.

The bullish backdrop for crude has become too compelling to ignore.

***In the past, Eric has highlighted the fallacy of “more electric vehicles mean oil is dead”

In short, though EVs will capture a growing share of the global auto market in coming years, the total auto market will continue to grow larger. That means the number of gas-powered automobiles on the road will continue to increase as well.

When you combine that reality with demand from other industries, the International Energy Agency (IEA) expects worldwide demand will be at least 25% higher in 2050 than it is today.

Recently, oil demand has rebounded sharply, supporting higher prices. In fact, this week, oil hit a seven-year high (in part due to an attack by Yemeni Houthi rebels on the three United Arab Emirates fuel tankers).

But investors pointing toward this seven-year-high saying that prices are peaking are missing an important part of the equation – basic supply and demand.

As to demand, this is from yesterday in The Wall Street Journal:

Global oil demand will exceed pre-pandemic levels this year thanks to growing Covid-19 immunization rates and as recent virus waves haven’t proved severe enough to warrant a return to strict lockdown measures, the International Energy Agency said Wednesday.

And for supply, here’s Eric:

Most folks assume that OPEC and others could easily ramp production to satisfy any significant surge in demand. But that assumption rests on a frail statistical foundation.

The U.S. has supplied almost all of the world’s crude production growth during the last decade, not OPEC. Pulling that rabbit out of the hat a second time will not be easy, as U.S. shale production topped out two years ago.

Eric points out that oil and gas companies have been slashing the exploration budgets for years. Global investments in oil and gas exploration and production are down by about 65% since 2014.

It’s not hard to connect the dots:

Net-net: Bountiful new supplies of crude oil seem highly unlikely.

A tightening oil market, coupled with a rising inflationary trend, provides ample reason to expect oil stocks to deliver market-beating results in 2022.

***Two “hedge” plays to balance your broader portfolio

Copper and oil are likely to bring firepower to your returns this year – think “offense.”

Let’s now look at two ways to play defense: gold and a bet against bonds.

Starting with gold, there’s no denying that this trade has been incredibly disappointing, most notably because it’s done nothing while inflation has surged.

From Eric:

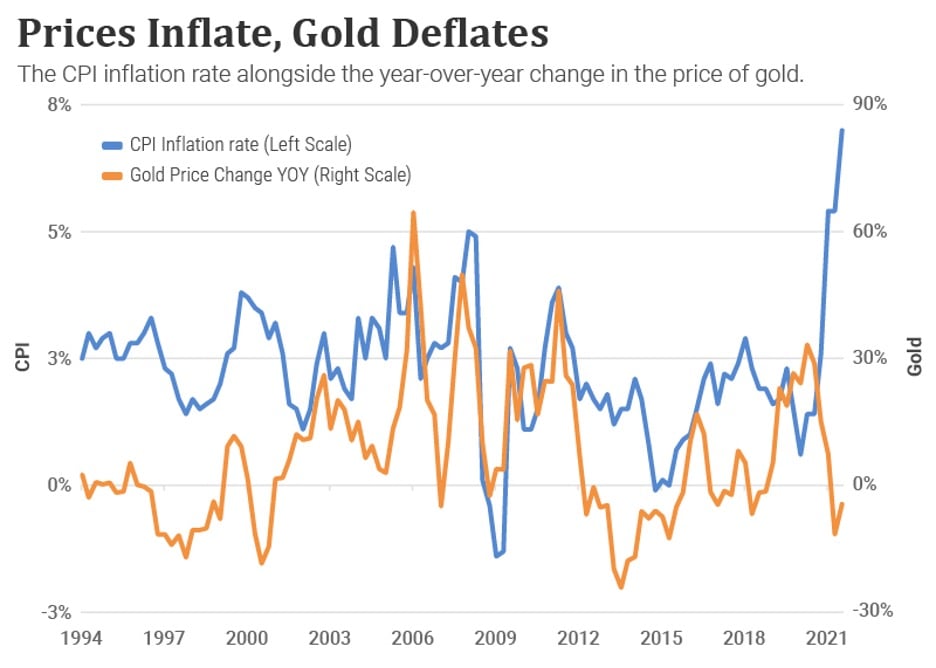

As the chart below shows, the gold price trend tends to track the inflation trend… but not this time around.

Despite the skyrocketing inflation reading on the right side of the chart, the gold price has been falling!

Even so, the yellow metal deserves the benefit of the doubt, both as an inflation hedge and as a hedge against stock market volatility… at least for now.

I still believe gold-related plays deserve a few investment dollars in a balanced portfolio.

Plus, gold might get a boost from an unexpected source…grumpy Bitcoin investors.

Through nearly all of 2021, Bitcoin acted like an inflation hedge. As yields surged, so too did Bitcoin’s price. When they fell, Bitcoin dropped.

As we noted earlier this week here in the Digest, this relationship appears to have come to a fiery crash in 2022.

What we’re seeing now is Bitcoin being treated as a risk asset. As yields surge, investors have been dumping Bitcoin.

But they’re not dumping gold.

Below, we look at gold versus Bitcoin since December 1. Bitcoin has lost 27% while gold is up 4%.

Remember, both of these assets derive their value from one source – emotion.

If we are truly seeing a broad shift toward “risk off” sentiment, all signs point toward gold being considered a stabler storehouse of value than cryptos.

And this could attract some “me too” Bitcoin investors who have been burned and are now looking for something more solid.

(To avoid confusion, we’re bullish on Bitcoin and elite altcoins. The analysis above refers to the mindsets behind investing in the two asset classes.)

***For the second hedge play, consider a bet against bonds

Interest rates have been sliding for four decades. But Eric suggests we could finally see a reversal this year.

From his issue:

As most folks are aware, the CPI inflation rate is running red-hot at a 40-year high of 7%. That means the buyer of a 30-year Treasury bond yielding 2.0% is receiving a robust after-inflation return of minus 5% per year.

That math is not the kind that builds wealth.

Sooner or later, bond buyers might demand more than 2% interest to tie up their money for 30 years… especially because the federal deficit is still running at a $215 billion monthly clip, or $2.6 trillion per year…

Without the price-insensitive Federal Reserve sopping a big chunk of that titanic Treasury bond supply, who will? And at what price?

Someone will buy our bonds, of course. But they might demand a much higher rate of interest to do so.

Eric is quick to point out that a sustained rising rate environment is not a certainty.

In fact, just about everyone is anticipating rates will be much higher a year from today. And longtime investors will likely tell you that when everyone believes the same narrative about the market, surprises often result.

That said, higher rates are enough of a possibility for Eric to feel confident about taking on this trade as a hedge.

If you’re an Investment Report subscriber, be sure to check out your latest issue. Eric details the specific investments he’s recommending for each of these trends plus a few others. To learn more about joining Eric in Investment Report, click here.

***Wrapping up, who knows what 2022 will bring, but it’s unlikely to offer the huge, broad returns as 2021

Is your portfolio ready for that?

If not, look at the trends we’ve touched on today. They’re likely to provide both returns and an added degree of portfolio hedging.

I’ll give Eric the final word:

Markets are forever and always cyclical. Sometimes cycles take their sweet time to shift direction, but they always do… eventually.

Once upon a time, hedging was a worthwhile activity…

That was before the Fates shifted and began smiling on unhedged strategies.

I believe the Fates may be shifting once again. We’ll see.

Have a good evening,

Jeff Remsburg