Ford Motor Company (NYSE:F) stock has slipped by around 42% since the turn of the year. Although many might be surprised by F stock’s recent capitulation, there’s a perfectly valid reason for it, and I’m afraid that matters won’t get better anytime soon.

I’ve noticed that many analysts are bullish on F stock amid its elaborate electric vehicle (EV) expansion. However, the central argument is somewhat of a drift considering the cost trade off. Furthermore, near term price discovery needs to be considered here as there’s no use investing in a mature asset before it enters a significant cyclical downturn. In addition, F stock is at a poor technical level, implying that a further downturn is in the offing.

Let’s delve into the details a little further.

| Ticker | Company | Price |

| F | Ford Motor Company | $12 |

Key Observations on F Stock

Ford released a disappointing May U.S. sales report earlier this month. The report revealed a total year-over-year sales decrease of 4.5% and a retail sales decrease of 5.7%. Additionally, Ford’s first-quarter earnings report shows that its total wholesale shipments are down by 9% versus last year, conveying a slowdown in global consumption.

Although Ford’s traditional vehicle sales have slipped, its EV sales have continued to gather steam with a 2.22x year-over-year increase in top-line growth. Although Ford’s EV segment is blossoming, it’s worth considering that it’s still a tiny part of the firm’s revenue mix. For instance, only 4.05% of Ford’s U.S. revenue is garnered from EVs.

I fully understand that we all need to be forward-looking when it comes to the financial markets and Ford’s business model. Nevertheless, Ford’s pivot to EVs is going to be expensive, with a planned investment of approximately $30 billion, which probably doesn’t cover much of the required restructuring costs. Moreover, as the EV space matures, Ford’s sales growth will naturally slow down as new market entrants enter the fray.

Lastly, Ford is a cyclical stock as it sells financed durable goods. As the economy continues to contract, we’ll likely see a decline in F stock’s financial performance and its stock.

Key Metrics & Systemic Risk

Click to Enlarge

Ford is really struggling to discover efficiency as global supply-chain congestion persists. The company’s gross profit margin is at a mere 11.36%, meaning it doesn’t possess economies of scale. Also, Ford’s return on invested capital of 4.08% and its debt-to-equity ratio of 3.05x implies that the firm might have capital structure issues, which could be extremely damaging to the enterprise if its sales start to wane.

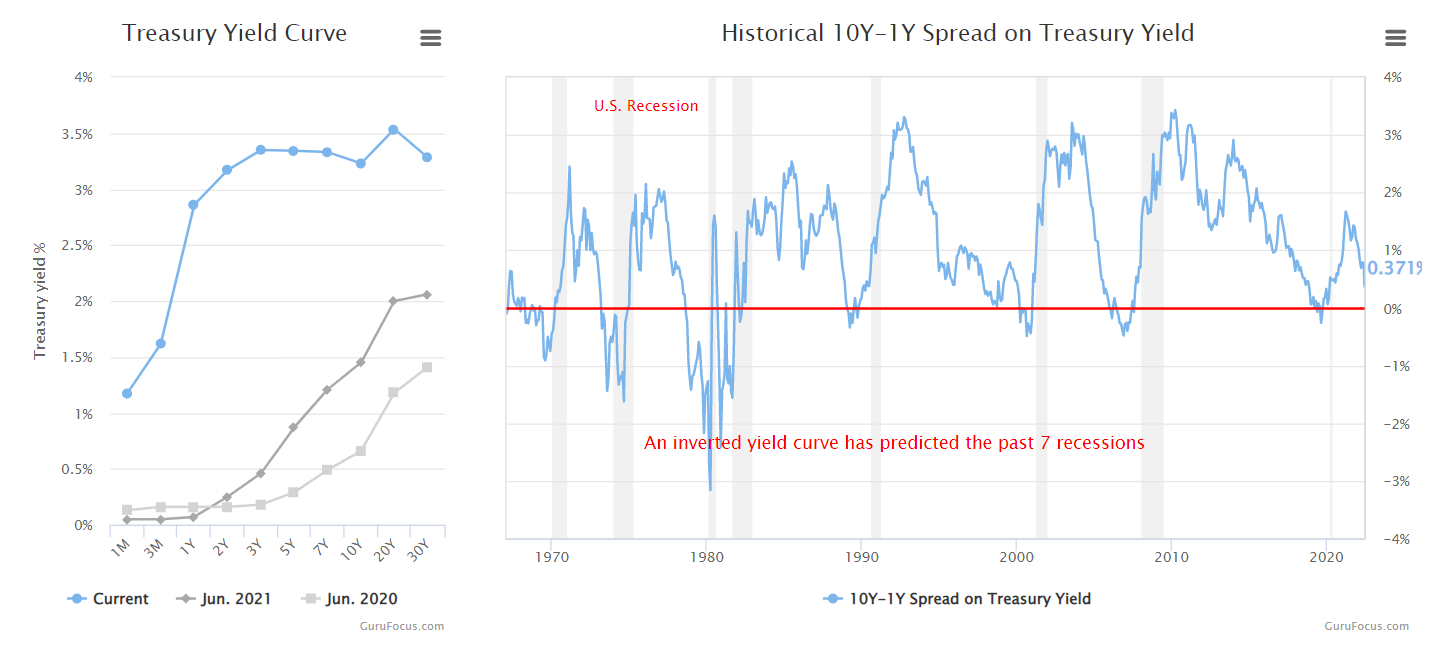

Furthermore, I expect systemic risk to exacerbate the state of the mentioned metrics. The curve implies that rising interest rates will contract the economy for the next two years, which could directly influence cyclical stocks, such as Ford. If benchmark rates follow the yield curve, we’ll likely see a tough two years ahead for F stock.

My Final Take on F Sock

Ford stock has slipped into a downward spiral. The key elements outlined in the article, coupled with the fact that F stock is trading below its 10-, 50-, 100-, and 200-day moving averages, implies that it is an asset to stay away from for now.

On the date of publication, Steve Booyens held an indirect long position in F. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.